|

市場調査レポート

商品コード

1741034

医療用エレクトロニクス市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測Medical Electronics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 医療用エレクトロニクス市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月16日

発行: Global Market Insights Inc.

ページ情報: 英文 139 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

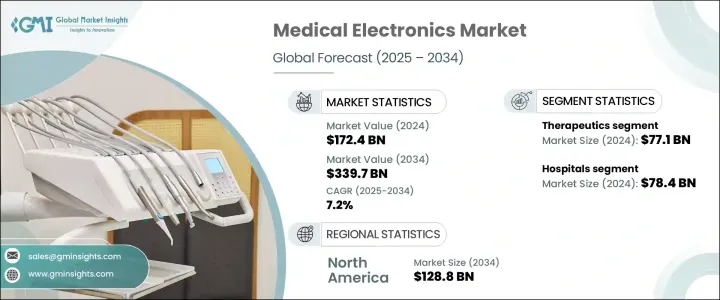

医療用エレクトロニクスの世界市場規模は、2024年に1,724億米ドルとなり、CAGR 7.2%で成長し、2034年には3,397億米ドルに達すると予測されています。

この成長の原動力は、診断、治療、予防、患者モニタリングをサポートするために、ヘルスケア分野全体で電子システムやデバイスの使用が拡大していることです。ヘルスケアのデジタル化が進むにつれて、情勢は臨床医がどのようにケアを提供するかに変化をもたらしています。画像診断ツールやウェアラブル・モニターから、ロボット手術システムやコネクテッド・セラピューティクスに至るまで、これらのデバイスは患者の経験や臨床結果を再構築しています。AI、IoT、クラウドコンピューティングのようなスマートテクノロジーの統合は、業務効率を再定義し、より迅速な診断を可能にし、データの精度を向上させ、人的ミスを減らしています。病院、診療所、そして在宅医療環境までもが、ワークフローの合理化、慢性疾患の管理、患者エンゲージメントの強化のために、相互接続された医療用エレクトロニクスに依存しています。世界の高齢化と非伝染性疾患の増加により、テクノロジー主導のヘルスケアソリューションへのシフトは明らかです。消費者は、パーソナライズされた、アクセスしやすい、リアルタイムのヘルスケアサービスを求めており、企業はより迅速な技術革新と、より直感的で信頼性の高い医療用電子機器の導入を推進しています。

心血管疾患、がん、呼吸器疾患などの慢性疾患や感染症の継続的な増加が、高度な医療用エレクトロニクスに対する需要の急増に大きく寄与しています。疾病の早期発見や予防医療に対する社会的意識が高まっており、診断技術の普及を後押ししています。同時に、低侵襲手術手技の進歩により、高精度の電子ツールへのニーズが加速しています。これらの技術革新は、リアルタイムの処置精度の向上、回復時間の短縮、患者の臨床転帰の向上に役立っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,724億米ドル |

| 予測金額 | 3,397億米ドル |

| CAGR | 7.2% |

この市場は、医療用ロボット、遠隔モニタリング、ウェアラブル診断などの分野で進行中の技術革新によっても力強い勢いを見せています。消費者がよりスマートでコネクテッドなヘルスケアツールに傾倒する中、医療用アプリケーションへのエレクトロニクスの統合は引き続き牽引役となっています。世界のヘルスケア支出の増加は、特に複雑な処置や長期ケアを管理するために設計された高度な電子機器の採用をさらに後押ししています。この動向は、リアルタイムのデータ、強化された画像処理、精密な制御に対する需要が依然として重要である特殊な医療分野で特に顕著です。

2024年、治療分野では、慢性的な症状を管理するための植え込み型および外付けデバイスの使用が増加していることが原動力となり、771億米ドルが創出されました。これらの治療技術は、高度な電子機能を組み合わせることで、安全性、送達精度、個別化治療を向上させる。ペースメーカー、神経刺激装置、輸液ポンプなどのデバイスは、生活の質を高め、通院を減らすために広く採用されています。

2024年には病院がエンドユーザーの採用をリードし、784億米ドルを稼ぎ出し、市場シェアの45.5%を占めました。これらの施設では、外来患者や入院患者の治療を効率的に管理するために、診断用と治療用の電子機器の両方に大きく依存しています。臨床ワークフローを最適化し、治療の遅れを最小化することに重点を置く病院は、より良い治療結果をもたらすために、次世代モニタリング機器、手術技術、画像処理システムへの投資を続けています。

米国医療用エレクトロニクス市場は、心血管疾患、糖尿病、がん、神経疾患などの慢性疾患の負担増に後押しされ、2023年に574億米ドルを創出しました。継続的なモニタリングと治療を必要とする患者の増加に伴い、高度な電子医療機器に対する需要は引き続き高いです。米国はまた、強力な研究開発インフラと早期の技術導入の恩恵を受けており、医療技術革新におけるリーダーシップを維持しています。

世界医療用エレクトロニクス市場の主要企業(オリンパス、Shenzhen Mindray Bio-医療用エレクトロニクス、シーメンス・ヘルスイニアーズ、Lepu Medical Technology、ボストン・サイエンティフィック、東芝メディカルシステムズ、富士フイルムホールディングス、GEヘルスケア、アボット・ラボラトリーズ、マイクロポート・サイエンティフィック、サムスン電子、メドトロニック、ケアストリームヘルス、Koninklijke Philips、Esaoteなど)は、市場での存在感を高めるために重要な戦略を実施しています。これには、イノベーションを迅速に進めるためのR&D投資の強化、リアルタイムのフィードバックを得るための医療提供者との連携、新興市場への進出、AIとIoTを活用したインテリジェント診断・遠隔ケアプラットフォームの立ち上げなどが含まれます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患と感染症の負担増大

- 先進技術の採用拡大医療用エレクトロニクス

- 低侵襲手術への嗜好の高まり

- 資本集約型機械のリース増加と外国直接投資(FDI)に関する重要な政策の開発

- 業界の潜在的リスク&課題

- 厳しい規制シナリオ

- 熟練したヘルスケア専門家の不足

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 国別の対応

- 業界への影響

- 供給側の影響(製造コスト)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(消費者のコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(製造コスト)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 技術的情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 治療薬

- ペースメーカー

- 植込み型除細動器

- 神経刺激装置

- 外科用ロボット

- 呼吸ケア機器

- 診断

- 患者モニタリング装置

- PET-CT装置

- MRIスキャナー

- 超音波装置

- X線装置

- CTスキャナー

- その他の製品タイプ

第6章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 外来手術センター

- クリニック

- その他の用途

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第8章 企業プロファイル

- Abbott Laboratories

- Boston Scientific

- Carestream Health

- Esaote

- FUJIFILM Holdings

- GE HealthCare

- Koninklijke Philips

- Lepu Medical Technology

- Medtronic

- MicroPort Scientific

- Olympus

- Samsung Electronics

- Shenzhen Mindray Bio-Medical Electronics

- Siemens Healthineers

- Toshiba Medical Systems

The Global Medical Electronics Market was valued at USD 172.4 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 339.7 billion through 2034. This growth is driven by the expanding use of electronic systems and devices across healthcare sectors to support diagnosis, treatment, prevention, and patient monitoring. As the healthcare landscape becomes increasingly digitized, medical electronics are transforming how clinicians deliver care. From diagnostic imaging tools and wearable monitors to robotic surgery systems and connected therapeutics, these devices are reshaping patient experiences and clinical outcomes. The integration of smart technologies like AI, IoT, and cloud computing is redefining operational efficiency, enabling faster diagnostics, improving data accuracy, and reducing human error. Hospitals, clinics, and even home care environments now rely on interconnected medical electronics to streamline workflows, manage chronic diseases, and enhance patient engagement. With an aging global population and the rising incidence of non-communicable diseases, there's a clear shift toward tech-driven healthcare solutions. Consumers are demanding personalized, accessible, and real-time healthcare services, pushing companies to innovate faster and introduce more intuitive, reliable medical electronic devices.

The continuous rise in chronic and infectious diseases-including cardiovascular conditions, cancer, and respiratory disorders-is contributing heavily to the surging demand for advanced medical electronics. There's growing public awareness around early disease detection and preventive care, which is encouraging the widespread use of diagnostic technologies. At the same time, advancements in minimally invasive surgical techniques are accelerating the need for high-precision electronic tools. These innovations are helping improve real-time procedural accuracy, reduce recovery times, and enhance clinical outcomes for patients globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $172.4 Billion |

| Forecast Value | $339.7 Billion |

| CAGR | 7.2% |

The market is also seeing robust momentum from ongoing technological innovation in areas like medical robotics, remote monitoring, and wearable diagnostics. As consumers lean toward smarter, more connected healthcare tools, the integration of electronics in medical applications continues to gain traction. Rising global healthcare expenditures further support the adoption of sophisticated electronic devices, especially those designed to manage complex procedures and long-term care. This trend is particularly evident in specialized medical fields where demand for real-time data, enhanced imaging, and precision control remains critical.

In 2024, the therapeutics segment generated USD 77.1 billion, driven by the increasing use of implantable and external devices to manage chronic conditions. These therapeutic technologies combine advanced electronic features to improve safety, delivery accuracy, and personalized care-especially in cardiovascular, neurological, and respiratory treatment. Devices such as pacemakers, neurostimulators, and infusion pumps are being widely adopted to boost quality of life and reduce hospital visits.

Hospitals led end-user adoption in 2024, generating USD 78.4 billion and accounting for 45.5% of the market share. These institutions depend heavily on both diagnostic and therapeutic electronics to manage outpatient and inpatient care efficiently. With a focus on optimizing clinical workflows and minimizing treatment delays, hospitals continue to invest in next-generation monitoring equipment, surgical technologies, and imaging systems to drive better outcomes.

The U.S. Medical Electronics Market generated USD 57.4 billion in 2023, fueled by the growing burden of chronic diseases such as cardiovascular disorders, diabetes, cancer, and neurological conditions. With more patients requiring continuous monitoring and treatment, the demand for advanced electronic medical devices remains high. The U.S. also benefits from strong R&D infrastructure and early tech adoption, helping sustain its leadership in medical innovation.

Leading players in the Global Medical Electronics Market-including Olympus, Shenzhen Mindray Bio-Medical Electronics, Siemens Healthineers, Lepu Medical Technology, Boston Scientific, Toshiba Medical Systems, FUJIFILM Holdings, GE HealthCare, Abbott Laboratories, MicroPort Scientific, Samsung Electronics, Medtronic, Carestream Health, Koninklijke Philips, and Esaote-are implementing key strategies to strengthen their market presence. These include boosting R&D investments to fast-track innovation, collaborating with healthcare providers for real-time feedback, expanding into emerging markets, and leveraging AI and IoT to launch intelligent diagnostic and remote care platforms.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising burden of chronic and infectious diseases

- 3.2.1.2 Growing adoption of technologically advanced medical electronics

- 3.2.1.3 Increasing preference towards minimally invasive surgeries

- 3.2.1.4 Upsurge in leasing of capital-intensive machines and development of significant policies for foreign direct investment (FDI)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory scenario

- 3.2.2.2 Lack of skilled healthcare professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Therapeutics

- 5.2.1 Pacemakers

- 5.2.2 Implantable cardioverter-defibrillators

- 5.2.3 Neurostimulation devices

- 5.2.4 Surgical robots

- 5.2.5 Respiratory care devices

- 5.3 Diagnostics

- 5.3.1 Patient monitoring devices

- 5.3.2 PET-CT devices

- 5.3.3 MRI scanners

- 5.3.4 Ultrasound devices

- 5.3.5 X-rays devices

- 5.3.6 CT scanners

- 5.4 Other product types

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Ambulatory surgical centers

- 6.4 Clinics

- 6.5 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott Laboratories

- 8.2 Boston Scientific

- 8.3 Carestream Health

- 8.4 Esaote

- 8.5 FUJIFILM Holdings

- 8.6 GE HealthCare

- 8.7 Koninklijke Philips

- 8.8 Lepu Medical Technology

- 8.9 Medtronic

- 8.10 MicroPort Scientific

- 8.11 Olympus

- 8.12 Samsung Electronics

- 8.13 Shenzhen Mindray Bio-Medical Electronics

- 8.14 Siemens Healthineers

- 8.15 Toshiba Medical Systems