|

市場調査レポート

商品コード

1750328

ブローストレッチパッケージングフィルムの市場機会、成長促進要因、業界動向分析、2025年~2034年予測Blown Stretch Packaging Films Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ブローストレッチパッケージングフィルムの市場機会、成長促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年05月13日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

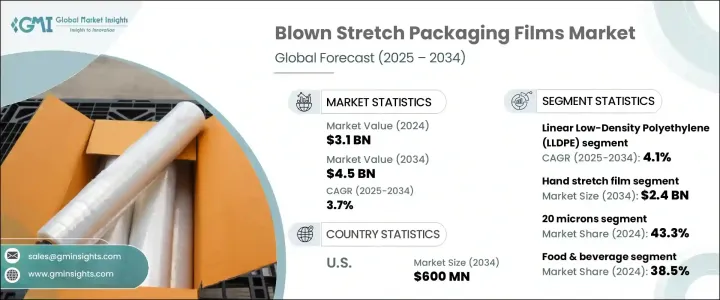

ブローストレッチパッケージングフィルムの世界市場は、2024年には31億米ドルと評価され、CAGR 3.7%で成長し、2034年には45億米ドルに達すると推定されています。

この成長は主に、飲食品分野を筆頭とする様々なパッケージング用途での需要増加が牽引しています。耐久性に優れ、柔軟で軽量な包装材料へのニーズが高まる中、ブローストレッチフィルムが大きな支持を得ています。これらのフィルムは優れた荷重安定性、製品保護、費用対効果を提供するため、包装の完全性と効率が重要な産業で不可欠なものとなっています。長年にわたり、経済的・政治的要因も市場情勢の形成に一役買ってきました。貿易制限や関税の変更は、特に投入コストの上昇によってサプライチェーンを圧迫しています。これに対応するため、メーカーは地政学的リスクを軽減し、事業の継続性を確保するために、地域に特化した生産戦略を採用するようになっています。このシフトは、企業が市場力学に迅速に適応できる地域に根ざしたエコシステムを構築することで、操業コストを削減し、サプライチェーンを確保し、利益率を守るのに役立ちます。

素材の種類は、市場の進化において重要な役割を果たしています。直鎖状低密度ポリエチレン(LLDPE)は、高い引張強度、柔軟性、耐パンク性などの優れた機械的特性により、市場の大部分を占めています。これらの特性により、LLDPEはストレッチフィルム製造、特に耐久性を損なうことなく材料使用量を削減するために薄いフィルムが必要な場合に好ましい選択肢となっています。LLDPE分野は2034年までにCAGR 4.1%で成長すると予測されているが、これは物流や消費財などの分野で、高性能でコスト効率の高いパッケージング・ソリューションに対する嗜好が高まっていることを反映しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 31億米ドル |

| 予測金額 | 45億米ドル |

| CAGR | 3.7% |

製品タイプ別では、ハンドストレッチフィルム、マシンストレッチフィルム、スペシャルティタイプがあります。このうち、ハンドストレッチフィルムは、その費用対効果と汎用性の高さから支持を集めています。ハンドストレッチフィルム分野は、手作業による包装に頼っている中小企業や倉庫業務での利用が増加していることを背景に、2034年までに24億米ドルに達すると予測されています。これらのフィルムは、特に自動化インフラが最小限の市場において、少量包装のニーズに実用的なソリューションを提供します。

厚みも需要に影響を与える重要なパラメーターです。2024年の市場シェアは、厚さ20ミクロンまでのフィルムが43.3%を占めています。このセグメントは、より軽い商品を包装するために、より薄いフィルムに目を向ける産業が増えるにつれて拡大しています。より薄いフィルムが好まれることで、包装廃棄物の削減、輸送コストの削減、持続可能性への取り組みが支援されます。

最終用途産業セグメンテーションでは、飲食品セクターが圧倒的な存在感を示しており、2024年の市場シェアは38.5%でした。ブローストレッチフィルムは、湿気や物理的ダメージから保護し、製品の賞味期限を延ばすことで、この業界で重要な役割を果たしています。保管中や輸送中に安全で衛生的な包装をサポートするその能力は、生鮮品に非常に適しています。消費者が安全で便利な包装を求めるようになっているため、この分野ではブローストレッチフィルムの採用が増え続けています。

流通チャネルも市場力学を形成しており、直販が2024年の総シェアの52%を占めてリードしています。直販により、メーカーはフィルムの厚み、引張強度、視覚的属性など、特定の顧客要件に合わせたカスタマイズされたパッケージング・ソリューションを提供できます。このアプローチは顧客との関係を強化し、シームレスなコミュニケーションを可能にし、より良いサービスと製品サポートを保証します。

地域別では、米国が力強い成長を遂げると予想されており、2034年までに市場は6億米ドルに達すると予測されています。特にeコマースの拡大や、安全で効率的な製品配送に対する消費者の期待の高まりにより、高性能食品包装材料への需要が高まっています。その結果、同市場では、製品の完全性を確保し、増大する物流ニーズをサポートするために、包装ソリューションの技術革新が進んでいます。

ブローストレッチパッケージングフィルム市場の競合環境は依然として激しく、大手企業は品質、イノベーション、持続可能性で競争しています。企業は、環境基準や消費者の嗜好を満たすため、生分解性フィルムや多層フィルム技術の開発に多額の投資を行っています。さらに、企業は市場での存在感を強め、技術力を向上させるため、戦略的な合併、買収、地域拡大に注力しています。また、サプライチェーンの効率を高め、安全性を確保するために、RFIDの統合や温度モニタリングなどのスマート・パッケージング・ソリューションへの関心も高まっています。医薬品、ロジスティクス、消費財といった対象業界向けのカスタマイズは、この進化する市場における差別化要因としてますます重要になってきています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 成長

- 寒冷地域での航空交通量の増加

- 厳格な航空安全規制

- 除氷技術の進歩

- 空港インフラの拡張

- 気候変動と厳しい冬

- 業界の潜在的リスク&課題

- 高い運用・保守コスト

- 環境と規制に関する懸念

- 成長

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- ハンドストレッチフィルム

- 機械ストレッチフィルム

- 特殊ストレッチフィルム

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 直鎖状低密度ポリエチレン(LLDPE)

- 低密度ポリエチレン(LDPE)

- 高密度ポリエチレン(HDPE)

- ポリプロピレン(PP)

- その他

第7章 市場推計・予測:厚さ別、2021-2034

- 主要動向

- 最大20ミクロン

- 21~40ミクロン

- 40ミクロン以上

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 食品・飲料

- 工業用包装

- 消費財

- 医薬品

- その他

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 販売業者/卸売業者

- オンラインチャネル

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- Berry Global Inc.

- AEP Industries Inc.

- Amcor Plc

- Coveris Holdings S.A.

- DUO PLAST AG

- Eurofilms Extrusion Ltd

- FlexSol Packaging Corp.

- Integrated Packaging Group Pty Ltd

- Intertape Polymer Group Inc.

- Manuli Stretch S.p.A.

- Megaplast India Pvt. Ltd.

- Mondi Group

- Paragon Films Inc.

- Polifilm GmbH

- RKW Group

- Sealed Air Corporation

- Sigma Plastics Group

- Trioplast Industrier AB

The Global Blown Stretch Packaging Films Market was valued at USD 3.1 billion in 2024 and is estimated to grow at a CAGR of 3.7% to reach USD 4.5 billion by 2034. This growth is primarily driven by increasing demand across various packaging applications, with the food and beverage sector at the forefront. As the need for durable, flexible, and lightweight packaging materials rises, blown stretch films have gained significant traction. These films offer superior load stability, product protection, and cost-effectiveness, making them essential in industries where packaging integrity and efficiency are vital. Over the years, economic and political factors have also played a role in shaping the market landscape. Trade restrictions and tariff changes have pressured the supply chain, particularly due to rising input costs. In response, manufacturers are adopting region-specific production strategies to reduce geopolitical risks and ensure business continuity. This shift helps companies lower operational costs, secure supply chains, and protect their profit margins by building localized ecosystems that can quickly adapt to market dynamics.

Material type plays a vital role in the market's evolution. Linear Low-Density Polyethylene (LLDPE) holds a significant portion of the market due to its outstanding mechanical properties, such as higher tensile strength, flexibility, and puncture resistance. These features make LLDPE a preferred choice for stretch film manufacturing, especially when thinner films are required to reduce material usage without compromising durability. The LLDPE segment is forecast to grow at a CAGR of 4.1% by 2034, reflecting the rising preference for high-performance and cost-efficient packaging solutions in sectors like logistics and consumer goods.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.1 Billion |

| Forecast Value | $4.5 Billion |

| CAGR | 3.7% |

In terms of product types, the market includes hand stretch films, machine stretch films, and specialty variants. Among these, hand stretch films are gaining traction due to their cost-effectiveness and versatility. The hand stretch film segment is projected to reach USD 2.4 billion by 2034, fueled by increasing usage among small to medium businesses and warehousing operations that rely on manual wrapping. These films provide a practical solution for low-volume packaging needs, especially in markets with minimal automation infrastructure.

Thickness is another key parameter influencing demand. Films with up to 20 microns in thickness accounted for a market share of 43.3% in 2024. This segment is expanding as more industries turn to thinner films to wrap lighter goods. The preference for lower thickness helps reduce packaging waste, cut transportation costs, and support sustainability efforts, which are increasingly important in modern supply chains.

The end-use industry segmentation shows a dominant presence in the food and beverage sector, which held a 38.5% market share in 2024. Blown stretch films serve a crucial role in this industry by offering protection against moisture and physical damage, extending product shelf life. Their ability to support secure and hygienic packaging during storage and transit makes them highly suitable for perishable goods. As consumers increasingly demand safe and convenient packaging, the adoption of blown stretch films continues to rise in this sector.

Distribution channels also shape the market dynamics, with direct sales leading the way by accounting for 52% of the total share in 2024. Direct sales allow manufacturers to provide customized packaging solutions tailored to specific customer requirements such as film thickness, tensile strength, or visual attributes. This approach strengthens client relationships and enables seamless communication, ensuring better service and product support.

In the regional landscape, the United States is expected to witness strong growth, with its market projected to hit USD 600 million by 2034. The demand for high-performance food packaging materials is rising, particularly due to expanding e-commerce and increased consumer expectations for safe and efficient product delivery. As a result, the market is seeing increased innovation in packaging solutions to ensure product integrity and support growing logistical needs.

The competitive environment in the blown stretch packaging films market remains intense, with leading players competing on quality, innovation, and sustainability. Companies are heavily investing in developing biodegradable and multi-layer film technologies to meet environmental standards and consumer preferences. In addition, firms are focusing on strategic mergers, acquisitions, and regional expansions to strengthen their market presence and improve technological capabilities. There is also growing interest in smart packaging solutions, including RFID integration and temperature monitoring, to enhance supply chain efficiency and ensure safety. Customization for targeted industries like pharmaceuticals, logistics, and consumer goods is becoming increasingly important as a differentiating factor in this evolving market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth

- 3.3.1.1.1 Growing air traffic in cold regions

- 3.3.1.1.2 Stringent aviation safety regulations

- 3.3.1.1.3 Advancements in de-icing technologies

- 3.3.1.1.4 Expansion of airport infrastructure

- 3.3.1.1.5 Climate variability and severe winters

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High operational and maintenance costs

- 3.3.2.2 Environmental and regulatory concerns

- 3.3.1 Growth

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Billion & kilo tons)

- 5.1 Key trends

- 5.2 Hand stretch film

- 5.3 Machine stretch film

- 5.4 Specialty stretch film

Chapter 6 Market Estimates and Forecast, By Material Type, 2021 – 2034 (USD Billion & kilo tons)

- 6.1 Key trends

- 6.2 Linear low-density polyethylene (LLDPE)

- 6.3 Low-density polyethylene (LDPE)

- 6.4 High-density polyethylene (HDPE)

- 6.5 Polypropylene (PP)

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Thickness, 2021-2034 (USD Billion & kilo tons)

- 7.1 Key trends

- 7.2 Up to 20 microns

- 7.3 21–40 microns

- 7.4 Above 40 microns

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Billion & kilo tons)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.3 Industrial packaging

- 8.4 Consumer goods

- 8.5 Pharmaceuticals

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 (USD Billion & kilo tons)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Distributors/wholesalers

- 9.4 Online channels

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion & kilo tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Berry Global Inc.

- 11.2 AEP Industries Inc.

- 11.3 Amcor Plc

- 11.4 Coveris Holdings S.A.

- 11.5 DUO PLAST AG

- 11.6 Eurofilms Extrusion Ltd

- 11.7 FlexSol Packaging Corp.

- 11.8 Integrated Packaging Group Pty Ltd

- 11.9 Intertape Polymer Group Inc.

- 11.10 Manuli Stretch S.p.A.

- 11.11 Megaplast India Pvt. Ltd.

- 11.12 Mondi Group

- 11.13 Paragon Films Inc.

- 11.14 Polifilm GmbH

- 11.15 RKW Group

- 11.16 Sealed Air Corporation

- 11.17 Sigma Plastics Group

- 11.18 Trioplast Industrier AB