自動車用キーインターロックケーブルの世界市場:機会、成長促進要因、業界動向分析、予測(2025年~2034年)

Automotive Key Interlock Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750262

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

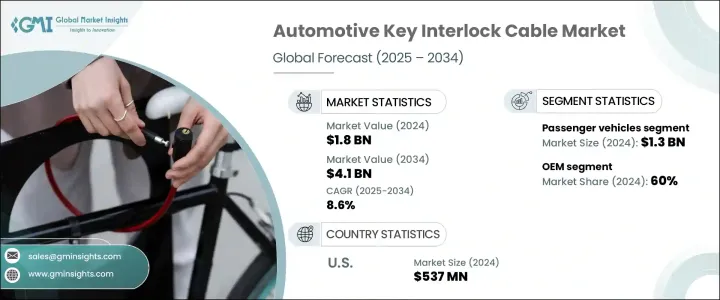

世界の自動車用キーインターロックケーブルの市場規模は、2024年に18億米ドルとなり、自動車の安全性に対する期待の高まり、オートマチックトランスミッションシステムの統合の進展、自動車分野における安全規制の厳格化などを背景に、CAGR8.6%で成長し、2034年には41億米ドルに達すると予測されます。 自動車メーカーは、意図しないギアシフトを防止し、安全性を高め、コンプライアンス要求を満たすために、高度なインターロック・システムを車両に組み込んでいます。

車両設計が高度化するにつれて、これらのケーブルは、特にギア操作をイグニッションの状態に関連付ける必要があるシステムにおいて、ドライバーの制御を確実にするための重要な部品としての役割を果たしています。これらのケーブルの採用は、電気自動車を含む商用車と乗用車の両セグメントで増加しています。

車両がADAS(先進運転支援システム)や半自動運転システムで進化し続ける中、高性能でコンパクト、かつ耐久性のあるキーインターロックソリューションへの需要が加速しています。これらのケーブルは、ギアシフト機能の信頼性の高い制御を提供し、潜在的な運転ミスを低減するため、安全性が重要な自動車システムに不可欠です。メーカーはまた、引張強度の強化や過酷な環境条件への耐性といった特徴にも注目しており、ケーブルがさまざまなストレス下で効率的に動作することを可能にしています。インターロック・システムは、さまざまなプラットフォームにおける最新の自動車アーキテクチャの要となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 18億米ドル |

| 予測金額 | 41億米ドル |

| CAGR | 8.6% |

乗用車セグメントは、2024年に13億米ドルを創出しました。これは、e-バイク、電動スクーター、小型電気自動車などの小型モビリティ・ソリューションに対する需要の高まりに牽引されたもので、その多くは安全性を高めるためのインターロックケーブルを備えています。軽量で折りたたみ可能な乗り物は、実用的で安全な移動手段を求める都市生活者や移動労働者の間で特に人気が高まっています。これらのインターロックケーブルは、未使用時の車両の移動を防止し、特に共有スペースでの盗難防止を強化することで、重要な役割を果たしています。

販売チャネルの観点から見ると、2024年の市場シェアの60%は相手先商標製品メーカー(OEM)が占めています。OEMはこの技術革新の最前線にあり、幅広い車種にキーインターロックケーブルを不可欠な部品として組み込んでいます。既存のシステムとのシームレスな互換性を提供し、信頼性の高い性能を確保する能力により、インターロックケーブルは最新の車両設計に不可欠な部品となっています。スマートで自動化されたロック機構の開発など、インターロック技術の絶え間ない進歩が、OEM供給ケーブルが好まれる要因となっています。

米国の自動車用キーインターロックケーブル市場は、強力な自動車部門、厳格な安全規制、電気自動車と自律走行車の高い採用率により、2024年に5億3,700万米ドルを創出しました。市場の拡大が続く中、米国メーカーはより先進的で耐久性があり効率的なインターロックシステムを開発するために研究開発に多額の投資を行っています。このような継続的な技術革新と、自動車の安全性向上を目的とした規制強化が相まって、米国が自動車用キーインターロックケーブル市場のリーダーであり続けることは確実です。

Suprajit、Orscheln、HI-Lex、Linamar、DURA、Ficosa、Kongsberg、Cablecraft、Kusterなどの主要企業は、戦略的提携、製品のカスタマイズ、生産拠点の拡大に注力することで、市場での地位を強化しています。これらの企業は、製品の寿命と進化する車両アーキテクチャとの互換性を向上させるための研究に投資する一方、OEMとのパートナーシップを活用して長期供給契約を確保しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 原材料供給業者

- 部品供給業者

- 製造業者

- テクノロジープロバイダー

- 流通チャネル分析

- 最終用途

- 利益率分析

- サプライヤーの情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- 規制情勢

- 価格動向

- 地域

- ケーブル

- コスト内訳分析

- 主なニュースと取り組み

- 影響要因

- 促進要因

- 車両安全規制の重要性の高まり

- オートマチックトランスミッション車の普及増加

- 電気自動車と自動運転車の成長

- ケーブル設計における技術的進歩

- 業界の潜在的リスクと課題

- 自動車産業のサイクルへの依存度が高め

- 原材料費の上昇

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:車両別(2021年~2034年)

- 主要動向

- 乗用車

- 商用車

- LCV

- MCV

- HCV

第6章 市場推計・予測:機能別(2021年~2034年)

- 主要動向

- 自動キーインターロック

- 手動キーインターロック

- リモートキーインターロック

第7章 市場推計・予測:ケーブル別(2021年~2034年)

- 主要動向

- 機械ケーブル

- 電気ケーブル

- ハイブリッドケーブル

- スマートケーブル

- カスタマイズケーブル

第8章 市場推計・予測:用途別(2021年~2034年)

- 主要動向

- 自動車セキュリティシステム

- イグニッションシステム

- トランスミッションシステム

- その他

第9章 市場推計・予測:販売チャネル別(2021年~2034年)

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別(2021年~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Aisin Seiki

- AutoCable

- Cablecraft Motion

- Curtiss-Wright

- DURA

- Shiloh

- Ficosa

- HI-Lex

- JOPP Automotive

- Kongsberg

- Kuster

- Linamar

- Ningbo Gaofa.

- Orscheln

- Shanghai Jinyi

- Sila Group

- Suprajit

- TOKAIRIKA

- Yazaki

- Zhejiang Sinyuan

目次

The Global Automotive Key Interlock Cable Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 4.1 billion by 2034, fueled by heightened vehicle safety expectations, the growing integration of automatic transmission systems, and stricter safety regulations in the automotive sector. Automakers are embedding advanced interlock systems into vehicles to prevent unintended gear shifts, enhancing safety and meeting compliance demands. As vehicle design becomes more sophisticated, these cables serve as crucial components for ensuring driver control, especially in systems where gear operation must be tied to ignition status. The adoption of these cables is growing in both commercial and passenger vehicle segments, including electric vehicles.

As vehicles continue to evolve with advanced driver-assist technologies and semi-autonomous systems, the demand for high-performance, compact, and durable key interlock solutions is accelerating. These cables offer reliable control over gear shift functions and reduce potential driver error, making them essential for safety-critical automotive systems. Manufacturers are also focusing on features such as enhanced tensile strength and resistance to harsh environmental conditions, allowing cables to operate efficiently under variable stresses. Interlock systems have become a cornerstone in modern vehicle architectures across various platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 8.6% |

The passenger vehicles segment generated USD 1.3 billion in 2024, driven by the rising demand for compact mobility solutions such as e-bikes, electric scooters, and small electric cars-many of which feature interlock cables for enhanced safety. Lightweight, foldable vehicles have become particularly popular among urban dwellers and mobile workers seeking practical, secure transportation. These interlock cables play a crucial role by preventing vehicle movement when not in use and offering additional theft protection, especially in shared spaces.

From a sales channel perspective, original equipment manufacturers (OEMs) held 60% of the market share in 2024, driven by the growing demand for enhanced vehicle safety and technological sophistication. OEMs are at the forefront of this innovation, integrating key interlock cables as integral components in a wide range of vehicle models. Their ability to provide seamless compatibility with existing systems and ensure reliable performance makes them an essential part of modern vehicle design. The constant advancements in interlock technology, including the development of smart and automated locking mechanisms, are contributing to the increased preference for OEM-supplied cables.

United States Automotive Key Interlock Cable Market generated USD 537 million in 2024 due to its strong automotive sector, rigorous safety regulations, and high adoption rates of electric and autonomous vehicles. As the market continues to expand, U.S. manufacturers are heavily investing in research and development to create more advanced, durable, and efficient interlock systems. This ongoing technological innovation, coupled with increased regulatory enforcement aimed at improving vehicle safety, ensures that the U.S. will remain a leader in the automotive key interlock cable market.

Key players such as Suprajit, Orscheln, HI-Lex, Linamar, DURA, Ficosa, Kongsberg, Cablecraft, Kuster, and Kongsberg (duplicate removed) are reinforcing their market position by focusing on strategic collaborations, product customization, and expanding their production footprint. These companies invest in research to improve product longevity and compatibility with evolving vehicle architectures while leveraging partnerships with OEMs to secure long-term supply agreements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.3.2 Pricing and product strategies

- 3.2.1 Impact on trade

- 3.3 Technology & innovation landscape

- 3.4 Patent analysis

- 3.5 Regulatory landscape

- 3.6 Price trend

- 3.6.1 Region

- 3.6.2 Cable

- 3.7 Cost breakdown analysis

- 3.8 Key news & initiatives

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising emphasis on vehicle safety regulations

- 3.9.1.2 Increased adoption of automatic transmission vehicles

- 3.9.1.3 Growth in electric and autonomous vehicles

- 3.9.1.4 Technological advancements in cable design

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High dependence on automotive industry cycles

- 3.9.2.2 Rising raw material costs

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Passenger vehicle

- 5.3 Commercial vehicles

- 5.3.1 LCV

- 5.3.2 MCV

- 5.3.3 HCV

Chapter 6 Market Estimates & Forecast, By Functionality, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Automatic key interlock

- 6.3 Manual key interlock

- 6.4 Remote key interlock

Chapter 7 Market Estimates & Forecast, By Cable, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Mechanical cables

- 7.3 Electrical cables

- 7.4 Hybrid cables

- 7.5 Smart cables

- 7.6 Customized cables

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Automotive security system

- 8.3 Ignition system

- 8.4 Transmission system

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 France

- 10.3.3 UK

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aisin Seiki

- 11.2 AutoCable

- 11.3 Cablecraft Motion

- 11.4 Curtiss-Wright

- 11.5 DURA

- 11.6 Shiloh

- 11.7 Ficosa

- 11.8 HI-Lex

- 11.9 JOPP Automotive

- 11.10 Kongsberg

- 11.11 Kuster

- 11.12 Linamar

- 11.13 Ningbo Gaofa.

- 11.14 Orscheln

- 11.15 Shanghai Jinyi

- 11.16 Sila Group

- 11.17 Suprajit

- 11.18 TOKAIRIKA

- 11.19 Yazaki

- 11.20 Zhejiang Sinyuan

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日