SGLT2阻害薬の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

SGLT2 Inhibitors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750339

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

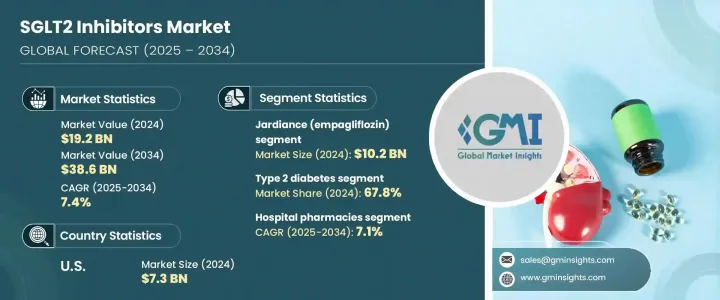

世界のSGLT2阻害薬市場は、2024年には192億米ドルと評価され、CAGR 7.4%で成長し、2034年には386億米ドルに達すると推定されています。

これは、運動不足、高齢化、肥満率の上昇などのライフスタイル要因によって数百万人が罹患している2型糖尿病の世界の有病率の増加が牽引しています。糖尿病治療薬は、血糖値を下げるだけでなく、特に心血管や腎臓に合併症を持つ患者に対して複数の利点をもたらすため、治療薬として際立っています。慢性的な健康状態の管理における役割の拡大は、患者層を大きく広げています。

SGLT2阻害薬は、従来の糖尿病治療薬とは異なり、腎臓からのグルコース排泄を促進することによりグルコースレベルを低下させるため、血糖コントロールをサポートするだけでなく、心血管や腎臓の保護にも貢献します。そのため、患者にもヘルスケアプロバイダーにも好まれる選択肢となっています。心不全や腎臓病患者における入院率や死亡率の減少を示す臨床試験のエビデンスが蓄積されるにつれ、これらの薬剤は、治療効果や患者のコンプライアンスを向上させるために、併用療法の一環として使用されることが多くなっています。さらに、製薬研究の継続的な進歩が技術革新をさらに加速し、製品の有効性を高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 192億米ドル |

| 予測金額 | 386億米ドル |

| CAGR | 7.4% |

2024年には、2型糖尿病管理セグメントが67.8%のシェアを占める。このセグメントの優位性は、糖尿病の負担が増大する中、効果的な解決策が緊急に必要とされていることを反映しています。特筆すべきは、治療効果を高めるために、多くの医師が他の経口糖尿病治療薬とともにこれらの阻害剤を処方することを好むようになったことです。複数の疾患因子に同時に対処できることから、現代糖尿病管理の要となっています。

世界の市場セグメンテーション市場は、流通チャネル別に病院薬局、小売薬局、オンライン薬局に区分されます。2024年現在、病院薬局セグメントは2025年から2034年にかけてCAGR 7.1%で成長すると予測され、これは入院患者および外来患者を対象に専門的な治療ソリューションを提供する中心的な役割を担っていることが背景にあります。病院薬局の支配的な地位は、調整されたケア経路をサポートし、臨床転帰を改善する高度な薬局サービスの統合に由来します。これらの薬局は、入院患者の服薬管理において重要な役割を果たしており、特に急性期医療の現場では、処方された治療薬をタイムリーに投与することを保証しています。

米国のSGLT2阻害薬2024年の市場シェアは41.1%で、2034年までCAGR 7.2%で成長します。米国は2034年に73億米ドルを創出。同国の成長軌道を支えているのは、強固なヘルスケア・インフラ、患者による治療への広範なアクセス、処方箋の採用を促す強力な償還政策です。一方、欧州とアジア太平洋市場は、診断率の向上、医療投資の増加、革新的治療への幅広いアクセスにより、大きな牽引力を見せています。

世界のSGLT2阻害薬業界では、メルク、ルピン・リミテッド、グレンマーク・ファーマシューティカルズ、アステラス製薬、ベーリンガー・インゲルハイム・インターナショナル、レキシコン・ファーマシューティカルズ、アストラゼネカ、ジョンソン・エンド・ジョンソン(ヤンセン・ファーマシューティカルズ)、サノフィ、イーライリリー・アンド・カンパニー、セラコスバイオ、ブリストル・マイヤーズスクイブ・カンパニーなどが有力なプレーヤーです。SGLT2阻害薬の世界市場における地位を強化するため、各社は戦略的パートナーシップや共同マーケティング契約、臨床適応の拡大などに積極的に投資しています。北米と欧州の大手企業は、研究開発パイプラインを活用し、糖尿病だけでなく心不全や腎臓病もターゲットにした先進的な製剤を開発しています。アジア太平洋地域の企業は、需要の増加に対応するため、製造能力を拡大し、販売提携を結んでいます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 2型糖尿病の有病率の上昇

- 治療適応の拡大

- 経口療法に対する患者の嗜好の増加

- 業界の潜在的リスク&課題

- 薬に伴う副作用

- 代替療法との競合

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 将来の市場動向

- パイプライン分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:薬剤クラス別、2021年~2034年

- 主要動向

- ジャディアンス(エンパグリフロジン)

- フォシーガ(ダパグリフロジン)

- インボカナ(カナグリフロジン)

- インペファ(ソタグリフロジン)

- Qtern(ダパグリフロジン/サキサグリプチン)

- その他のSGLT2阻害薬

第6章 市場推計・予測:適応症別、2021年~2034年

- 主要動向

- 2型糖尿病

- 心血管疾患

- 慢性腎臓病(CKD)

- その他の適応症

第7章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 病院薬局

- 小売薬局

- オンライン薬局

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Astellas

- AstraZeneca

- Boehringer Ingelheim International

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- Glenmark Pharmaceuticals

- Johnson &Johnson(Janssen Pharmaceuticals)

- Lexicon Pharmaceuticals

- Lupin Limited

- Merck

- Sanofi

- TheracosBio

目次

The Global SGLT2 Inhibitors Market was valued at USD 19.2 billion in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 38.6 billion by 2034, driven by the increasing global prevalence of type 2 diabetes, a condition affecting millions due to lifestyle factors such as physical inactivity, aging populations, and rising obesity rates. These medications stand out in the therapeutic landscape because they offer multiple benefits beyond lowering blood sugar, particularly for patients with cardiovascular and renal complications. Their expanding role in managing chronic health conditions has significantly broadened their patient base.

Unlike traditional diabetes medications, SGLT2 inhibitors reduce glucose levels by promoting glucose excretion through the kidneys, which not only supports glycemic control but also contributes to cardiovascular and kidney protection. This makes them a preferred option among both patients and healthcare providers. With mounting evidence from clinical studies showing reduced hospitalization rates and mortality in heart failure and kidney disease patients, these drugs are increasingly used as part of combination therapies to improve treatment efficacy and patient compliance. Additionally, ongoing advancements in pharmaceutical research are further accelerating innovation and enhancing product effectiveness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $19.2 Billion |

| Forecast Value | $38.6 Billion |

| CAGR | 7.4% |

In 2024, the segment for managing type 2 diabetes held a 67.8% share. The dominance of this segment reflects the urgent need for effective solutions amid the growing diabetes burden. Notably, many physicians now favor prescribing these inhibitors alongside other oral antidiabetic agents to amplify therapeutic outcomes. Their ability to address multiple disease factors simultaneously has made them a cornerstone of modern diabetes management.

By distribution channel, the global SGLT2 inhibitors market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. As of 2024, the hospital pharmacies segment will grow at a CAGR of 7.1% from 2025-2034, driven by its central role in delivering specialized treatment solutions across inpatient and outpatient settings. The dominant position of hospital pharmacies stems from their integration of advanced pharmacy services that support coordinated care pathways and improve clinical outcomes. These pharmacies play a crucial role in medication management for hospitalized patients, ensuring the timely administration of prescribed therapies, especially in acute care settings.

United States SGLT2 Inhibitors Market held 41.1% share in 2024 and will grow at a 7.2% CAGR through 2034. United States generated USD 7.3 billion in 2034. The country's growth trajectory is supported by a robust healthcare infrastructure, widespread patient access to treatments, and strong reimbursement policies encouraging prescription adoption. Meanwhile, Europe and the Asia-Pacific markets are showing significant traction due to improved diagnosis rates, rising healthcare investments, and broader access to innovative therapies.

Prominent players in the Global SGLT2 Inhibitors Industry include Merck, Lupin Limited, Glenmark Pharmaceuticals, Astellas, Boehringer Ingelheim International, Lexicon Pharmaceuticals, AstraZeneca, Johnson & Johnson (Janssen Pharmaceuticals), Sanofi, Eli Lilly and Company, TheracosBio, and Bristol-Myers Squibb Company. To strengthen their position in the Global SGLT2 Inhibitors Market, companies are actively investing in strategic partnerships, co-marketing agreements, and expanding clinical indications. Major players in North America and Europe are leveraging R&D pipelines to develop advanced formulations targeting not just diabetes, but also heart failure and kidney disease. Firms in Asia-Pacific are expanding manufacturing capacities and forming distribution alliances to meet rising demand.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of type 2 diabetes

- 3.2.1.2 Expanding therapeutic indications

- 3.2.1.3 Increased patient preference for oral therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects associated with drugs

- 3.2.2.2 Competition from alternative therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Future market trends

- 3.7 Pipeline analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Jardiance (Empagliflozin)

- 5.3 Farxiga (Dapagliflozin)

- 5.4 Invokana (Canagliflozin)

- 5.5 Inpefa (Sotagliflozin)

- 5.6 Qtern (Dapagliflozin/Saxagliptin)

- 5.7 Other SGLT2 inhibitors

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Type 2 diabetes

- 6.3 Cardiovascular diseases

- 6.4 Chronic kidney disease (CKD)

- 6.5 Other indications

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 Online pharmacies

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Astellas

- 9.2 AstraZeneca

- 9.3 Boehringer Ingelheim International

- 9.4 Bristol-Myers Squibb Company

- 9.5 Eli Lilly and Company

- 9.6 Glenmark Pharmaceuticals

- 9.7 Johnson & Johnson (Janssen Pharmaceuticals)

- 9.8 Lexicon Pharmaceuticals

- 9.9 Lupin Limited

- 9.10 Merck

- 9.11 Sanofi

- 9.12 TheracosBio

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日