|

市場調査レポート

商品コード

1892816

うっ血性心不全治療薬市場機会、成長要因、業界動向分析、および2025年から2034年までの予測Congestive Heart Failure Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| うっ血性心不全治療薬市場機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年12月12日

発行: Global Market Insights Inc.

ページ情報: 英文 139 Pages

納期: 2~3営業日

|

概要

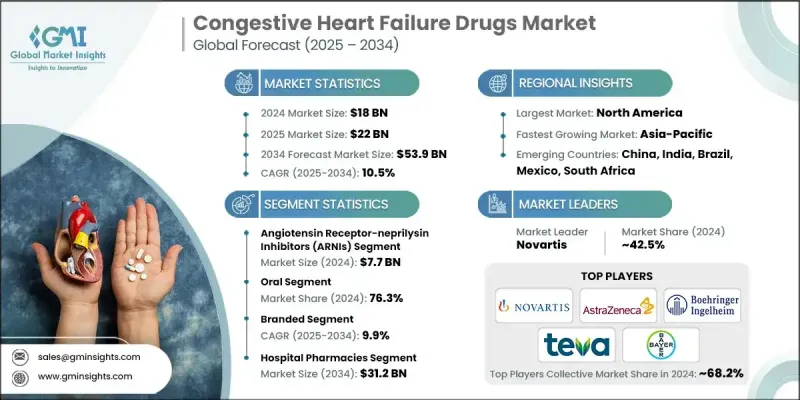

世界のうっ血性心不全治療薬市場は、2024年に180億米ドルと評価され、2034年までにCAGR10.5%で成長し、539億米ドルに達すると予測されております。

市場成長は、心不全の有病率上昇、医薬品開発の進歩、およびガイドラインに基づく薬物療法の拡大によって牽引されています。ACE阻害薬、β遮断薬、利尿薬などの確立された治療法に加え、SGLT2阻害薬やARNIsなどの新規薬剤クラスの採用拡大により、生存率が向上し入院が減少しているため、対象患者層が拡大しています。遠隔医療と遠隔モニタリングの統合が進むことで、早期介入、より厳密な治療最適化、長期的な服薬遵守の向上が可能となり、急性期・慢性期ケア環境を問わず薬剤利用が促進されています。製薬企業はまた、パイプラインの革新、併用療法、より広範な心不全表現型への適応拡大に注力しており、予測期間中の市場成長をさらに加速させています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025-2034 |

| 開始時価値 | 180億米ドル |

| 予測金額 | 539億米ドル |

| CAGR | 10.5% |

うっ血性心不全治療薬市場は、主に投与経路によって区分されており、2024年には経口投与セグメントが76.3%を占めました。経口療法は、その利便性、自己投与の容易さ、投与コストの低さ、そして慢性心不全の長期的な在宅管理への適性から好まれています。徐放性製剤、1日1回投与製剤、固定用量配合剤は複雑な治療計画を簡素化し、複数の併存疾患を管理する患者の服薬遵守率と治療成果を向上させます。さらに、ACE阻害薬、β遮断薬、SGLT2阻害薬などの強力な経口薬剤の普及拡大は、外来診療および遠隔医療を活用したケアモデルの両方において、このセグメントの優位性を強化しています。

流通チャネル別では、急性心不全症例の高負担(集中的なプロトコルに基づく治療を必要とする)を背景に、2024年に病院薬局セグメントは312億米ドルの市場規模を生み出しました。これらの施設では、静脈内強心薬、利尿薬、ARNIs(アルギニルリシンヌクレオチド分解酵素阻害薬)やSGLT2阻害薬などの先進治療を複雑に組み合わせた管理が行われ、多大な薬剤消費を牽引するとともに、治療開始と最適化における重要な拠点としての病院薬局の地位を確立しています。

北米のうっ血性心不全治療薬市場は2024年に53.9%のシェアを占めました。この優位性は、診断済み患者数の多さ、革新的治療法の早期導入、強力な償還制度、そしてガイドライン更新と新分子導入を加速させる堅固な臨床研究インフラによって支えられています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 心不全の有病率の増加

- 医薬品開発の進展

- 意識向上とスクリーニングの推進

- 業界の潜在的リスク&課題

- 厳格な規制承認

- 先進医療の高コスト

- 業界の潜在的リスク&課題

- 新規薬剤クラスの開発

- 慢性心不全管理のための遠隔医療と遠隔モニタリングの統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 米国

- カナダ

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 北米

- 技術環境

- 現在の技術動向

- 新興技術

- パイプライン分析

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

第5章 市場推計・予測:薬剤クラス別、2021-2034

- 主要動向

- ACE阻害薬

- β遮断薬

- 利尿薬

- アンジオテンシンII受容体拮抗薬

- ミネラルコルチコイド受容体拮抗薬(MRA)

- アンジオテンシン受容体ーネプリライシン阻害薬(ARNI)

- 強心薬

- SGLT2阻害薬

- その他の薬剤分類

第6章 市場推計・予測:投与経路別、2021-2034

- 主要動向

- 経口投与

- 非経口

第7章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- ブランド品

- ジェネリック

第8章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 病院薬局

- 小売薬局

- オンライン薬局

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Alnylam Pharmaceuticals

- Amgen

- AstraZeneca

- Bayer

- Boehringer Ingelheim International

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- GlaxoSmithKline

- Johnson &Johnson

- Merck

- Novartis

- Otsuka Pharmaceutical

- Pfizer

- Sanofi

- Teva Pharmaceutical Industries