炭酸水素ナトリウムの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Sodium Bicarbonate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日

- 商品コード

- 1741037

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

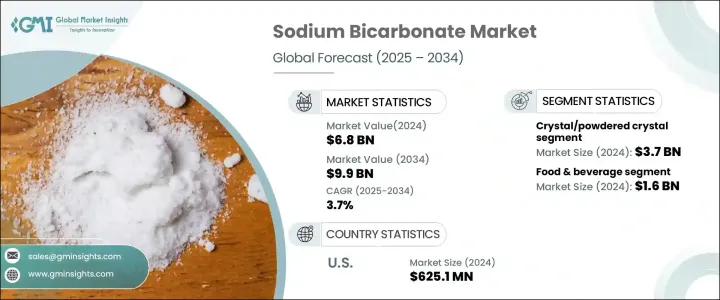

炭酸水素ナトリウムの世界市場規模は、2024年には68億米ドルとなり、産業用途の拡大と様々な分野における規制遵守の高まりが相まって、CAGR 3.7%で成長し、2034年には99億米ドルに達すると予測されています。

歴史的に、炭酸水素ナトリウムは医薬品、食品加工、環境ソリューションなど数多くの産業で定番であり続けてきました。炭酸水素ナトリウムの需要は、世界のサプライチェーンの不安定さによる混乱に直面しているにもかかわらず、多様な製造・加工業務において不可欠な役割を担っていることから、大きな回復力を示しています。

アジア太平洋、北米、欧州などの地域における需要の増加は、主に急速な工業化と環境意識の高まりによるものです。これらの地域では、進化する環境基準に合わせるための積極的な取り組みが行われており、その結果、炭酸水素ナトリウムに対する需要が持続しています。さらに、ヘルスケア製剤や医薬品のpH調整剤としての使用も、その関連性を高めています。また、炭酸水素ナトリウムが殺菌剤や栄養添加剤として使用されている農業や動物飼料分野でも、顕著な成長が見られます。このような力関係により、炭酸水素ナトリウムは世界のサプライチェーンと消費サイクルの中で確固たる地位を保っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 68億米ドル |

| 予測金額 | 99億米ドル |

| CAGR | 3.7% |

結晶および粉末結晶の市場情勢は、引き続き市場を独占しています。2024年の市場規模は37億米ドルで、2025年から2034年にかけてCAGR 4.2%で成長すると予測されています。粉末結晶の形態は、化学的安定性、保存の容易さ、保存期間の長さで際立っています。この形態は、一貫した品質と信頼性の高い処方が鍵となる食品製造、医薬品、パーソナルケアなどの分野で特に有利です。粉末状の炭酸水素ナトリウムは、細かく流動性のあるテクスチャーが好まれ、直接混合、効率的な包装、正確な製剤化に適しています。さらに、溶解性に優れ、粒子径が一定しているため、規制の厳しい産業での投与が簡素化されます。また、排煙脱硫におけるその有用性も、産業用途全体における需要を強化しています。

飲食品分野では、炭酸水素ナトリウムは2024年に16億米ドルの評価額を記録し、2025年から2034年までCAGR 4.1%で成長する見込みです。この分野は市場全体の約22.9%を占めています。製パン、加工食品、飲食品への炭酸水素ナトリウムの使用が増加していることは、重要な膨張剤およびpH調整剤としての役割を裏付けています。便利ですぐに食べられる健康志向の食品を求める消費者の増加により、メーカーは健康を損なうことなく製品の品質を向上させる原料を使用するようになっています。炭酸水素ナトリウムは、そのクリーンラベルの魅力と機能的な汎用性により、こうした嗜好によく合致しています。

米国の炭酸水素ナトリウム市場は、2024年に6億2,510万米ドルとなり、2034年までCAGR 3.5%で拡大すると予測されています。米国市場の開拓は、産業活動、規制の進展、継続的な経済発展によって大きく左右されます。政府の支援政策、確立された産業インフラ、厳しい環境規制と食品安全政策が安定した需要に寄与しています。パンデミック後の消費者行動の変化は、新たな産業投資と並んで成長をさらに後押ししています。ヘルスケアと利便性に特化した消費財の両分野で需要の増加が確認されており、世界情勢における日本の地歩を固めています。

競合情勢は、イノベーションと戦略的拡大を通じてより大きな市場シェアを確保しようとする主要企業によって支配されています。各社は製品ラインを多様化し、持続可能なソリューションに投資し、需要の高まりに対応するために世界のプレゼンスを強化しています。研究開発、特に製品の機能性と持続可能性の向上に向けた継続的な取り組みが、各社のポジショニングを変えています。特に、製品の革新、環境に配慮した製造方法、生産の最適化や合併による需要の高い地域への参入が、顕著に重視されています。市場力学が消費者動向や規制シフトによってますます形成される中、企業は競争力を維持し、世界のニーズに対応するために戦略を調整しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 供給側の影響(原材料)

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国、2021-2024

- 主要輸入国、2021-2024

- 製造プロセスとサプライチェーン分析

- 原材料分析

- 主要原材料

- 原材料調達

- 原材料価格動向

- 原材料サプライヤー

- 製造プロセス分析

- ソルベイ法

- トロナ法

- 炭酸ナトリウム法

- 水酸化ナトリウム法

- ナコライト抽出

- 新興生産技術

- コスト構造分析

- サプライチェーン分析

- サプライチェーンの構造とマッピング

- 流通チャネル分析

- 主要物流業者

- サプライチェーンの課題

- サプライチェーン最適化戦略

- 生産能力分析

- 世界の生産能力

- 稼働率

- 計画されている容量拡張

- 在庫管理と倉庫管理

- 品質管理と認証基準

- 原材料分析

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 世界的規制状況

- 食品グレード規制

- 医薬品グレード規制

- 産業グレードの規制

- 地域規制分析

- 北米

- 欧州

- アジア太平洋地域

- 世界のその他の地域

- 輸出入規制

- 製品の表示および包装規制

- 安全と取り扱いに関するガイドライン

- 環境規制

- 排出ガス規制

- 廃棄物管理規制

- 規制影響評価

- 生産コストへの影響

- 市場参入障壁への影響

- 製品開発への影響

- 世界的規制状況

- 影響要因

- 促進要因

- 製薬業界における需要の増加

- 食品・飲料分野での応用拡大

- 環境への懸念の高まりと環境に優しい製品の需要

- パーソナルケアおよび化粧品業界の成長

- 業界の潜在的リスク&課題

- 原材料の価格変動

- 生産プロセスに対する厳格な環境規制

- 促進要因

- 将来の市場見通しと戦略的機会

- 市場予測 2025~2034年

- 短期予測(1~3年)

- 中期予測(4~7年)

- 長期予測(8~10年)

- 新興市場の機会

- 高成長の応用分野

- 未開拓の地域市場

- ニッチセグメントの機会

- 戦略的成長機会

- 製品開発の機会

- 市場拡大の機会

- 付加価値サービスの機会

- テクノロジーの導入とイノベーションのロードマップ

- 持続可能性主導の機会

- 戦略的提言

- メーカー向け

- 販売代理店およびサプライヤー向け

- 最終用途向け

- 投資家向け

- 将来のシナリオ計画

- 楽観的シナリオ

- 現実的なシナリオ

- 悲観的なシナリオ

- 市場予測 2025~2034年

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- リスク分析と軽減戦略

- 市場リスク評価

- 需要変動リスク

- 価格変動リスク

- 競争リスク

- 代替リスク

- 運用リスク

- サプライチェーンの混乱

- 生産リスク

- 品質管理リスク

- 規制およびコンプライアンスリスク

- 環境と持続可能性のリスク

- 地政学的リスク

- リスク軽減戦略

- 多様化戦略

- ヘッジ戦略

- 保険とリスク移転の仕組み

- 緊急時対応計画

- 業界利害関係者向けのリスク管理フレームワーク

- 市場リスク評価

第5章 市場推計・予測:形態別、2021-2034

- 主要動向

- クリスタル/粉末クリスタル

- 液体

- スラリー

第6章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 食品・飲料

- 産業

- 医薬品

- パーソナルケア

- 農薬

- 動物飼料

- その他

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- Akshar Chemical India Private Limited

- Ciner Group

- Church &Dwight

- Crystal Mark

- FMC

- GHCL

- Haohua Honghe Chemical

- Natural Soda

- Opta Minerals

- Sisecam

- Solvay

- Tata Chemicals

- Tosoh

目次

The Global Sodium Bicarbonate Market was valued at USD 6.8 billion in 2024 and is estimated to grow at a CAGR of 3.7% to reach USD 9.9 billion by 2034, driven by a combination of expanding industrial applications and rising regulatory compliance across various sectors. Historically, sodium bicarbonate has remained a staple across numerous industries, including pharmaceuticals, food processing, and environmental solutions. Despite facing disruptions due to global supply chain instability, the demand for sodium bicarbonate displayed significant resilience, largely due to its indispensable role in diverse manufacturing and processing operations.

The increasing demand in regions such as Asia Pacific, North America, and Europe has primarily been driven by rapid industrialization and growing environmental awareness. These regions are taking proactive steps to align with evolving environmental standards, resulting in sustained demand for sodium bicarbonate. Additionally, the compound's use in healthcare formulations and as a pH control agent in medications continues to fuel its relevance. There has also been notable growth in the agriculture and animal feed sectors, where sodium bicarbonate is used both as a fungicide and nutritional additive. These dynamics collectively ensure that the product retains a strong foothold in global supply chains and consumption cycles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.8 Billion |

| Forecast Value | $9.9 Billion |

| CAGR | 3.7% |

The crystal and powdered crystal forms of sodium bicarbonate continue to dominate the market landscape. Valued at USD 3.7 billion in 2024, this segment is projected to grow at a CAGR of 4.2% between 2025 and 2034. The powdered crystal form stands out for its chemical stability, ease of storage, and longer shelf life. This format is particularly advantageous in sectors like food production, pharmaceuticals, and personal care, where consistent quality and reliable formulation are key. Powdered sodium bicarbonate is preferred for its fine, free-flowing texture, which makes it suitable for direct blending, efficient packaging, and precise formulation. Furthermore, it offers excellent solubility and consistent particle size, which simplifies dosing in tightly regulated industries. Its utility in flue gas desulfurization also strengthens its demand across industrial applications.

Within the food and beverage sector, sodium bicarbonate held a valuation of USD 1.6 billion in 2024, with expectations to grow at a 4.1% CAGR from 2025 to 2034. This segment accounts for approximately 22.9% of the total market share. The increasing incorporation of sodium bicarbonate in baking, processed foods, and beverages underscores its role as a vital leavening and pH-regulating agent. Rising consumer inclination toward convenient, ready-to-eat, and health-oriented food options is pushing manufacturers to use ingredients that enhance product quality without compromising health. Sodium bicarbonate aligns well with these preferences due to its clean-label appeal and functional versatility.

In the United States, the sodium bicarbonate market was valued at USD 625.1 million in 2024 and is projected to expand at a CAGR of 3.5% through 2034. Growth in the U.S. market is largely shaped by industrial activity, evolving regulations, and ongoing economic developments. Supportive government policies, an established industrial infrastructure, and stringent environmental and food safety regulations are contributing to steady demand. Post-pandemic shifts in consumer behavior, alongside new industrial investments, have further bolstered growth. There is an observable uptick in demand across both healthcare and convenience-focused consumer goods sectors, reinforcing the country's stronghold in the global landscape.

The competitive landscape is dominated by key players aiming to secure larger market shares through innovation and strategic expansion. Companies are diversifying product lines, investing in sustainable solutions, and strengthening their global presence to meet rising demand. Continuous efforts in research and development, particularly toward enhancing product functionality and sustainability, are reshaping how these companies position themselves. In particular, there is a noticeable emphasis on product innovation, eco-conscious manufacturing practices, and tapping into high-demand regions through production optimization and mergers. With market dynamics increasingly shaped by consumer trends and regulatory shifts, businesses are adjusting strategies to stay competitive and responsive to global needs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Demand-side impact (selling price)

- 3.2.3.1 Price transmission to end markets

- 3.2.3.2 Market share dynamics

- 3.2.3.3 Consumer response patterns

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries, 2021-2024 (kilo tons)

- 3.3.2 Major importing countries, 2021-2024 (kilo tons)

- 3.4 Manufacturing process and supply chain analysis

- 3.4.1 Raw materials analysis

- 3.4.1.1 Key raw materials

- 3.4.1.2 Raw material sourcing

- 3.4.1.3 Raw material price trends

- 3.4.1.4 Raw material suppliers

- 3.4.2 Manufacturing process analysis

- 3.4.2.1 Solvay process

- 3.4.2.2 Trona process

- 3.4.2.3 Sodium carbonate method

- 3.4.2.4 Sodium hydroxide method

- 3.4.2.5 Nahcolite extraction

- 3.4.2.6 Emerging production technologies

- 3.4.2.7 Cost structure analysis

- 3.4.3 Supply chain analysis

- 3.4.3.1 Supply chain structure and mapping

- 3.4.3.2 Distribution channels analysis

- 3.4.3.3 Key logistics providers

- 3.4.3.4 Supply chain challenges

- 3.4.3.5 Supply chain optimization strategies

- 3.4.4 Production capacity analysis

- 3.4.4.1 Global production capacity

- 3.4.4.2 Capacity utilization rates

- 3.4.4.3 Planned capacity expansions

- 3.4.5 Inventory management and warehousing

- 3.4.6 Quality control and certification standards

- 3.4.1 Raw materials analysis

- 3.5 Supplier landscape

- 3.6 Profit margin analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.8.1 Global regulatory landscape

- 3.8.1.1 Food grade regulations

- 3.8.1.2 Pharmaceutical grade regulations

- 3.8.1.3 Industrial grade regulations

- 3.8.2 Regional regulatory analysis

- 3.8.2.1 North America

- 3.8.2.2 Europe

- 3.8.2.3 Asia pacific

- 3.8.2.4 Rest of the world

- 3.8.3 Import-export regulations

- 3.8.4 Product labeling and packaging regulations

- 3.8.5 Safety and handling guidelines

- 3.8.6 Environmental regulations

- 3.8.6.1 Emission control regulations

- 3.8.6.2 Waste management regulations

- 3.8.7 Regulatory impact assessment

- 3.8.7.1 Impact on production costs

- 3.8.7.2 Impact on market entry barriers

- 3.8.7.3 Impact on product development

- 3.8.1 Global regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand in the pharmaceutical industry.

- 3.9.1.2 Expanding applications in food and beverage sectors.

- 3.9.1.3 Rising environmental concerns and demand for eco-friendly products.

- 3.9.1.4 Growth in the personal care and cosmetics industry.

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Price volatility of raw materials.

- 3.9.2.2 Stringent environmental regulations on production processes.

- 3.9.1 Growth drivers

- 3.10 Future market outlook and strategic opportunities

- 3.10.1 Market forecast 2025–2034

- 3.10.1.1 Short-term forecast (1–3 years)

- 3.10.1.2 Medium-term forecast (4–7 years)

- 3.10.1.3 Long-term forecast (8–10 years)

- 3.10.2 Emerging market opportunities

- 3.10.2.1 High-growth application areas

- 3.10.2.2 Untapped regional markets

- 3.10.2.3 Niche segment opportunities

- 3.10.3 Strategic growth opportunities

- 3.10.3.1 Product development opportunities

- 3.10.3.2 Market expansion opportunities

- 3.10.3.3 Value-added services opportunities

- 3.10.4 Technology adoption and innovation roadmap

- 3.10.5 Sustainability-driven opportunities

- 3.10.6 Strategic recommendations

- 3.10.7 For manufacturers

- 3.10.8 For distributors and suppliers

- 3.10.9 For end use

- 3.10.10 For investors

- 3.10.11 Future scenario planning

- 3.10.11.1 Optimistic scenario

- 3.10.11.2 Realistic scenario

- 3.10.11.3 Pessimistic scenario

- 3.10.1 Market forecast 2025–2034

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Risk analysis and mitigation strategies

- 4.5.1 Market risks assessment

- 4.5.1.1 Demand fluctuation risks

- 4.5.1.2 Price volatility risks

- 4.5.1.3 Competitive risks

- 4.5.1.4 Substitution risks

- 4.5.2 Operational risks

- 4.5.2.1 Supply chain disruptions

- 4.5.2.2 Production risks

- 4.5.2.3 Quality control risks

- 4.5.3 Regulatory and compliance risks

- 4.5.4 Environmental and sustainability risks

- 4.5.5 Geopolitical risks

- 4.5.6 Risk mitigation strategies

- 4.5.6.1 Diversification strategies

- 4.5.6.2 Hedging strategies

- 4.5.6.3 Insurance and risk transfer mechanisms

- 4.5.6.4 Contingency planning

- 4.5.7 Risk management framework for industry stakeholders

- 4.5.1 Market risks assessment

Chapter 5 Market Estimates & Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Crystal/powdered crystal

- 5.3 Liquid

- 5.4 Slurry

Chapter 6 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Food & beverage

- 6.3 Industrial

- 6.4 Pharmaceutical

- 6.5 Personal care

- 6.6 Agrochemical

- 6.7 Animal feed

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Akshar Chemical India Private Limited

- 8.2 Ciner Group

- 8.3 Church & Dwight

- 8.4 Crystal Mark

- 8.5 FMC

- 8.6 GHCL

- 8.7 Haohua Honghe Chemical

- 8.8 Natural Soda

- 8.9 Opta Minerals

- 8.10 Sisecam

- 8.11 Solvay

- 8.12 Tata Chemicals

- 8.13 Tosoh

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日