電子飛行計器システムの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Electronic Flight Instrument System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 185 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750297

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

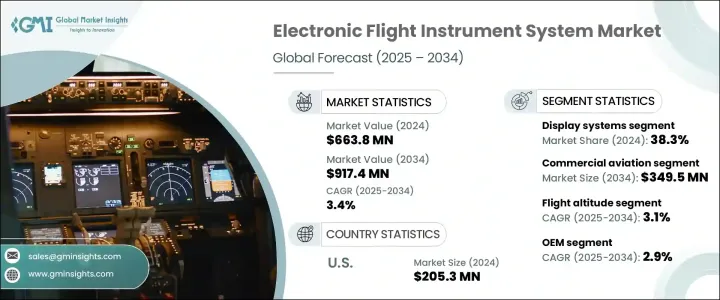

世界の電子飛行計器システム市場は、2024年には6億6,380万米ドルと評価され、民間航空機納入の急増、世界の航空旅行の増加、航空会社の機材更新の着実な増加により、CAGR 3.4%で成長し、2034年には9億1,740万米ドルに達すると予測されています。

航空交通量が増加し、運航会社が安全性と運航精度を優先するにつれて、リアルタイムで統合されたフライトデータへの需要が、新造機と改修機の両方でEFISの採用に寄与しています。これらのシステムは、飛行計画、燃料使用量、ナビゲーションを合理化し、より効率的で安全な運航を求める航空業界の動きに合致しています。

しかし、米国が航空宇宙・航空電子機器部品に課した関税により、市場は一時的な逆風に直面しました。この措置は国内メーカーのコストを大幅に引き上げ、サプライチェーンを混乱させ、最先端のフライトシステムの統合を遅らせました。一部のサプライヤーは、関税の影響を打ち消すために生産を現地化することで対応しましたが、価格設定と部品入手の不確実性により、民間部門と防衛部門の両方で短期的な市場減速につながりました。こうした課題にもかかわらず、航空利害関係者は引き続き航空電子機器のアップグレードを優先しており、特に進化する規制要件や安全義務に準拠したアップグレードを優先しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 6億6,380万米ドル |

| 予測金額 | 9億1,740万米ドル |

| CAGR | 3.4% |

コンポーネント別で、コントロールパネルセグメントは2025~2034年のCAGRが4.6%でした。高解像度のタッチスクリーンディスプレイ、再構成可能なレイアウト、モジュール式のハードウェア設計などの進歩により、コックピットの人間工学が向上し、パイロットのワークフローが合理化されています。これらのシステムは、リアルタイムのデータ統合やシームレスなインターフェイスのカスタマイズを可能にし、ミッションプロファイルや航空機のカテゴリーに対応しています。スマートアビオニクススイートおよび次世代飛行管理システムとの互換性の向上により、柔軟性と効率性が求められる多目的航空機での採用が特に促進されます。

民間航空分野は、2034年までに3億4,950万米ドルの売上が見込まれています。航空会社は、レガシーシステムを、リアルタイムの気象データ、高度な地形マッピング、交通の可視化をサポートする次世代EFISに置き換えつつあります。さらに、コスト効率への取り組みや燃料の最適化が、老朽化した航空機の改修を促しています。多くの航空会社は、安全マージンを改善し、飛行中にリアルタイムの洞察を提供する予測分析対応システムに移行しています。

米国は電子飛行計器システム(EFIS)の技術革新が牽引し、2024年の市場規模は2億530万米ドルとなりました。大規模な民間航空機改修プログラムと戦略的防衛アップグレードの組み合わせがこの分野の成長に寄与しています。政府主導の取り組みにより、状況認識、サイバー耐性、自律機能が強化され、デジタルコックピットソリューションへの投資が促進されます。

世界の電子飛行計器システム市場の主要企業には、BAE Systems、Aspen Avionics、Avidyne Corporation、Garmin、Genesys Aerosystems、Dynon Avionicsなどがあります。Dynon Avionics、Genesys Aerosystems、Avidyne Corporation、Garmin、Aspen Avionics、BAE Systemsなど、電子飛行計器システム市場で事業を展開する企業は、世界な事業展開を強化するためにいくつかの重要な戦略を採用しています。その多くは、有人および無人航空機をサポートするAI統合型およびモジュール型のEFISプラットフォームを構築するための研究開発に投資しています。OEMや規制機関とのコラボレーションは、進化する航空規格へのコンプライアンスの合理化に役立っています。メーカー各社は、カスタマイズ可能なインターフェースやタッチスクリーンパネルなど、ユーザー中心のイノベーションに注力し、民間、軍事、一般航空の各分野の需要に応えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 次世代航空機における先進的な航空電子機器の需要増加

- 民間航空機の納入と機体数の増加

- 航空旅客数の増加と航空会社の運航効率

- 統合航空電子機器アーキテクチャの採用増加

- 拡大する軍事・防衛航空部門

- 業界の潜在的リスク&課題

- 高額な初期投資と改修コスト

- 既存の航空電子機器システムとの複雑な統合

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:コンポーネント別、2021~2034年

- 主要動向

- ディスプレイシステム

- コントロールパネル

- 処理システム

- その他

第6章 市場推計・予測:プラットフォーム別、2021~2034年

- 主要動向

- 民間航空

- ナローボディ機

- ワイドボディ機

- リージョナルジェット機

- 軍事航空

- 戦闘機

- 輸送機および偵察機

- 軍用ヘリコプター

- ビジネスおよび一般航空

- 無人航空機(UAV)

第7章 市場推計・予測:用途別、2021~2034年

- 主要動向

- 飛行高度

- ナビゲーション

- 情報管理

- エンジン監視

- その他

第8章 市場推計・予測:最終用途別、2021~2034年

- 主要動向

- OEM(オリジナル機器メーカー)

- アフターマーケット(MROおよび航空電子機器アップグレード)

第9章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Aspen Avionics

- Avidyne Corporation

- BAE Systems

- Dynon Avionics

- Garmin

- Genesys Aerosystems

- Honeywell International

- Kanardia

- L3Harris Technologies

- LPP SRO

- Meggitt

- MGL Avionics

- Taskem Corporation

- Thales

- Universal Avionics

目次

The Global Electronic Flight Instrument System Market was valued at USD 663.8 million in 2024 and is estimated to grow at a CAGR of 3.4% to reach USD 917.4 million by 2034, driven by a surge in commercial aircraft deliveries, rising global air travel, and a steady increase in airline fleet upgrades. As air traffic grows and operators prioritize safety and operational precision, demand for real-time, integrated flight data is fueling the adoption of EFIS in both new aircraft and retrofits. These systems streamline flight planning, fuel usage, and navigation, aligning with the aviation industry's push for more efficient and secure flight operations.

However, the market faced temporary headwinds due to US-imposed tariffs on aerospace and avionics components. These measures significantly raised costs for domestic manufacturers, disrupting supply chains and delaying the integration of cutting-edge flight systems. Some suppliers responded by localizing production to counteract the tariff impact, but uncertainty in pricing and part availability led to short-term market slowdowns in both commercial and defense sectors. Despite these challenges, aviation stakeholders continue to prioritize avionics upgrades, especially those complying with evolving regulatory requirements and safety mandates.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $663.8 Million |

| Forecast Value | $917.4 Million |

| CAGR | 3.4% |

Within components, the control panels segment held a 4.6% CAGR during 2025-2034. Advancements such as high-resolution touch-screen displays, reconfigurable layouts, and modular hardware designs are enhancing cockpit ergonomics and streamlining pilot workflows. These systems allow real-time data integration and seamless interface customization, catering to mission profiles and aircraft categories. Enhanced compatibility with smart avionics suites and next-gen flight management systems fuels adoption, particularly in multi-role aircraft that demand flexibility and efficiency.

The commercial aviation segment is expected to generate USD 349.5 million by 2034. Airlines are replacing legacy systems with next-generation EFIS that support real-time weather data, advanced terrain mapping, and traffic visualization. In addition, cost-efficiency initiatives and fuel optimization prompt retrofitting across aging aircraft fleets. Many carriers are moving toward predictive analytics-enabled systems that improve safety margins and offer real-time insights during flight.

U.S. Electronic Flight Instrument System Market generated USD 205.3 million in 2024, driven by the innovation in electronic flight instrument systems (EFIS). A combination of large-scale commercial aircraft retrofitting programs and strategic defense upgrades contributes to the sector's growth. Government-driven initiatives enhance situational awareness, cyber-resilience, and autonomous capabilities, and foster increased investment in digital cockpit solutions.

Key players in Global Electronic Flight Instrument System Market include BAE Systems, Aspen Avionics, Avidyne Corporation, Garmin, Genesys Aerosystems, and Dynon Avionics. Companies operating in the electronic flight instrument system market-such as Dynon Avionics, Genesys Aerosystems, Avidyne Corporation, Garmin, Aspen Avionics, and BAE Systems-are adopting several key strategies to enhance their global footprint. Many are investing in R&D to create AI-integrated and modular EFIS platforms that support manned and unmanned aircraft. Collaborations with OEMs and regulatory bodies are helping streamline compliance with evolving aviation standards. Manufacturers focus on user-centric innovations such as customizable interfaces and touchscreen panels to meet demand across commercial, military, and general aviation sectors.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing demand for advanced avionics in next-generation aircraft

- 3.3.1.2 Rise in commercial aircraft deliveries and fleet expansion

- 3.3.1.3 Growth in air passenger traffic and airline operational efficiency

- 3.3.1.4 Increased adoption of integrated avionics architectures

- 3.3.1.5 Expanding military and defense aviation sector

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High initial investment and retrofit costs

- 3.3.2.2 Complex integration with existing avionics systems

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 Pestel analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Component, 2021-2034 (USD Million & units)

- 5.1 Key trends

- 5.2 Display systems

- 5.3 Control panels

- 5.4 Processing systems

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Platform Type, 2021-2034 (USD Million & units)

- 6.1 Key trends

- 6.2 Commercial aviation

- 6.2.1 Narrow-body aircraft

- 6.2.2 Wide-body aircraft

- 6.2.3 Regional jets

- 6.3 Military aviation

- 6.3.1 Fighter jets

- 6.3.2 Transport & reconnaissance aircraft

- 6.3.3 Military helicopters

- 6.4 Business & general aviation

- 6.5 Unmanned aerial vehicles (UAVs)

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & units)

- 7.1 Key trends

- 7.2 Flight altitude

- 7.3 Navigation

- 7.4 Information management

- 7.5 Engine monitoring

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million & units)

- 8.1 Key trends

- 8.2 OEM (original equipment manufacturer)

- 8.3 Aftermarket (MROs and avionics upgrades)

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Aspen Avionics

- 10.2 Avidyne Corporation

- 10.3 BAE Systems

- 10.4 Dynon Avionics

- 10.5 Garmin

- 10.6 Genesys Aerosystems

- 10.7 Honeywell International

- 10.8 Kanardia

- 10.9 L3Harris Technologies

- 10.10 LPP SRO

- 10.11 Meggitt

- 10.12 MGL Avionics

- 10.13 Taskem Corporation

- 10.14 Thales

- 10.15 Universal Avionics

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 185 Pages

- 納期

- 2~3営業日