|

市場調査レポート

商品コード

1892897

歯内療法市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Endodontics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 歯内療法市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月10日

発行: Global Market Insights Inc.

ページ情報: 英文 145 Pages

納期: 2~3営業日

|

概要

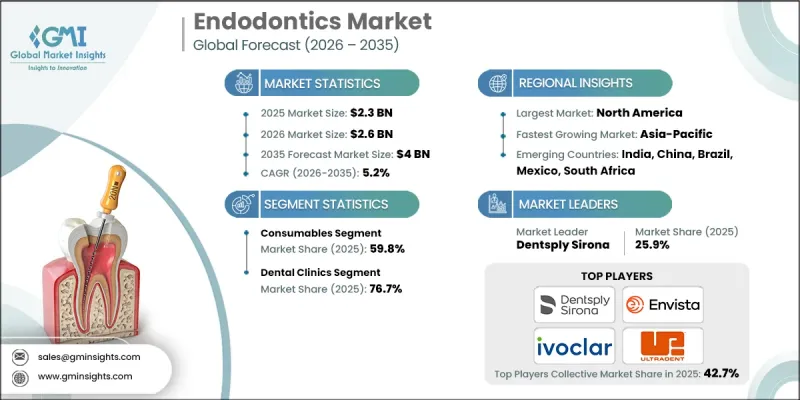

世界の歯内療法市場は、2025年に23億米ドルと評価され、2035年までにCAGR5.2%で成長し、40億米ドルに達すると予測されています。

市場拡大の背景には、歯内治療器具の急速な技術進歩、歯科健康に対する一般の意識向上、歯科疾患の増加傾向が挙げられます。世界的に歯科医療従事者や診療所の数が増加していることも需要を支えています。歯内療法は、主に根管治療を通じて歯髄および周辺組織の疾患を診断・治療する分野であり、感染の除去、痛みの緩和、天然歯の保存を目的としています。エンビスタ、デンツプライ・サイロナ、アイボクラール、ウルトラデント・プロダクツなどの主要企業は、技術革新、世界の流通網、研究開発への多額の投資を通じて市場での地位を維持しています。回転式歯内治療器具、アペックスロケーター、レーザー補助療法、3Dイメージングシステムなどの画期的な技術は、処置の精度、安全性、患者の快適性を向上させ、現代的な技術の普及を促進し、市場成長を加速させています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 23億米ドル |

| 予測金額 | 40億米ドル |

| CAGR | 5.2% |

2025年、消耗品セグメントは59.8%のシェアを占めました。頻繁な使用頻度、定期的な交換の必要性、そしてファイル、シーラー、充填材、洗浄液が全ての根管治療において不可欠な役割を果たすことから、安定した需要が維持されています。虫歯や歯髄感染の増加により世界的に根管治療の件数が増加する中、消耗品は引き続き最も購入されるカテゴリーであり続けています。

歯科医院セグメントは2025年に76.7%のシェアを占め、32億米ドルに達すると予測されています。歯科医院は根管治療の主要な診療拠点であり、虫歯や歯髄感染の蔓延による患者数の増加が歯内療法サービスの需要を押し上げています。

北米の歯内療法市場は2025年に37.7%のシェアを占め、生活習慣要因、糖分摂取、高齢化に伴う歯科疾患の高頻度が背景にあります。根管治療の需要は依然として高く、診療所全体での歯内療法器具および消耗品の持続的な使用を支えています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 歯科疾患の増加傾向

- 口腔衛生の重要性に対する認識の高まり

- 技術的進歩

- 業界の潜在的リスク&課題

- 発展途上地域や地方における高度な歯内療法へのアクセス制限

- 市場機会

- 新興市場およびサービスが行き届いていない市場への進出

- 痛みのない、低侵襲で患者中心の治療法への需要増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 技術動向

- 現在の技術動向

- 新興技術

- 消費者洞察

- 価格分析

- 将来の市場動向

- サプライチェーン分析

- ポーター分析

- PESTEL分析

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:タイプ別、2022-2035

- 消耗品

- ファイルおよびシェイパー

- 充填材

- 溶液および潤滑剤

- その他の消耗品

- 器具

- モーター

- アペックスロケーター

- 歯内治療用スケーラー

- 機械補助充填システム

- その他の器具

第6章 市場推計・予測:最終用途別、2022-2035

- 歯科医院

- 病院

- その他の用途

第7章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- BRASSELER

- COLTENE

- Dentsply Sirona

- DiaDent

- EdgeEndo

- Envista

- Essential Dental Systems

- FKG

- Ivoclar

- Kerr

- MANI

- Pac-Dent

- Septodent

- Shenzhen Perfect

- ULTRADENT