|

市場調査レポート

商品コード

1750346

プロバイオティクス飲料の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Probiotic Drinks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| プロバイオティクス飲料の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月06日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

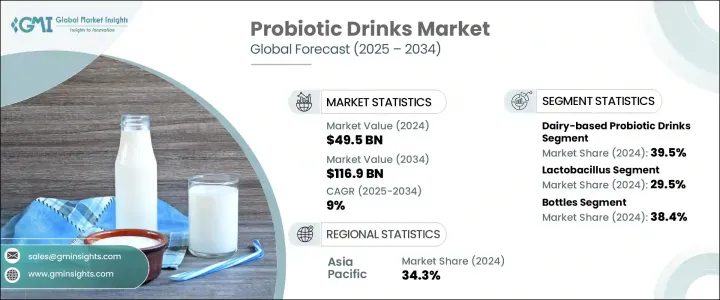

世界のプロバイオティクス飲料市場は、2024年には495億米ドルと評価され、腸の健康、免疫力、総合的なウェルネスに対する消費者の関心の高まりにより、CAGR9%で成長し、2034年には1,169億米ドルに達すると推定されています。

当初はヨーグルトとサプリメントに限られていたプロバイオティクス製品は、その後、機能性飲料、乳児用調製粉乳、さらには動物飼料にまで発展しています。市場の成長を支えているのは、プロバイオティクスの健康効果を確認する科学的調査と、消費者の意識の高まりです。

プロバイオティクス飲料の需要は、先進国市場と新興国市場の双方で高まっており、特に北米、欧州、アジア太平洋地域で高い伸びを示しています。アジア太平洋市場は、人口の多さ、可処分所得の増加、食生活の嗜好の変化により、最も高い成長率が見込まれています。さらに、人口の高齢化と代謝性疾患や胃腸疾患の増加が、プロバイオティクスベースの製品に対する需要を促進しています。調査によると、飲食品、特に乳製品にプロバイオティクスを取り入れることで、消費者の受容性と製品の安定性が大幅に向上し、市場が拡大しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 495億米ドル |

| 予測金額 | 1,169億米ドル |

| CAGR | 9% |

乳製品ベースのプロバイオティクス飲料セグメントは2024年に39.5%のシェアを占める。これらの飲料はその栄養価の高さから依然として人気が高く、ヨーグルト飲料やケフィアが特定の地域で優位を保っています。しかし、市場は植物ベースのプロバイオティクス飲料へのシフトを目の当たりにしています。この変化は、ビーガン、ラクトースフリー、アレルゲンフリーの代替品に対する需要の高まりが主な要因となっています。大豆、アーモンド、ココナッツ、オート麦などを原料とする飲料は、その味と健康上の利点から人気を集めています。

プロバイオティクス飲料市場はプロバイオティクス菌株別に分類され、2024年には乳酸桿菌が29.5%のシェアを占めてリードしています。L.ラムノサスやL.アシドフィルスなどの乳酸菌株は、消化器系の健康を促進し、免疫力を高めることでよく知られています。ビフィダム菌やロンガム菌のような他の菌株は、特に高齢者や子供の健康的な腸内バランスの維持に役立ちます。プロバイオティクスの利点に対する消費者の認識が高まるにつれ、これらの菌株が市場拡大の原動力になると予想されます。

アジア太平洋プロバイオティクス飲料2024年の市場シェアは34.3%。この地域は急速な成長を遂げており、日本のような国々は科学的裏付けのあるプロバイオティクス製品に注力している一方、中国やインドはヨーグルトやコンブチャのような健康志向の飲料をますます受け入れています。北米でもウェルネス動向の高まりが見られ、飲むヨーグルトやコンブチャなどの機能性飲料の需要が高まっています。

In the Globalプロバイオティクス飲料Market, companies like Yakult Honsha Co.Ltd.、Groupe Danone SA、The Fonterra Co-op Group Ltd.、Kerry Group PLC、Groupe Lactalisなどの企業は、市場での存在感を高めるために重要な戦略を採用しています。これらの戦略には、幅広い機能性飲料や植物性飲料を含む製品ポートフォリオの拡大、製品の品質を高めるための先進生産技術の活用、環境に配慮したパッケージングや調達慣行による持続可能性の動向への対応などが含まれます。さらに、これらの企業は、変化する消費者の嗜好に合った革新的な製品を生み出すための研究開発に投資しており、製品の安定性の向上と健康効果の強化に注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 製造業者

- 販売代理店

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 供給側の影響(原材料)

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 北米

- FDA規制(米国)

- カナダ保健省の規制

- 欧州

- 欧州食品安全機関(EFSA)ガイドライン

- EUの健康強調表示規制

- アジア太平洋地域

- 特保規制(日本)

- CFDA規制(中国)

- FSSAI規制(インド)

- 世界のその他の地域

- 影響要因

- 促進要因

- パーソナライズされた健康とウェルネスのニーズ

- 持続可能性と倫理的な調達

- 植物由来および乳製品以外の代替品への移行

- 業界の潜在的リスク&課題

- 高い生産コスト

- プロバイオティクスの生存能力維持における課題

- 市場機会

- 新興市場への拡大

- 製品配合における革新

- Eコマースと消費者直販チャネルの成長

- 植物由来の代替品に対する需要の高まり

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

- 製造プロセスと技術

- 製造プロセスの概要

- 原材料の調達と準備

- プロバイオティクス培養液の調製

- 発酵と加工

- 配合とブレンド

- 包装と保管戦略

- 生産コスト分析

- 原材料費

- 処理コスト

- 人件費

- 梱包コスト

- 製造間接費

- コスト最適化戦略

- 製造施設分析

- 施設拡張計画

- サプライチェーンの課題と解決策

- 原材料調達

- サプライチェーン全体の品質管理

- コールドチェーン管理

- 在庫管理

- 品質保証と管理

- 微生物検査

- 安定性および保存期間の試験

- 官能評価

- 製造プロセスの概要

- 消費者行動と市場動向の分析

- 消費者の嗜好と購買パターン

- 消費者の人口統計分析

- 消費者の意識と教育

- 新たな消費者動向

- デジタル変革が消費者エンゲージメントに与える影響

- 消費者フィードバック分析とその影響

- 価格動向分析

- 価格に影響を与える要因

- 原材料費

- 生産および加工コスト

- 製品セグメント全体の価格戦略

- プレミアム市場とマス市場のポジショニング

- 価値に基づく価格設定アプローチ

- 価格に影響を与える要因

- 地域別の価格変動とその要因

- 価格と価値の関係分析

- 市場に影響を与える経済指標

- プロバイオティクス飲料の現在の技術動向

- 新興技術とその潜在的な影響

- マイクロカプセル化技術

- シンバイオティクス製剤

- 製品イノベーションの動向

- 機能性成分の組み合わせ

- 常温保存可能なプロバイオティクスソリューション

- パッケージングの革新

- 持続可能な包装材料

- アクティブでインテリジェントなパッケージング

- 生産と流通におけるデジタル技術

- IoTとスマート製造

- トレーサビリティのためのブロックチェーン

- 研究開発活動とイノベーションハブ

- 地域ごとの技術導入動向

- アジア太平洋が機能性飲料技術の導入でリード

- 生産技術における持続可能性を重視する欧州

- 将来の技術ロードマップ 2025-2033

- パーソナライズされたプロバイオティクスソリューションの開発

- 品質管理システムにおける自動化とAI

- 新興技術とその潜在的な影響

- マーケティング戦略とブランド分析

- 現在のマーケティング情勢

- デジタルマーケティング戦略

- 従来のマーケティング手法

- 健康コミュニケーション戦略

- 主要プレーヤーのブランド分析

- マーケティングツールとしてのパッケージ

- 将来のマーケティング動向と戦略

- 市場機会と戦略的提言

- 未開拓の市場機会

- 市場参入企業への戦略的提言

- 製品開発戦略

- 市場参入と拡大戦略

- 競争優位性構築戦略

- 将来の成長経路

- リスク評価と軽減戦略

- 市場リスク

- 需要変動

- 競争圧力

- 運用リスク

- サプライチェーンの混乱

- 生産上の課題

- 規制およびコンプライアンスリスク

- 食品安全規制の変化

- ラベル表示および主張規制

- 評判リスク

- 環境と持続可能性のリスク

- リスク軽減戦略とフレームワーク

- 市場リスク

- 将来の見通しと市場の進化

- 長期市場予測2025-2035

- 将来の市場シナリオ

- 楽観的シナリオ

- 現実的なシナリオ

- 悲観的なシナリオ

- 新興製品カテゴリーとイノベーション

- 消費者の嗜好と行動の進化

- 技術の進化とその影響

- 持続可能性と循環型経済の発展

- 将来の競合情勢

- 長期的な成功のための戦略的必須事項

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 乳製品ベースのプロバイオティクス飲料

- プロバイオティクスヨーグルトドリンク

- ケフィア

- プロバイオティクスミルク飲料

- その他

- 植物由来のプロバイオティクス飲料

- 豆乳飲料

- アーモンドベースのドリンク

- ココナッツベースのドリンク

- その他

- 果物と野菜ベースのプロバイオティクス飲料

- プロバイオティクスフルーツジュース

- プロバイオティクス野菜ジュース

- フルーツと野菜のミックスドリンク

- 水性プロバイオティクス飲料

- プロバイオティクスウォーター

- プロバイオティクス炭酸飲料

- 発酵プロバイオティクス飲料

- コンブチャ

- クワス

- その他

- プロバイオティクス機能性飲料

- プロバイオティクスエナジードリンク

- プロバイオティクススポーツドリンク

- プロバイオティクスウェルネスショット

第6章 市場推計・予測:プロバイオティクス菌株別、2021-2034

- 主要動向

- 乳酸菌

- ビフィズス菌

- 連鎖球菌

- バチルス

- サッカロミセス

- 多菌株製剤

第7章 市場推計・予測:包装形態別、2021-2034

- 主要動向

- ボトル

- カートン

- 缶

- ポーチ

- その他

第8章 市場推計・予測:ターゲット消費者グループ別、2021-2034

- 主要動向

- 一般成人人口

- 子どもと青少年

- 高齢者人口

- アスリートやフィットネス愛好家

- 健康志向の消費者

第9章 市場推計・予測:消費シーン別、2021-2034

- 主要動向

- 1日の消費量

- 食事代替品

- 外出先での消費

- 運動後の回復

第10章 市場推計・予測:価格帯別、2021-2034

- 主要動向

- エコノミー/マスマーケット

- ミッドレンジ

- プレミアム/高級

第11章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- スーパーマーケットとハイパーマーケット

- コンビニエンスストア

- 専門健康食品店

- 薬局とドラッグストア

- オンライン小売

- 食品サービス部門

第12章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- B2B

- B2C

第13章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第14章 企業プロファイル

- Yakult Honsha Co.、Ltd.

- Danone S.A.

- Nestle S.A.

- PepsiCo、Inc.

- Coca-Cola Company

- Lifeway Foods、Inc.

- Harmless Harvest

- KeVita(PepsiCo)

- GoodBelly(NextFoods)

- Chobani、LLC

- Groupe Lactalis

- Bio-K Plus International Inc.

- Fonterra Co-operative Group Juicery

The Global Probiotic Drinks Market was valued at USD 49.5 billion in 2024 and is estimated to grow at a CAGR of 9% to reach USD 116.9 billion by 2034, driven by a surge in consumer interest in gut health, immunity, and overall wellness. Initially limited to yogurt and supplements, probiotic products have since evolved to include functional beverages, infant formulas, and even animal feed. The market's growth is supported by scientific research confirming the health benefits of probiotics, as well as increasing consumer awareness.

Demand for probiotic drinks is rising across both developed and emerging markets, with particularly high growth in North America, Europe, and the Asia-Pacific region. The Asia-Pacific market is expected to experience the highest growth rates due to its large population, increasing disposable income, and changing dietary preferences. Additionally, an aging population and a rise in metabolic and gastrointestinal disorders are driving the demand for probiotic-based products. Research has shown that incorporating probiotics into food and beverages, especially in dairy products, has significantly increased consumer acceptance and product stability, expanding the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $49.5 Billion |

| Forecast Value | $116.9 Billion |

| CAGR | 9% |

Dairy-based probiotic drinks segment held a 39.5% share in 2024. These drinks remain popular for their nutritional value, with yogurt drinks and kefir continuing to dominate in certain regions. However, the market is witnessing a shift toward plant-based probiotic drinks. This change is largely driven by growing demand for vegan, lactose-free, and allergen-free alternatives. Drinks made from ingredients like soy, almond, coconut, and oat are gaining popularity for their taste and health benefits.

The probiotic drinks market is categorized by probiotic strains, with Lactobacillus taking the lead, representing a 29.5% share in 2024. Lactobacillus strains such as L. rhamnosus and L. acidophilus are well-known for promoting digestive health and boosting immunity. Other strains like B. bifidum and B. longum help maintain a healthy gut balance, especially in the elderly and children. As consumer awareness of the benefits of probiotics grows, these strains are expected to drive market expansion.

Asia-Pacific Probiotic Drinks Market held a 34.3% share in 2024. The region is experiencing rapid growth, with countries like Japan focusing on science-backed probiotic products, while China and India are increasingly embracing health-conscious beverages like yogurt and kombucha. North America is also seeing a rise in wellness trends, with a growing demand for functional beverages such as drinkable yogurts and kombucha.

In the Global Probiotic Drinks Market, companies like Yakult Honsha Co. Ltd., Groupe Danone SA, The Fonterra Co-op Group Ltd., Kerry Group PLC, and Groupe Lactalis are adopting key strategies to strengthen their market presence. These strategies include expanding product portfolios to include a wider range of functional and plant-based drinks, leveraging advanced production technologies to enhance product quality, and aligning with sustainability trends through eco-friendly packaging and sourcing practices. Additionally, these companies are investing in research and development to create innovative products that meet changing consumer preferences, focusing on improving product stability and enhancing health benefits.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Manufacturers

- 3.1.5 Distributors

- 3.1.6 Impact on trade

- 3.1.7 Trade volume disruptions

- 3.2 Retaliatory measures

- 3.3 Impact on the industry

- 3.3.1 Supply-side impact (raw materials)

- 3.3.1.1 Price volatility in key materials

- 3.3.1.2 Supply chain restructuring

- 3.3.1.3 Production cost implications

- 3.3.1 Supply-side impact (raw materials)

- 3.4 Demand-side impact (selling price)

- 3.4.1 Price transmission to end markets

- 3.4.2 Market share dynamics

- 3.4.3 Consumer response patterns

- 3.5 Key companies impacted

- 3.6 Strategic industry responses

- 3.6.1 Supply chain reconfiguration

- 3.6.2 Pricing and product strategies

- 3.6.3 Policy engagement

- 3.7 Outlook and future considerations

- 3.8 Supplier landscape

- 3.9 Profit margin analysis

- 3.10 Key news & initiatives

- 3.11 Regulatory landscape

- 3.12 North America

- 3.12.1 FDA regulations (United States)

- 3.12.2 Health Canada regulations

- 3.13 Europe

- 3.13.1 European Food Safety Authority (EFSA) Guidelines

- 3.13.2 EU health claims regulation

- 3.14 Asia Pacific

- 3.14.1 FOSHU regulations (Japan)

- 3.14.2 CFDA regulations (China)

- 3.14.3 FSSAI regulations (India)

- 3.15 Rest of the world

- 3.16 Impact forces

- 3.16.1 Growth drivers

- 3.16.1.1 Personalized health and wellness needs

- 3.16.1.2 Sustainability and ethical sourcing

- 3.16.1.3 Shift toward plant-based and non-dairy alternatives

- 3.16.2 Industry pitfalls & challenges

- 3.16.2.1 High production costs

- 3.16.2.2 Challenges in maintaining probiotic viability

- 3.16.3 Market Opportunities

- 3.16.3.1 Expansion in emerging markets

- 3.16.3.2 Innovation in product formulations

- 3.16.3.3 Growth of E-commerce and direct-to-consumer channels

- 3.16.3.4 Rising demand for plant-based alternatives

- 3.16.1 Growth drivers

- 3.17 Growth potential analysis

- 3.18 Porter's analysis

- 3.19 PESTEL analysis

- 3.20 Manufacturing process and technology

- 3.20.1 Manufacturing process overview

- 3.20.1.1 Raw material procurement and preparation

- 3.20.1.2 Probiotic culture preparation

- 3.20.1.3 Fermentation and processing

- 3.20.1.4 Formulation and blending

- 3.20.1.5 Packaging and storage strategies

- 3.20.2 Production cost analysis

- 3.20.2.1 Raw material costs

- 3.20.2.2 Processing costs

- 3.20.2.3 Labor costs

- 3.20.2.4 Packaging costs

- 3.20.2.5 Manufacturing overheads

- 3.20.2.6 Cost optimization strategies

- 3.20.3 Manufacturing facilities analysis

- 3.20.3.1 Facility expansion plans

- 3.20.4 Supply chain challenges and solutions

- 3.20.4.1 Raw material sourcing

- 3.20.4.2 Quality control throughout supply chain

- 3.20.4.3 Cold chain management

- 3.20.4.4 Inventory management

- 3.20.5 Quality assurance and control

- 3.20.5.1 Microbial testing

- 3.20.5.2 Stability and shelf-life testing

- 3.20.5.3 Sensory evaluation

- 3.20.1 Manufacturing process overview

- 3.21 Consumer behavior and market trends analysis

- 3.21.1 Consumer preferences and purchasing patterns

- 3.21.2 Demographic analysis of consumers

- 3.21.3 Consumer awareness and education

- 3.21.4 Emerging consumer trends

- 3.21.5 Impact of digital transformation on consumer engagement

- 3.21.6 Consumer feedback analysis and implications

- 3.22 Pricing trends analysis

- 3.22.1 Factors affecting pricing

- 3.22.1.1 Raw material costs

- 3.22.1.2 Production and processing costs

- 3.22.2 Pricing strategies across product segments

- 3.22.2.1 Premium vs. mass market positionings

- 3.22.2.2 Value-based pricing approaches

- 3.22.1 Factors affecting pricing

- 3.23 Regional price variations and factors

- 3.24 Price-value relationship analysis

- 3.25 Economic indicators impacting the market

- 3.26 Current technological trends in probiotic drinks

- 3.26.1 Emerging technologies and their potential impact

- 3.26.1.1 Microencapsulation technologies

- 3.26.1.2 Synbiotic formulations

- 3.26.2 Product innovation trends

- 3.26.2.1 Functional ingredient combinations

- 3.26.2.2 Shelf-stable probiotic solutions

- 3.26.3 Packaging innovations

- 3.26.3.1 Sustainable packaging materials

- 3.26.3.2 Active and intelligent packaging

- 3.26.4 Digital technologies in production and distribution

- 3.26.4.1 IoT and smart manufacturing

- 3.26.4.2 Blockchain for traceability

- 3.26.5 R&D activities and innovation hubs

- 3.26.6 Technology adoption trends across regions

- 3.26.6.1 Asia-pacific leading in functional drink tech adoption

- 3.26.6.2 Europe emphasizing sustainability in production tech

- 3.26.7 Future technology roadmap 2025-2033

- 3.26.7.1 Development of personalized probiotic solutions

- 3.26.7.2 Automation and ai in quality control systems

- 3.26.1 Emerging technologies and their potential impact

- 3.27 Marketing strategies and brand analysis

- 3.27.1 Current marketing landscape

- 3.27.2 Digital marketing strategies

- 3.27.3 Traditional marketing approaches

- 3.27.4 Health communication strategies

- 3.27.5 Brand analysis of key players

- 3.27.6 Packaging as a marketing tool

- 3.27.7 Future marketing trends and strategies

- 3.28 Market opportunities and strategic recommendations

- 3.28.1 Untapped market opportunities

- 3.28.2 Strategic recommendations for market participants

- 3.28.3 Product development strategies

- 3.28.4 Market entry and expansion strategies

- 3.28.5 Competitive advantage building strategies

- 3.28.6 Future growth pathways

- 3.29 Risk assessment and mitigation strategies

- 3.29.1 Market risks

- 3.29.1.1 Demand fluctuations

- 3.29.1.2 Competitive pressures

- 3.29.2 Operational risks

- 3.29.2.1 Supply chain disruptions

- 3.29.2.2 Production challenges

- 3.29.3 Regulatory and compliance risks

- 3.29.3.1 Changing food safety regulations

- 3.29.3.2 Labeling and claims regulations

- 3.29.4 Reputational risks

- 3.29.5 Environmental and sustainability risks

- 3.29.6 Risk mitigation strategies and frameworks

- 3.29.1 Market risks

- 3.30 Future outlook and market evolution

- 3.30.1 Long-term market forecast 2025-2035

- 3.30.2 Future market scenarios

- 3.30.2.1 Optimistic scenario

- 3.30.2.2 Realistic scenario

- 3.30.2.3 Pessimistic scenario

- 3.30.3 Emerging product categories and innovations

- 3.30.4 Evolving consumer preferences and behaviors

- 3.30.5 Technological evolution and its impact

- 3.30.6 Sustainability and circular economy developments

- 3.30.7 Future competitive landscape

- 3.30.8 Strategic imperatives for long-term success

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Liters)

- 5.1 Key trends

- 5.2 Dairy-based probiotic drinks

- 5.2.1 Probiotic yogurt drinks

- 5.2.2 Kefir

- 5.2.3 Probiotic milk drinks

- 5.2.4 Others

- 5.3 Plant-based probiotic drinks

- 5.3.1 Soy-based drinks

- 5.3.2 Almond-based drinks

- 5.3.3 Coconut-based drinks

- 5.3.4 Others

- 5.4 Fruit and vegetable-based probiotic drinks

- 5.4.1 Probiotic fruit juices

- 5.4.2 Probiotic vegetable juices

- 5.4.3 Mixed fruit and vegetable drinks

- 5.5 Water-based probiotic drinks

- 5.5.1 Probiotic water

- 5.5.2 Probiotic sparkling beverages

- 5.6 Fermented probiotic beverages

- 5.6.1 Kombucha

- 5.6.2 Kvass

- 5.6.3 Others

- 5.7 Probiotic functional beverages

- 5.7.1 Probiotic energy drinks

- 5.7.2 Probiotic sports drinks

- 5.7.3 Probiotic wellness shots

Chapter 6 Market Estimates and Forecast, By Probiotic Strain, 2021 - 2034 (USD Billion) (Kilo Liters)

- 6.1 Key trends

- 6.2 Lactobacillus

- 6.3 Bifidobacterium

- 6.4 Streptococcus

- 6.5 Bacillus

- 6.6 Saccharomyces

- 6.7 Multi-strain formulations

Chapter 7 Market Estimates and Forecast, By Packaging Type, 2021 - 2034 (USD Billion) (Kilo Liters)

- 7.1 Key trends

- 7.2 Bottles

- 7.3 Cartons

- 7.4 Cans

- 7.5 Pouches

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Target Consumer Group, 2021 - 2034 (USD Billion) (Kilo Liters)

- 8.1 Key trends

- 8.2 General adult population

- 8.3 Children and Adolescents

- 8.4 Elderly population

- 8.5 Athletes and fitness enthusiasts

- 8.6 Health-conscious consumers

Chapter 9 Market Estimates and Forecast, By Consumption Occasion, 2021 - 2034 (USD Billion) (Kilo Liters)

- 9.1 Key trends

- 9.2 Daily consumption

- 9.3 Meal replacement

- 9.4 On-the-Go consumption

- 9.5 Post-exercise recovery

Chapter 10 Market Estimates and Forecast, By Price Segment, 2021 - 2034 (USD Billion) (Kilo Liters)

- 10.1 Key trends

- 10.2 Economy / mass market

- 10.3 Mid-range

- 10.4 Premium / luxury

Chapter 11 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Kilo Liters)

- 11.1 Key trends

- 11.2 Supermarkets and hypermarkets

- 11.3 Convenience stores

- 11.4 Specialty health food stores

- 11.5 Pharmacy and drug stores

- 11.6 Online retail

- 11.7 Foodservice sector

Chapter 12 Market Estimates and Forecast, By Sales Channel, 2021 - 2034 (USD Billion) (Kilo Liters)

- 12.1 Key trends

- 12.2 B2B

- 12.3 B2C

Chapter 13 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Liters)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Spain

- 13.3.5 Italy

- 13.3.6 Netherlands

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 Australia

- 13.4.5 South Korea

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.6 Middle East and Africa

- 13.6.1 Saudi Arabia

- 13.6.2 South Africa

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Yakult Honsha Co., Ltd.

- 14.2 Danone S.A.

- 14.3 Nestle S.A.

- 14.4 PepsiCo, Inc.

- 14.5 Coca-Cola Company

- 14.6 Lifeway Foods, Inc.

- 14.7 Harmless Harvest

- 14.8 KeVita (PepsiCo)

- 14.9 GoodBelly (NextFoods)

- 14.10 Chobani, LLC

- 14.11 Groupe Lactalis

- 14.12 Bio-K Plus International Inc.

- 14.13 Fonterra Co-operative Group Juicery