丸型コネクタの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Circular Connector Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 136 Pages

- 納期

- 2~3営業日

- 商品コード

- 1741010

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

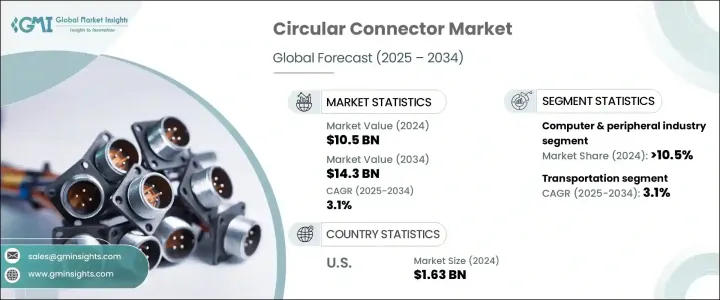

世界の丸型コネクタ市場は2024年に105億米ドルと評価され、CAGR 3.1%で拡大し、2034年には143億米ドルに達すると推定されています。

この成長軌道は、特に過酷で要求の厳しい環境において、データ信号と電力の安定的かつ効率的な伝送を確保する上で、サーキュラーコネクターの重要性が増していることを強調しています。産業オートメーションとデジタルトランスフォーメーションが世界中で加速し続ける中、これらのコネクターは、さまざまなアプリケーションでシームレスかつ安全なオペレーションを可能にする重要なコンポーネントとして台頭してきています。円形コネクターは、高い信頼性、堅牢な設計、環境課題に対する優れた耐性を備えており、これらの特性は、今日の高性能な産業用システムおよび電子システムに不可欠なものとなりつつあります。

スマート・マニュファクチャリングの急増、インダストリー4.0の成長、組み込みシステムの進歩は、すべて需要の高まりに寄与しています。ロボット工学やファクトリーオートメーションから航空宇宙や防衛に至るまで、サーキュラーコネクターは中断のない接続性のためのバックボーンを提供しています。さらに、エッジコンピューティング、IoT、リアルタイム分析の台頭により、システムはより大量のデータを障害なく伝送する必要に迫られており、堅牢なコネクター技術の必要性が高まっています。デジタルインフラの拡大、コンポーネントの小型化、システムの信頼性への注目の高まりといった世界の動向は、現代のイノベーション・エコシステムにおけるサーキュラーコネクターの不可欠な役割をさらに確固たるものにしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 105億米ドル |

| 予測金額 | 143億米ドル |

| CAGR | 3.1% |

自動化技術が各分野で普及するにつれ、複雑な機械のリアルタイム通信とシームレスな操作を可能にする上で、サーキュラーコネクターが重要な役割を果たすようになっています。急速な産業成長と、ファクトリーオートメーションやプロセス制御システムなどのインテリジェントインフラの拡大が、市場の需要を直接後押ししています。通信、自動車システム、軍事機器における絶え間ない技術革新も、高耐久性、高精度、高性能の相互接続ソリューションの必要性を高めています。

現在進行中の5Gインフラの展開と高速データ伝送機能の統合が、採用の主要な推進力として浮上しています。現代の通信ネットワークでは、高周波負荷の下でも完全性と性能を維持できるコネクターが求められており、サーキュラーコネクターはこうした厳しい要件を満たすために独自に設計されています。さらに、防衛産業は、耐候性、耐衝撃性、および極端な運用環境で機能する高信頼性コンポーネントの一貫したニーズによって後押しされ、依然として市場成長に大きく貢献しています。

しかし、市場には課題もあります。世界の貿易政策の変化と関税構造の変動は、サプライチェーンの継続性を阻害し、一時的な品不足を引き起こしています。このようなシフトは長期的な安定を支える一方で、効果的な実施には多額の設備投資と長いスケジュールを必要とします。

2024年の丸型コネクタ市場では、運輸部門が顕著な勢いを示しました。2034年までのCAGRは3.1%と予測されており、この分野の成長は電気自動車(EV)インフラへの投資の急増が主因となっています。高速充電ネットワークの全国展開に対する政府の強力な支援が、高電圧、過酷な天候、頻繁な使用に対応できるコネクタの需要を促進しています。円形コネクターは、その堅牢な構造、効率的な電力伝達能力、急速充電技術との互換性により、EV充電ステーションや車載システムの不可欠な構成要素となっています。

市場を最終用途別にセグメント化すると、電気通信、産業オートメーション、軍事、自動車、コンピュータと周辺機器、運輸、その他ニッチ分野にわたる幅広い用途が浮き彫りになります。2024年には、スマートフォン、ノートパソコン、サーバー、ルーターなどの機器における高速で信頼性の高いデータ転送に対する需要の高まりにより、コンピューターおよび周辺機器分野が10.5%の市場シェアを獲得しました。クラウドコンピューティング、高度なデータセンター、IoT技術の普及が、この分野の需要を引き続き押し上げています。

米国丸型コネクタ2024年の市場規模は16億3,000万米ドルで、持続可能な輸送と電動モビリティ・インフラへの官民の大規模投資が後押ししています。消費者がよりクリーンでハイテクを駆使したモビリティ・ソリューションをますます求めるようになるにつれて、頑丈で高性能な円形コネクタのニーズが高まっており、米国は世界市場拡大の主要な促進要因となっています。

世界の丸型コネクタ分野の主要企業には、矢崎総業、Lapp Group、Fischer Connectors、Mencom、TE Connectivity、Amphenol、Molex、Aptiv、AVX、Phoenix Contact、GTK、ヒロセ電機、3M、日本航空電子工業、Rosenberger、Ametek、Foxconn、Luxshare Precisionなどがあります。これらの企業は、生産能力の拡大、次世代製品開発のための研究開発への投資、多業種にわたる戦略的提携の形成に注力しています。また、革新的な技術にアクセスし、提供する製品の幅を広げるために、多くの企業が買収を進めています。サプライチェーンのリスクを最小化し、より迅速かつ効率的に地域市場の需要に応えることを目的とした、地域製造への強力な軸足もまた牽引力を増しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 貿易への影響

- 展望と今後の検討事項

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略的ダッシュボード

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:最終用途別、2021-2034

- 主要動向

- 通信

- 交通機関

- 自動車

- 産業

- コンピューターと周辺機器

- 軍隊

- その他

第6章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第7章 企業プロファイル

- 3M

- Ametek

- Amphenol

- Aptiv

- AVX

- Fischer Connectors

- Foxconn

- GTK

- Hirose Electric

- Japan Aviation Electronics

- Lapp Group

- Luxshare Precision

- Mencom

- Molex

- Phoenix Contact

- Rosenberger

- TE Connectivity

- Yazaki

目次

The Global Circular Connector Market was valued at USD 10.5 billion in 2024 and is estimated to expand at a CAGR of 3.1% to reach USD 14.3 billion by 2034. This growth trajectory underscores the increasing importance of circular connectors in ensuring stable and efficient transmission of data signals and electrical power, particularly in harsh and demanding environments. As industrial automation and digital transformation continue to accelerate worldwide, these connectors are emerging as crucial components in enabling seamless and secure operations across a variety of applications. Circular connectors offer high reliability, rugged design, and superior resistance to environmental challenges-traits that are becoming indispensable in today's high-performance industrial and electronic systems.

The surge in smart manufacturing, growth of Industry 4.0, and advancements in embedded systems are all contributing to the heightened demand. From robotics and factory automation to aerospace and defense, circular connectors are providing the backbone for uninterrupted connectivity. Furthermore, with the rise of edge computing, IoT, and real-time analytics, systems are under increasing pressure to transmit larger volumes of data without failure, elevating the need for robust connector technologies. Global trends such as digital infrastructure expansion, miniaturization of components, and the rising focus on system reliability further solidify the integral role of circular connectors in modern innovation ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.5 Billion |

| Forecast Value | $14.3 Billion |

| CAGR | 3.1% |

As automation technologies gain ground across sectors, circular connectors are playing a key role in enabling real-time communication and seamless operation of complex machinery. Rapid industrial growth and the expansion of intelligent infrastructure-such as factory automation and process control systems-are directly fueling market demand. Continuous innovation in telecommunications, automotive systems, and military equipment is also driving the need for highly durable, precise, and high-performance interconnect solutions.

The ongoing rollout of 5G infrastructure and the growing integration of high-speed data transmission capabilities have emerged as major drivers of adoption. Modern communication networks demand connectors that can maintain integrity and performance even under high-frequency loads, and circular connectors are uniquely engineered to meet these stringent requirements. In addition, the defense industry remains a significant contributor to market growth, propelled by its consistent need for weather-resistant, shock-proof, and highly reliable components that perform in extreme operational settings.

However, the market does face certain challenges. Shifting global trade policies and fluctuating tariff structures have disrupted supply chain continuity, causing temporary shortages and compelling manufacturers to explore regionalized production strategies. While such a shift supports long-term stability, it also requires substantial capital investments and longer timelines to implement effectively.

In 2024, the transportation sector demonstrated notable momentum within the circular connector market. With projections estimating a steady CAGR of 3.1% through 2034, growth in this sector is driven largely by surging investments in electric vehicle (EV) infrastructure. Strong government support for the nationwide deployment of high-speed charging networks is fueling demand for connectors capable of handling high voltages, harsh weather, and frequent use. Circular connectors are becoming essential components of EV charging stations and onboard systems due to their robust build, efficient power transfer capabilities, and compatibility with fast-charging technology.

Segmenting the market by end-use highlights a broad range of applications spanning telecom, industrial automation, military, automotive, computers and peripherals, transportation, and other niche sectors. In 2024, the computer and peripherals segment captured a 10.5% market share, driven by growing demand for high-speed and dependable data transfer in devices like smartphones, laptops, servers, and routers. The widespread adoption of cloud computing, advanced data centers, and IoT technologies continues to boost demand in this segment.

The United States Circular Connector Market generated USD 1.63 billion in 2024, propelled by significant public and private investments in sustainable transportation and electric mobility infrastructure. As consumers increasingly demand cleaner, tech-enabled mobility solutions, the need for rugged and high-performance circular connectors is rising-positioning the U.S. as a major driver of global market expansion.

Key players in the global circular connector space include Yazaki, Lapp Group, Fischer Connectors, Mencom, TE Connectivity, Amphenol, Molex, Aptiv, AVX, Phoenix Contact, GTK, Hirose Electric, 3M, Japan Aviation Electronics, Rosenberger, Ametek, Foxconn, and Luxshare Precision. These companies are focusing on expanding production capacity, investing in R&D for next-gen product development, and forming strategic alliances across multiple industries. Many are also pursuing acquisitions to access innovative technologies and broaden their offerings. A strong pivot toward regional manufacturing is also gaining traction, aimed at minimizing supply chain risks and catering to local market demands with greater speed and efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data source

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.1 Impact on trade

- 3.3 Outlook and future considerations

- 3.4 Regulatory landscape

- 3.5 Industry impact forces

- 3.5.1 Growth drivers

- 3.5.2 Industry pitfalls & challenges

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By End Use, 2021 - 2034 (Million Units, USD Billion)

- 5.1 Key trends

- 5.2 Telecom

- 5.3 Transportation

- 5.4 Automotive

- 5.5 Industrial

- 5.6 Computer & peripherals

- 5.7 Military

- 5.8 Others

Chapter 6 Market Size and Forecast, By Region, 2021 - 2034 (Million Units, USD Billion)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 UK

- 6.3.3 France

- 6.3.4 Spain

- 6.3.5 Italy

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.4.4 South Korea

- 6.4.5 Australia

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 UAE

- 6.5.3 South Africa

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Argentina

Chapter 7 Company Profiles

- 7.1 3M

- 7.2 Ametek

- 7.3 Amphenol

- 7.4 Aptiv

- 7.5 AVX

- 7.6 Fischer Connectors

- 7.7 Foxconn

- 7.8 GTK

- 7.9 Hirose Electric

- 7.10 Japan Aviation Electronics

- 7.11 Lapp Group

- 7.12 Luxshare Precision

- 7.13 Mencom

- 7.14 Molex

- 7.15 Phoenix Contact

- 7.16 Rosenberger

- 7.17 TE Connectivity

- 7.18 Yazaki

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 136 Pages

- 納期

- 2~3営業日