|

市場調査レポート

商品コード

1750323

慢性疾患管理の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Chronic Disease Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 慢性疾患管理の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月14日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

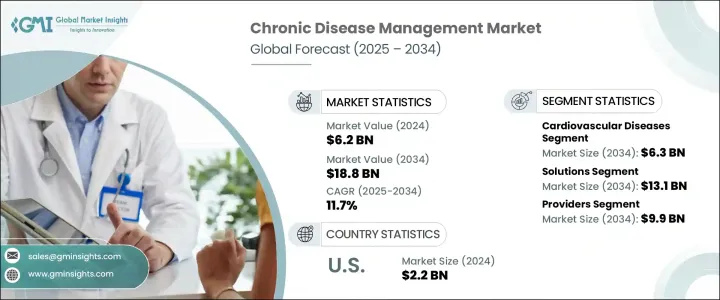

世界の慢性疾患管理市場は、2024年には62億米ドルと評価され、糖尿病、心血管疾患、高血圧などの慢性疾患の有病率の増加により、効果的な管理戦略が必要となり、CAGR 11.7%で成長し、2034年には188億米ドルに達すると推定されています。

さらに、遠隔医療サービス、遠隔監視装置、電子カルテなどのデジタル医療技術の進歩は、慢性医療の状況を一変させました。これらの技術的進歩は、ケアコーディネーションと臨床的意思決定を強化するだけでなく、疾病の進行を予防し、病院再入院を最小限に抑え、治療のアドヒアランスを高める予防的介入をサポートし、最終的には慢性期ケアの提供を変革し、システム全体の効率を高める。

さらに、ヘルスケアプロバイダーにリアルタイムのデータ洞察を提供し、患者とケアチーム間のコミュニケーションを合理化し、タイムリーな投薬調整を促進することで、より迅速で患者中心のケアと長期的な健康管理に貢献します。また、これらのツールは、複雑で長期にわたる病態を効果的に管理するために不可欠な自己モニタリング、教育、説明責任を促進することで、患者の関与を高める。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 62億米ドル |

| 予測金額 | 188億米ドル |

| CAGR | 11.7% |

心血管疾患分野は2024年に22億米ドルと評価され、2034年には63億米ドルに達すると予測されています。冠動脈疾患、心不全、高血圧などの疾患の罹患率が上昇しているため、包括的な管理ソリューションに対する需要が高まっています。テレヘルスプラットフォーム、ウェアラブルデバイス、遠隔モニタリングシステムは、血圧や心拍数などのバイタルサインを追跡し、タイムリーな介入を促進し、治療レジメンに対する患者のコンプライアンスを強化するのに役立ちます。

2024年には、プロバイダー部門が市場の53.8%を占め、市場を独占しており、2025年から2034年にかけてCAGR 11.5%で成長すると予測されています。病院、診療所、専門ケアセンターなどのヘルスケアプロバイダーは、慢性疾患管理サービスの中心的存在です。デジタルヘルス技術を統合することで、医療提供者は継続的な治療を提供し、患者の経過を監視し、必要に応じて治療計画を調整することができ、患者の転帰と満足度の向上につながります。

米国の慢性疾患管理市場は2024年に22億米ドルを占め、2025年から2034年にかけてCAGR 11.1%で成長すると予測されています。同国の高度なヘルスケアインフラ、デジタルヘルス技術の普及、支援的な償還政策がこの成長に寄与しています。米国の人口における慢性疾患の有病率の増加は、効果的な管理ソリューションの需要をさらに促進しています。

世界の慢性疾患管理市場の主な企業には、ResMed、Veradigm、IBM Corporation、Amwell、Oracle Corporation、Teladoc Health、Cerner Corporation、HealthSnap、Medtronic、Koninklijke Philips N.V.などがいます。これらの企業は、慢性疾患管理を強化する革新的なソリューションの開発に注力しています。遠隔医療サービスの拡大、予測分析のための人工知能の統合、ヘルスケアプロバイダーとのパートナーシップの形成などの戦略は、市場での存在感を強化するために採用されています。さらに、研究開発への投資は、患者のエンゲージメントと治療成果の向上を目指しており、これらの企業は進化するヘルスケアの展望の中で持続的な成長を目指しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患の有病率の上昇

- 遠隔医療と遠隔モニタリングの進歩

- 拡大するデジタルヘルス分野

- 革新的な解決策に対する政府の取り組みと資金提供

- 業界の潜在的リスク&課題

- 高い導入コスト

- データのプライバシーとセキュリティに関する懸念

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:疾患タイプ別、2021年~2034年

- 主要動向

- 心血管疾患(CVD)

- 糖尿病

- 慢性呼吸器肺疾患(COPD)

- がん

- 神経疾患

- その他の疾患タイプ

第6章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- ソリューション

- Webベースのソリューション

- クラウドベースのソリューション

- オンプレミスソリューション

- サービス

- 疾病管理プログラムとサービス

- 監視サービス

- カウンセリングとサポートサービス

- その他のサービスタイプ

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 提供者

- 支払者

- その他の用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Active Health Technologies

- Amwell

- Apollo TeleHealth

- Epic Systems

- HealthSnap

- IBM

- Koninklijke Philips N.V.

- Medicross

- Medtronic

- Oracle

- ResMed

- ScienceSoft USA

- Teladoc

- TimeDoc Health

- Topcon Healthcare

- Veradigm

- ZEISS

The Global Chronic Disease Management Market was valued at USD 6.2 billion in 2024 and is estimated to grow at a CAGR of 11.7% to reach USD 18.8 billion by 2034, driven by the increasing prevalence of chronic conditions such as diabetes, cardiovascular diseases, and hypertension, which necessitate effective management strategies. Additionally, advancements in digital health technologies, including telehealth services, remote monitoring devices, and electronic health records, have transformed the landscape of chronic care. These technological advancements not only enhance care coordination and clinical decision-making but also support proactive interventions that prevent disease progression, minimize hospital readmissions, and increase treatment adherence, ultimately transforming chronic care delivery and boosting system-wide efficiency.

Additionally, they empower healthcare providers with real-time data insights, streamline communication between patients and care teams, and facilitate timely medication adjustments, all of which contribute to more responsive, patient-centered care and long-term health management. These tools also foster greater patient engagement by promoting self-monitoring, education, and accountability, which are essential for managing complex, long-duration conditions effectively.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.2 Billion |

| Forecast Value | $18.8 Billion |

| CAGR | 11.7% |

The cardiovascular diseases segment was valued at USD 2.2 billion in 2024 and is anticipated to reach USD 6.3 billion by 2034. The rising incidence of conditions like coronary artery disease, heart failure, and hypertension has increased the demand for comprehensive management solutions. Telehealth platforms, wearable devices, and remote monitoring systems help in tracking vital signs such as blood pressure and heart rate, facilitating timely interventions, and enhancing patient compliance with treatment regimens.

In 2024, the providers segment dominated the market, accounting for 53.8% of the share, and is expected to grow at a CAGR of 11.5% from 2025 to 2034. Healthcare providers, including hospitals, clinics, and specialized care centers, are central to chronic disease management services. Integrating digital health technologies allows providers to offer continuous care, monitor patient progress, and adjust treatment plans as needed, leading to improved patient outcomes and satisfaction.

U.S. Chronic Disease Management Market accounted for USD 2.2 billion in 2024 and is projected to grow at a CAGR of 11.1% between 2025 and 2034. The country's advanced healthcare infrastructure, widespread adoption of digital health technologies, and supportive reimbursement policies contribute to this growth. The increasing prevalence of chronic conditions among the U.S. population further drives the demand for effective management solutions.

Key players in the Global Chronic Disease Management Market include ResMed, Veradigm, IBM Corporation, Amwell, Oracle Corporation, Teladoc Health, Cerner Corporation, HealthSnap, Medtronic, and Koninklijke Philips N.V. These companies are focusing on developing innovative solutions to enhance chronic disease management. Strategies such as expanding telehealth services, integrating artificial intelligence for predictive analytics, and forming partnerships with healthcare providers are being employed to strengthen their market presence. Additionally, investments in research and development aim to improve patient engagement and treatment outcomes, positioning these companies for sustained growth in the evolving healthcare landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic disease

- 3.2.1.2 Growing advancements in telehealth and remote monitoring

- 3.2.1.3 Expanding digital health sector

- 3.2.1.4 Government initiatives and funding for innovative solution

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation costs

- 3.2.2.2 Data privacy and security concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Disease Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Cardiovascular diseases (CVD)

- 5.3 Diabetes

- 5.4 Chronic respiratory pulmonary diseases (COPD)

- 5.5 Cancer

- 5.6 Neurological disorders

- 5.7 Other disease types

Chapter 6 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Solutions

- 6.2.1 Web-based solutions

- 6.2.2 Cloud-based solutions

- 6.2.3 On-premises solutions

- 6.3 Services

- 6.3.1 Disease management program and services

- 6.3.2 Monitoring services

- 6.3.3 Counseling and support services

- 6.3.4 Other service types

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Providers

- 7.3 Payers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Active Health Technologies

- 9.2 Amwell

- 9.3 Apollo TeleHealth

- 9.4 Epic Systems

- 9.5 HealthSnap

- 9.6 IBM

- 9.7 Koninklijke Philips N.V.

- 9.8 Medicross

- 9.9 Medtronic

- 9.10 Oracle

- 9.11 ResMed

- 9.12 ScienceSoft USA

- 9.13 Teladoc

- 9.14 TimeDoc Health

- 9.15 Topcon Healthcare

- 9.16 Veradigm

- 9.17 ZEISS