|

市場調査レポート

商品コード

1928995

ストレッチフィルムおよびシュリンクフィルム市場における機会、成長要因、業界動向分析、ならびに2026年から2035年までの予測Stretch and Shrink Films Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| ストレッチフィルムおよびシュリンクフィルム市場における機会、成長要因、業界動向分析、ならびに2026年から2035年までの予測 |

|

出版日: 2026年01月15日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

概要

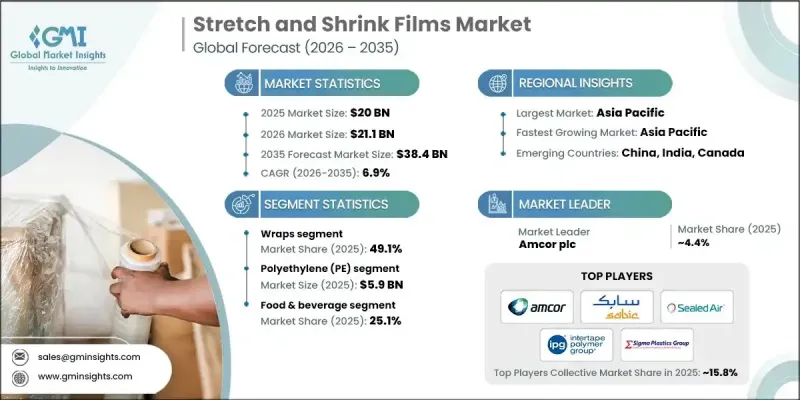

世界のストレッチフィルムおよびシュリンクフィルム市場は、2025年に200億米ドルと評価され、2035年までにCAGR 6.9%で成長し、384億米ドルに達すると予測されています。

市場成長は、循環型経済の実践の加速、リサイクル活動の増加、持続可能な包装ソリューションに対する規制当局の注目の高まりによって牽引されています。電子商取引と物流活動の急速な拡大は、輸送や保管中に商品を保護する耐久性があり軽量でコスト効率の高い包装材料の需要を大幅に押し上げています。食品保存分野での用途拡大と、スマート包装およびフィルム製造技術の進歩が相まって、市場の拡大をさらに後押ししています。環境意識の高まりとプラスチック廃棄物規制の強化により、メーカーは再生可能・生分解性・環境に配慮したフィルムソリューションの導入を促進しています。加えて、地域調達への志向の高まりと地域別持続可能性政策への適合がサプライチェーンの再構築を促しています。これらの動向は過去数年間で勢いを増しており、特に欧州と北米では規制圧力と消費者の嗜好変化により、環境配慮型包装の採用が加速しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 200億米ドル |

| 予測金額 | 384億米ドル |

| CAGR | 6.9% |

ラップセグメントは2025年に49.1%のシェアを占めました。このセグメントの需要は、食品、小売、オンライン流通チャネルにおいて製品の完全性を維持する、手頃な価格で保護性の高い包装ソリューションへのニーズによって支えられています。メーカーは、保護性、効率性、環境負荷低減のバランスが取れた高性能かつ持続可能なラップソリューションの開発をますます優先しています。

ポリエチレンセグメントは2025年に59億米ドルの売上を生み出しました。ポリエチレンフィルムは、その汎用性、耐久性、および複数の最終用途産業におけるコスト優位性から、引き続き広く採用されています。生産者は、フィルム品質の向上に注力すると同時に、リサイクル可能、堆肥化可能、および環境負荷の低い素材オプションの開発を進めています。

北米のストレッチフィルムおよびシュリンクフィルム市場は、2025年に30.2%のシェアを占めました。地域の成長は、活発な電子商取引活動、包装業務における自動化の進展、持続可能な包装導入を促進する規制枠組みによって牽引されています。環境に配慮した包装に対する消費者需要が、市場の勢いをさらに強めています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 循環型経済とリサイクル施策への注力

- 電子商取引および物流セクターの拡大

- 食品保存分野における応用拡大

- スマート包装ソリューションの台頭

- フィルム製造技術の進歩

- 業界の潜在的リスク&課題

- 代替包装材料との競合

- プラスチック使用削減に向けた規制圧力

- 市場機会

- 持続可能な包装ソリューション

- 生分解性フィルムの導入

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 新興ビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 消費者心理分析

- 地政学的・貿易動向

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 市場集中度分析

- 主要企業の競合ベンチマーキング

- 財務実績比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオ比較

- 製品ラインの幅広さ

- 技術

- イノベーション

- 地理的プレゼンス比較

- 世界展開分析

- サービスネットワークカバレッジ

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー企業

- 課題者

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績比較

- 主な発展, 2022-2025

- 合併・買収

- 提携および共同事業

- 技術的進歩

- 拡大と投資戦略

- サステナビリティ施策

- デジタルトランスフォーメーションの取り組み

新興企業/スタートアップ競合の動向

第5章 市場推計・予測:材料別、2022-2035

- ポリエチレン(PE)

- ポリ塩化ビニル(PVC)

- ポリプロピレン(PP)

- 生分解性および堆肥化可能

- その他

第6章 市場推計・予測:製品別、2022-2035

- フード

- スリーブおよびラベル

- ラップ

第7章 市場推計・予測:厚さタイプ別、2022-2035

- 超薄型/薄肉フィルム(5-15μm)

- 標準商業用フィルム(15-25μm)

- ヘビーデューティフィルム(25-50μm)

- 超厚手/特殊規格フィルム(50μm以上)

第8章 市場推計・予測:用途別、2022-2035

- 消費財

- 食品・飲料

- 工業用包装

- 物流・輸送

- 医薬品

- その他

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- 世界の主要企業

- Amcor plc

- Dow

- Sealed Air

- SABIC

- 地域別主要企業

- 北米

- Intertape Polymer Group Inc.

- Film Source Packaging

- Sigma Plastics Group

- アジア太平洋地域

- Scientex Berhad

- Shaktiman Packaging Pvt. Ltd.

- 欧州

- Klockner Pentaplast

- Bollore Inc.

- 北米

- ニッチプレイヤー/ディスラプター

- Balcan Innovations Inc.

- HIPAC Spa

- Italdibipack SpA

- RKW Group

- LyondellBasell Industries N.V.

- A-Z Packaging

- Paragon Films

- Coveris Holdings S.A.

- LUBAN PACK