AI PCの市場機会、成長促進要因、産業動向分析、2025~2034年予測

AI PC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750350

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

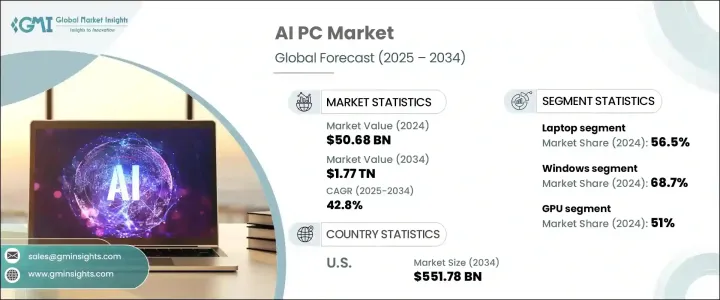

世界のAI PC市場は、2024年に506億8,000万米ドルと評価され、コンピューティングデバイスにおけるニューラルプロセッシングユニット(NPU)の統合が進んでいることを背景に、CAGR 42.8%で成長し、2034年には1兆7,700億米ドルに達すると推定されています。

これらの内蔵AIアクセラレータは、PCを、高度で低遅延のAI機能をデバイス上で直接サポートできるインテリジェント・システムに変えつつあります。主な成長要因は、生産性、コンテンツ作成、コミュニケーション、およびデバイスのセキュリティにわたるリアルタイムのAI駆動機能に対するユーザーの要求が進化していることに起因します。この移行は、従来のコンピューティングから、より優れたパフォーマンスとデータ保護のために処理をローカライズするAIネイティブ・インフラへのシフトを意味します。

半導体や高性能プロセッサなどの主要部品に対する関税を含む貿易規制は、AI PCのコスト構造に影響を与えています。こうした規制は、価格変動や納期延長につながるだけでなく、国際的に不可欠な技術へのアクセスを阻害しています。これに対応するため、メーカー各社はサプライチェーンを再編成し、輸入品への依存度を下げ、各国の技術政策へのコンプライアンスを確保するため、地域で生産される部品に目を向けています。このシフトは、主要経済諸国における国産チップ製造のインセンティブと一致しており、国産AIエコシステムの開発を強化しています。現地調達はまた、中断のない生産サイクルを維持し、世界の貿易摩擦に関連するリスクを軽減するという戦略的利点ももたらします。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 506億8,000万米ドル |

| 予測金額 | 1兆7,700億米ドル |

| CAGR | 42.8% |

日常的なコンピューティング・タスクでAI対応ソフトウェアの利用が増加していることから、ビジネスとコンシューマの両市場でAI PCの導入が加速しています。クラウドにデータをオフロードすることなくユーザー体験を向上させるオンデバイスAIアプリケーションをサポートするデバイスが増加しています。このセットアップにより、今日のハイブリッドなワークカルチャーにおいて特に重要な、より高いデータプライバシーと迅速なパフォーマンスが保証されます。AI PCは現在、インテリジェントなエンドポイントとして機能し、エッジおよびクラウド・コンピューティング・システムとシームレスに連携して、分散AIワークロードを効率的に管理しています。セキュアで分散型のAIフレームワークの進化は、世界な規制機関によって積極的に推進されており、応答性とコンプライアンスに優れたAIシステムの必要性が強調されています。

ハードウェア設計別では、AI PC市場はデスクトップ、ラップトップ、ワークステーションに区分されます。2024年には、ノートPCが56.5%と最大のシェアを占め、AI機能と統合されたポータブル・コンピューティング・パワーに対する需要の高まりが牽引しています。これらのデバイスは現在、AIタスク専用に設計されたプロセッサを搭載しており、外出先でインテリジェントな機能を必要とするモバイルユーザーにとって理想的なものとなっています。バッテリー寿命の向上、応答性の高いユーザーインターフェース、マルチメディア機能の強化も、専門家や一般消費者にAI搭載ノートPCへのアップグレードを促しています。

OS別に分類すると、Windowsが2024年のシェア68.7%でAI PC市場をリードしています。この優位性は、Windowsプラットフォームを中心に構築されたハードウェアパートナー、ソフトウェアエコシステム、企業の採用が広く存在することに起因しています。古いオペレーティングシステムの段階的な廃止によってハードウェアの更新サイクルが継続することで、企業はコンプライアンス、セキュリティ、生産性機能が強化された、AIに最適化された新しいWindows PCに投資するようになっています。

コンピューティングタイプ別に見ると、市場はGPU、NPU、その他に分けられます。GPUは、複雑なAIアルゴリズムを処理し、ハイエンドのグラフィックス性能を提供する上で重要な役割を担っているため、2024年の市場シェアは51%と最も高いです。これらのプロセッサは、ディープラーニング、画像処理、リアルタイムデータ分析などのAIワークロードを処理する上で特に重要です。高度なGPUアーキテクチャの統合により、ビジュアル品質が向上し、幅広いアプリケーションでAIアクセラレーション機能が利用できるようになっています。

地域別では、米国のAI PC市場は2034年までに5,517億8,000万米ドルに達すると予測されます。国内AIおよび半導体インフラへの政府の強力な投資が、エッジAIソリューションへの企業の関心と相まって、市場成長を牽引しています。AIベースのツールやサービスを採用する企業が増えるにつれ、高性能コンピューティングデバイスのニーズは高まり続けています。技術の独立性とデジタル・レジリエンスへのシフトは、厳しいデータ保護と性能基準を満たすAI PCの採用を企業に促しています。

AI PC分野における競合は激化しており、規制要件や生産性向上への要求が購買決定の中心となっています。ヘルスケア、教育、金融などさまざまな業界の組織が、業務効率を維持しながらコンプライアンス基準を満たすためにAI PCに注目しています。オンデバイスでのAI処理により、クラウドストレージへの依存度を低減することが可能となり、世界のデータ保護およびサイバーセキュリティ規制の強化に合致しています。生成的なAIツールやインテリジェントな自動化に対する需要が高まる中、企業はワークフローを最適化し、反復作業を削減し、情報に基づいた意思決定をサポートするために、AI対応システムでITインフラを刷新しています。PCメーカーとソフトウェア開発者の共同開発により、AIの統合がさらに強化され、ユーザーとパーソナルコンピューティングデバイスの関わり方が変化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(サービスプロバイダー)

- 主要サービスの価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(価格設定)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サーバープロバイダーの再構成

- 価格設定とサービス戦略

- 政策関与

- 展望と今後の検討事項

- 供給側の影響(サービスプロバイダー)

- 貿易への影響

- 業界への影響要因

- 促進要因

- PCへのニューラルプロセッシングユニット(NPU)の統合

- AI搭載アプリケーションの急増

- AIアルゴリズムの進歩

- AIに関する政府の取り組みと投資

- クラウドとエッジコンピューティングの拡大

- 業界の潜在的リスク&課題

- AI統合ハードウェアコンポーネントの高コスト

- デバイス上でのAI処理におけるデータプライバシーとセキュリティの懸念

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:ハードウェア設計別、2021-2034

- 主要動向

- デスクトップ

- ソフトウェア

- ワークステーション

第6章 市場推計・予測:OS別、2021-2034

- 主要動向

- Windows

- MacOS

- その他

第7章 市場推計・予測:コンピューティングタイプ別、2021-2034

- 主要動向

- GPU

- NPU

- その他

第8章 市場推計・予測:最終用途別、2021-2034

- 消費者

- 企業

第9章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア・ニュージーランド

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Acer

- Apple Inc.

- ASUSTeK Computer Inc.

- BOXX

- CORSAIR

- Dell Inc.

- GIGA-BYTE Technology Co.、Ltd.

- HP Development Company、L.P

- Huawei

- Lenovo

- Microsoft

- Micro-Star INT'L CO.、LTD.

- NVIDIA Corporation

- Puget Systems

- Razer Inc.

目次

The Global AI PC Market was valued at USD 50.68 billion in 2024 and is estimated to grow at a CAGR of 42.8% to reach USD 1.77 trillion by 2034, fueled by the increasing integration of neural processing units (NPUs) in computing devices. These built-in AI accelerators are transforming PCs into intelligent systems capable of supporting advanced, low-latency AI functions directly on the device. A major growth factor stems from evolving user demands for real-time, AI-driven capabilities across productivity, content creation, communication, and device security. This transition marks a shift from traditional computing to AI-native infrastructure, where processing is localized for better performance and data protection.

Trade regulations, including tariffs on key components like semiconductors and high-performance processors, have impacted the cost structure of AI PCs. These restrictions have not only led to price volatility and increased delivery timelines but have also disrupted access to essential international technologies. As a response, manufacturers are realigning supply chains and turning toward regionally produced components to reduce dependency on imports and ensure compliance with national tech policies. This shift is in line with domestic chip-making incentives across major economies, reinforcing the development of homegrown AI ecosystems. Local sourcing also provides strategic advantages in maintaining uninterrupted production cycles and mitigating risks linked to global trade tensions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $50.68 Billion |

| Forecast Value | $1.77 Trillion |

| CAGR | 42.8% |

The increasing use of AI-enabled software in everyday computing tasks is accelerating the adoption of AI PCs across both business and consumer markets. More devices are being built to support on-device AI applications, which enhance user experience without needing to offload data to the cloud. This setup ensures greater data privacy and quicker performance, which are especially critical in today's hybrid work culture. AI PCs are now acting as intelligent endpoints, working seamlessly with edge and cloud computing systems to manage distributed AI workloads efficiently. The evolution of secure, decentralized AI frameworks is being actively promoted by global regulatory bodies, emphasizing the need for responsive and compliant AI systems.

In terms of hardware design, the AI PC market is segmented into desktops, laptops, and workstations. In 2024, laptops accounted for the largest share at 56.5%, driven by growing demand for portable computing power integrated with AI capabilities. These devices now come equipped with processors specifically designed for AI tasks, making them ideal for mobile users who need intelligent features on the go. Improved battery life, responsive user interfaces, and enhanced multimedia functions are also encouraging professionals and general consumers to upgrade to AI-powered laptops.

When categorized by operating systems, Windows leads the AI PC market with a share of 68.7% in 2024. This dominance can be attributed to the widespread presence of hardware partners, software ecosystems, and enterprise adoption built around the Windows platform. Ongoing hardware refresh cycles, driven by the phasing out of older operating systems, are pushing organizations to invest in new AI-optimized Windows PCs that offer enhanced compliance, security, and productivity features.

By compute type, the market is divided into GPUs, NPUs, and others. GPUs held the highest market share at 51% in 2024, owing to their vital role in processing complex AI algorithms and delivering high-end graphics performance. These processors are particularly important for handling AI workloads such as deep learning, image processing, and real-time data analysis. The integration of advanced GPU architectures is enhancing visual quality and enabling AI-accelerated features across a wide range of applications.

In regional terms, the U.S. AI PC market is expected to reach USD 551.78 billion by 2034. Strong government investments in domestic AI and semiconductor infrastructure, combined with corporate interest in edge AI solutions, are driving market growth. As more companies embrace AI-based tools and services, the need for high-performance computing devices continues to grow. The shift toward technology independence and digital resilience is encouraging businesses to adopt AI PCs that meet stringent data protection and performance standards.

Competition in the AI PC space is intensifying, with regulatory requirements and productivity demands becoming central to purchasing decisions. Organizations across industries such as healthcare, education, and finance are turning to AI PCs to meet compliance standards while maintaining operational efficiency. On-device AI processing enables reduced reliance on cloud storage, aligning with increasing global data protection and cybersecurity regulations. As demand for generative AI tools and intelligent automation grows, companies are refreshing IT infrastructure with AI-ready systems to optimize workflows, cut down on repetitive tasks, and support informed decision-making. Collaborative efforts between PC manufacturers and software developers are further enhancing AI integration, transforming the way users interact with personal computing devices.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.1.3 Impact on the industry

- 3.2.1.3.1 Supply-side impact (service providers)

- 3.2.1.3.1.1 Price volatility in key services

- 3.2.1.3.1.2 Supply chain restructuring

- 3.2.1.3.1.3 Production cost implications

- 3.2.1.3.2 Demand-side impact (pricing)

- 3.2.1.3.2.1 Price transmission to end markets

- 3.2.1.3.2.2 Market share dynamics

- 3.2.1.3.2.3 Consumer response patterns

- 3.2.1.3.3 Key companies impacted

- 3.2.1.3.4 Strategic industry responses

- 3.2.1.3.4.1 Server provider reconfiguration

- 3.2.1.3.4.2 Pricing and service strategies

- 3.2.1.3.4.3 Policy engagement

- 3.2.1.3.5 Outlook and future considerations

- 3.2.1.3.1 Supply-side impact (service providers)

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Integration of Neural Processing Units (NPUs) in PCs

- 3.3.1.2 Surge in AI-powered applications

- 3.3.1.3 Advancements in AI algorithms

- 3.3.1.4 Government initiatives and investments in AI

- 3.3.1.5 Expansion of cloud and edge computing

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High cost of AI-integrated hardware components

- 3.3.2.2 Data privacy and security concerns in on-device AI processing

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Form Factor, 2021-2034 (USD Billion & units)

- 5.1 Key trends

- 5.2 Desktop

- 5.3 Software

- 5.4 Workstation

Chapter 6 Market Estimates & Forecast, By Operating System, 2021-2034 (USD Billion & units)

- 6.1 Key trends

- 6.2 Windows

- 6.3 MacOS

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Compute Type, 2021-2034 (USD Billion & units)

- 7.1 Key trends

- 7.2 GPU

- 7.3 NPU

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion & units)

- 8.1 Consumers

- 8.2 Enterprises

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion & units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 ANZ

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Acer

- 10.2 Apple Inc.

- 10.3 ASUSTeK Computer Inc.

- 10.4 BOXX

- 10.5 CORSAIR

- 10.6 Dell Inc.

- 10.7 GIGA-BYTE Technology Co., Ltd.

- 10.8 HP Development Company, L.P

- 10.9 Huawei

- 10.10 Lenovo

- 10.11 Microsoft

- 10.12 Micro-Star INT'L CO., LTD.

- 10.13 NVIDIA Corporation

- 10.14 Puget Systems

- 10.15 Razer Inc.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日