|

市場調査レポート

商品コード

1750320

アルミ箔の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Aluminum Foil Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| アルミ箔の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月16日

発行: Global Market Insights Inc.

ページ情報: 英文 225 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

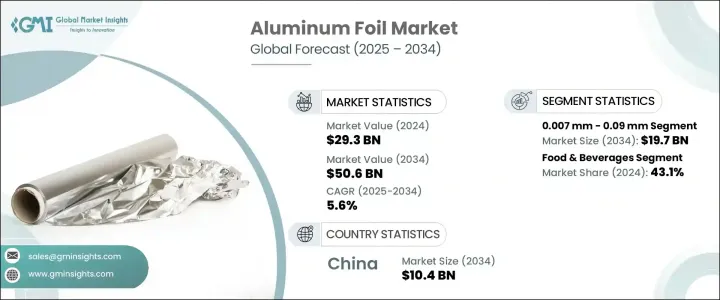

アルミ箔の世界市場は、2024年には293億米ドルとなり、CAGR 5.6%で成長し、2034年には506億米ドルに達すると推定されています。

この成長の主要因は、食品や医薬品の包装セグメントでの需要の増加、産業用断熱包装や自動車用遮熱材への用途の増加です。アルミ箔はその軽量性、強力なバリア性、リサイクル性で知られているため、特にサステイナブル材料への注目が世界的に高まるにつれて、最新の包装ソリューションにおける重要な材料となっています。開発途上国では、包装食品の消費急増が市場拡大にさらに貢献しており、メーカーやサプライヤーは進化する包装基準に対応する必要に迫られています。

環境規制や包装規制への対応、便利で使いやすい製品に対する消費者の嗜好、包装資材のリサイクル可能性への関心の高まりなど、さまざまな要因が重なってこの成長が加速しています。特に医薬品セグメントでは、製品の賞味期限や汚染防止に関する厳しい要件があるため、アルミ箔が重要な役割を果たしています。このような背景から、フォイルラミネートの需要は高まることが予想されます。さらに、技術の進歩が新たな市場機会を引き出しています。例えば、活性と生分解性箔ソリューション、ナノラミネート製品、箔ベースの複合材料などであり、これらすべてがより高い性能と持続可能性の利点を記載しています。一方、建築や自動車などの産業では、より軽量でエネルギー効率の高い材料への転換が進んでおり、包装以外のアルミ箔の用途がさらに広がっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 293億米ドル |

| 予測金額 | 506億米ドル |

| CAGR | 5.6% |

グリーンエネルギーを利用した製錬やリサイクル能力など、よりクリーンな生産プロセスに焦点を当てた投資も、環境負荷の低減に貢献しています。こうした取り組みはバリューチェーンを再構築し、アルミ箔製造業の全体的な持続可能性を高めると考えられます。各国が生産設備を近代化し、エコフレンドリー操業にシフトするにつれ、長期的な利益がこのセグメントの成長を支え続けると考えられます。

アルミ箔市場を厚さ別に分類すると、0.007mm~0.09mm、0.09mm~0.2mm、0.2mm~0.4mm、その他といったカテゴリーがあります。このうち、0.007mm~0.09mmセグメントが最大の収益シェアを占め、2024年には113億米ドルを生み出します。このセグメントは、CAGR 5.8%で成長し、2034年には197億米ドルに達すると予測されています。その優位性は、食品包装、医薬品、家庭用ラップ、産業用断熱材など、さまざまな用途に適応できることに起因します。費用対効果、バリア強度、柔軟性のバランスにより、消費者ニーズと商業ニーズの両方に好まれる選択肢となっています。特に、湿気、酸素、光から内容物を遮断する能力が高く評価されており、使い捨ての商品やリサイクル可能なフォーマットに最適です。

最終用途産業の観点から、市場は飲食品、医薬品、パーソナルケア・化粧品、家庭用、産業用、その他に分類されます。飲食品セグメントは2024年に最大のシェアを占め、世界市場収益の43.1%を占めました。このセグメントでの箔の広範な使用は、湿気、光、空気などの外部要素からの効果的な保護が原動力となっています。ホイルは保存期間を延長し、製品の鮮度を維持し、安全性を確保するのに役立ちます。箔は、軟質パウチ、蓋、容器、ラミネートラップなど、様々な消耗品に幅広く使用されています。

地域別では、中国の市場は2024年に59億米ドルの売上を記録し、CAGR 5.8%を記録して2034年には104億米ドルに達すると予測されています。中国は引き続き世界の生産量を独占しており、2025年までに世界のアルミ箔生産量の約60%を占めます。国内生産レベルも、消費拡大への広範な動向を反映して、大幅な伸びを示しています。過剰生産能力や環境問題などの課題に対応するため、国内は一次製錬事業の拡大から舵を切り、よりエコフレンドリー代替案へと移行しています。これには、再生可能エネルギーの利用やリサイクル能力の強化が含まれ、2027年までに年間1,500万トン以上のアルミニウムをリサイクルすることを目標としています。

世界のアルミ箔産業は、2024年時点で主要企業5社が合計40%以上の市場シェアを占め、緩やかな統合が続いています。多くの企業は、ヘルスケア、断熱材、エレクトロニクスなどの産業で高まる先進的フォイルタイプの需要に対応するため、新興市場に注力しています。この戦略的転換は、生産量の拡大だけでなく、エンボス加工、多層化、硬度向上などの機能を備えたプレミアムフォイルなど、製品提供の革新も重視しています。市場の進化に伴い、競合力学は持続可能性、技術革新、世界貿易の調整によって形成される可能性が高いです。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権の関税の影響-構造化された概要

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 産業への影響

- 供給側の影響(原料)

- 主要原料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原料)

- 影響を受ける主要企業

- 戦略的な産業対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 施策関与

- 展望と今後の検討事項

- 貿易への影響

- サプライヤーの情勢

- 利益率分析

- 主要ニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 原料価格の変動

- 代替包装材との競合

- 環境問題

- アルミニウムの浸出に関連する健康上の懸念

- 産業の潜在的リスク・課題

- 原料価格の変動

- 代替包装材との競合

- 環境問題

- アルミニウムの浸出に関連する健康上の懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

- バリューチェーン分析

- 原料サプライヤー

- アルミ箔メーカー

- コンバータとプロセッサ

- 販売代理店

- 最終用途

- 価格分析

- コスト構造分析

- 価格動向分析

- 価格予測

- 技術

- 製造プロセス概要

- 鋳造

- 熱間圧延

- 冷間圧延

- アニーリング

- 仕上げとスリット

- 技術的進歩

- アルミ箔生産の自動化

- 品質管理技術

- 製造プロセス概要

- 規制の枠組み

- 食品接触材料規制

- FDA規制(米国)

- EU規制

- その他の中東・アフリカ規制

- 環境規制

- 貿易施策と関税

- 規制が市場成長に与える影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推定・予測:厚さ別、2021~2034年

- 主要動向

- 0.007mm~0.09mm

- 0.09mm~0.2mm

- 0.2mm~0.4mm

- その他

第6章 市場推定・予測:箔タイプ別、2021~2034年

- 主要動向

- 印刷アルミ箔

- 非印刷アルミ箔

- ラミネート加工アルミ箔

- 裏地付きアルミ箔

- その他

第7章 市場推定・予測:用途別、2021~2034年

- 主要動向

- バッグ&ポーチ

- ラップ&ロール

- ブリスター

- 蓋

- ラミネートチューブ

- トレイ

- その他

第8章 市場推定・予測:最終用途産業別、2021~2034年

- 主要動向

- 飲食品

- ベーカリー&菓子類

- レディトゥイートミール

- 乳製品

- 飲料

- その他

- 医薬品

- ブリスター包装

- ストリップ包装

- その他

- パーソナルケア・化粧品

- 家庭用

- 産業用

- 断熱

- 電気用途

- その他

- その他

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第10章 企業プロファイル

- Alcoa Corporation

- Aleris Corporation

- Alufoil Products

- Amco India

- Amcor

- Assan Aluminyum

- China Hongqiao Group

- Constellium

- Ess Dee Aluminium

- Eurofoil

- Hindalco Industries

- Huawei Aluminum

- Norsk Hydro

- Novelis

- Reynolds Consumer Products

- Symetal Aluminium Foil Industry

- UACJ Corporation

- United Company RUSAL

- Xiamen Xiashun Aluminium Foil

- Zhejiang Junma Aluminium Industry

The Global Aluminum Foil Market was valued at USD 29.3 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 50.6 billion by 2034. This growth is primarily fueled by rising demand across the food and pharmaceutical packaging sectors, as well as increasing applications in industrial insulation and automotive thermal shielding. As aluminum foil is known for its lightweight nature, strong barrier properties, and recyclability, it has become a key material in modern packaging solutions, especially as the focus on sustainable materials gains momentum worldwide. In developing nations, the surge in consumption of packaged foods is further contributing to market expansion, pushing manufacturers and suppliers to meet evolving packaging standards.

A combination of factors is accelerating this growth, including compliance with environmental and packaging regulations, consumer preference for convenient and easy-to-use products, and growing attention to the recyclability of packaging materials. Particularly in the pharmaceutical space, aluminum foil plays a vital role due to strict requirements surrounding product shelf life and contamination prevention. The demand for foil laminates is expected to climb in this context. Additionally, technological advancements are unlocking new market opportunities, such as active and biodegradable foil solutions, nano-laminated products, and foil-based composites, all of which offer greater performance and sustainability benefits. Meanwhile, industries such as construction and automotive are turning to lighter, more energy-efficient materials, further widening the use of aluminum foil beyond packaging.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $29.3 Billion |

| Forecast Value | $50.6 Billion |

| CAGR | 5.6% |

Investments focused on cleaner production processes, such as green energy-powered smelting and recycling capabilities, are also contributing to reduced environmental impact. These efforts are likely to reshape the value chain, enhancing the overall sustainability of aluminum foil manufacturing. As countries modernize production facilities and shift toward eco-conscious operations, the long-term benefits will continue to support growth in the sector.

When segmented by thickness, the aluminum foil market includes categories such as 0.007 mm - 0.09 mm, 0.09 mm - 0.2 mm, 0.2 mm - 0.4 mm, and others. Among these, the 0.007 mm - 0.09 mm segment accounted for the largest revenue share, generating USD 11.3 billion in 2024. This segment is forecast to reach USD 19.7 billion by 2034, growing at a CAGR of 5.8%. Its dominance is attributed to its adaptability across various applications, including food packaging, pharmaceutical products, household wraps, and industrial insulation. The balance of cost-effectiveness, barrier strength, and flexibility makes it a preferred choice for both consumer and commercial needs. It is especially valued for its ability to shield contents from moisture, oxygen, and light, making it ideal for single-use items and recyclable formats.

In terms of end-use industries, the market is categorized into food and beverages, pharmaceuticals, personal care and cosmetics, household, industrial, and others. The food and beverages segment held the largest share in 2024, accounting for 43.1% of global market revenue. The widespread use of foil in this sector is driven by its effective protection against external elements such as moisture, light, and air. It helps extend shelf life, maintain product freshness, and ensure safety-key requirements in the packaged food industry. Foil finds extensive use in flexible pouches, lids, containers, and laminated wraps, serving a variety of consumable products.

Regionally, the market in China recorded a revenue of USD 5.9 billion in 2024 and is projected to reach USD 10.4 billion by 2034, registering a CAGR of 5.8%. China continues to dominate global production, accounting for roughly 60% of the world's aluminum foil output by 2025. Domestic production levels have also witnessed significant growth, reflecting a broader trend toward increased consumption. In response to challenges like overcapacity and environmental concerns, the country is steering away from expanding primary smelting operations and moving toward greener alternatives. These include utilizing renewable energy sources and enhancing recycling capabilities, with a targeted goal to recycle over 15 million tons of aluminum annually by 2027.

The global aluminum foil industry remains moderately consolidated, with five leading companies collectively holding over 40% market share as of 2024. Many businesses are focusing on emerging markets to meet the growing demand for advanced foil types across industries like healthcare, insulation, and electronics. This strategic shift emphasizes not just expansion in output but also innovation in product offerings, including premium foils with features like embossing, multi-layering, and increased hardness. As the market evolves, competitive dynamics are likely to be shaped by sustainability, technological innovation, and global trade alignment.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Impact of trump administration tariffs - structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Fluctuating raw material prices

- 3.7.1.2 Competition from alternative packaging materials

- 3.7.1.3 Environmental concerns

- 3.7.1.4 Health concerns related to aluminum leaching

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Fluctuating raw material prices

- 3.7.2.2 Competition from alternative packaging materials

- 3.7.2.3 Environmental concerns

- 3.7.2.4 Health concerns related to aluminum leaching

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Value chain analysis

- 3.11.1 Raw material suppliers

- 3.11.2 Aluminum foil manufacturers

- 3.11.3 Converters & processors

- 3.11.4 Distributors

- 3.11.5 End use

- 3.12 Pricing analysis

- 3.12.1 Cost structure analysis

- 3.12.2 Price trends analysis

- 3.12.3 Price forecast

- 3.13 Technology landscape

- 3.13.1 Manufacturing process overview

- 3.13.1.1 Casting

- 3.13.1.2 Hot rolling

- 3.13.1.3 Cold rolling

- 3.13.1.4 Annealing

- 3.13.1.5 Finishing & slitting

- 3.13.2 Technological advancements

- 3.13.3 Automation in aluminum foil production

- 3.13.4 Quality control technologies

- 3.13.1 Manufacturing process overview

- 3.14 Regulatory framework

- 3.14.1 Food contact materials regulations

- 3.14.2 Fda regulations (us)

- 3.14.3 Eu regulations

- 3.14.4 Other regional regulations

- 3.15 Environmental regulations

- 3.15.1 Trade policies & tariffs

- 3.15.2 Impact of regulations on market growth

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Thickness, 2021 - 2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 0.007 mm - 0.09 mm

- 5.3 0.09 mm - 0.2 mm

- 5.4 0.2 mm - 0.4 mm

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Foil Type, 2021 - 2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Printed aluminum foil

- 6.3 Unprinted aluminum foil

- 6.4 Laminated aluminum foil

- 6.5 Backed aluminum foil

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Bags & pouches

- 7.3 Wraps & rolls

- 7.4 Blisters

- 7.5 Lids

- 7.6 Laminated tubes

- 7.7 Trays

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.1.1 Food & beverages

- 8.1.2 Bakery & confectionery

- 8.1.3 Ready-to-eat meals

- 8.1.4 Dairy products

- 8.1.5 Beverages

- 8.1.6 Others

- 8.2 Pharmaceuticals

- 8.2.1 Blister packaging

- 8.2.2 Strip packaging

- 8.2.3 Others

- 8.3 Personal care & cosmetics

- 8.4 Household

- 8.5 Industrial

- 8.5.1 Heat insulation

- 8.5.2 Electrical applications

- 8.5.3 Others

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Alcoa Corporation

- 10.2 Aleris Corporation

- 10.3 Alufoil Products

- 10.4 Amco India

- 10.5 Amcor

- 10.6 Assan Aluminyum

- 10.7 China Hongqiao Group

- 10.8 Constellium

- 10.9 Ess Dee Aluminium

- 10.10 Eurofoil

- 10.11 Hindalco Industries

- 10.12 Huawei Aluminum

- 10.13 Norsk Hydro

- 10.14 Novelis

- 10.15 Reynolds Consumer Products

- 10.16 Symetal Aluminium Foil Industry

- 10.17 UACJ Corporation

- 10.18 United Company RUSAL

- 10.19 Xiamen Xiashun Aluminium Foil

- 10.20 Zhejiang Junma Aluminium Industry