|

市場調査レポート

商品コード

1740996

成形パルプ包装の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Molded Pulp Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 成形パルプ包装の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月15日

発行: Global Market Insights Inc.

ページ情報: 英文 217 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

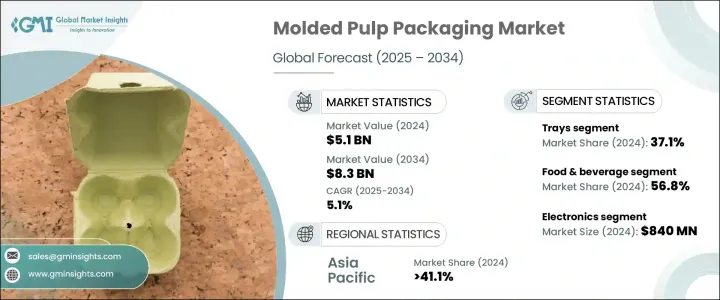

世界の成形パルプ包装市場は、2024年に51億米ドルと評価され、CAGR 5.1%で成長し、2034年には83億米ドルに達すると予測されています。

この成長の原動力となっているのは、環境廃棄物を削減する世界の取り組みとともに、持続可能なパッケージング・ソリューションへのシフトが進んでいることです。使い捨てプラスチックに対する規制が強化され、消費者の環境意識が高まるにつれて、生分解性でリサイクル可能な代替品への需要が高まり続けています。再生可能な繊維ベースの素材から作られた成形パルプ包装は、従来のプラスチック包装に代わる持続可能な代替品を提供し、様々な業界で支持を集めています。堆肥化やリサイクルが可能なこの素材は、環境目標を達成し、エコフレンドリーなイメージの向上を目指すブランドにとって、好ましい選択肢となっています。

成形パルプ包装市場もまた、特にeコマースや小売分野でのプラスチック使用規制の高まりにより、大きな盛り上がりを見せています。こうした規制は、企業を環境に優しいパッケージング・ソリューションへと押し上げています。米国における輸入関税のような貿易政策は、パルプの国内調達を奨励することで地域のサプライチェーンを強化するのに役立っています。この動向は、海外サプライヤーへの依存を減らし、特に輸入コストの上昇が続く場合には、地域のパルプメーカーに利益をもたらす可能性があります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 51億米ドル |

| 予測金額 | 83億米ドル |

| CAGR | 5.1% |

製品タイプの中では、成型パルプトレーが支配的なセグメントとなっており、2024年には19億米ドルを生み出します。この分野は、トレーの保護特性と環境配慮の魅力によって、CAGR 5.2%の成長が見込まれています。産業界がより持続可能な事業へと移行するにつれて、成形パルプトレーの需要は増加し、同分野の成長に拍車がかかると予想されます。

2024年に29億米ドルと評価される飲食品産業も市場拡大の主な要因です。2034年までCAGR 4.9%で成長すると予測されるこの業界では、規制を遵守し、環境意識の高い消費者に対応するため、成形パルプ包装の採用が進んでいます。企業が持続可能性を優先することで、消費者のロイヤリティが向上し、食品関連アプリケーションでの成形パルプ包装の継続的な採用が促進されます。

2024年に市場の41.1%のシェアを占めたアジア太平洋地域は、CAGR 5.6%で成長すると予測されます。急速な工業化、活況を呈するeコマース部門、中国、インド、日本、東南アジアなどの主要市場における持続可能なパッケージングに対する意識の高まりが、プラスチックに代わるパルプ成形品の需要を促進しています。この地域の競争力は、原材料の入手可能性、生産コストの低さ、大規模生産能力によってさらに強化されています。

Huhtamaki、Eco Pulp Packaging、Dart Container Corporation、Henry Molded Products Inc.、Pactiv Evergreen Inc.、UFP Technologies, Inc.などの市場大手企業は、製品ラインの拡大と自動化への投資に注力し、需要の拡大に対応しています。小売業者やFMCGブランドとの戦略的パートナーシップは流通網を強化し、持続可能なイノベーションと生分解性素材への投資は市場での地位固めに役立っています。さらに、これらの企業は新たな地域市場に参入し、長期的なブランド価値を育むために循環経済イニシアチブと連携しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- ベンダーマトリックス

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 業界への影響要因

- 促進要因

- eコマースにおける持続可能な包装の採用増加

- ヘルスケア包装分野での採用増加

- 環境に優しい包装を促進する規制の強化

- 環境への影響に対する消費者の意識の高まり

- 新興市場における持続可能な慣行の出現

- 業界の潜在的リスク&課題

- 長い生産サイクル

- バイオプラスチックとの競合

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

- 将来の市場動向

- 規制情勢

第4章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- トレイ

- クラムシェル

- カップとボウル

- プレート

- その他

第5章 市場推計・予測:成形技術別、2021-2034

- 主要動向

- 厚肉成形

- トランスファー成形

- 熱成形パルプ

- 加工パルプ

第6章 市場推計・予測:最終用途産業別、2021-2034

- 主要動向

- 食品・飲料

- エレクトロニクス

- ヘルスケア

- 自動車

- 化粧品・パーソナルケア

- その他

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 日本

- 中国

- インド

- 韓国

- オーストラリア・ニュージーランド

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ地域

- 中東・アフリカ

- 南アフリカ

- アラブ首長国連邦

- サウジアラビア

- その他中東・アフリカ地域

第8章 企業プロファイル

- Best Plus Pulp Factory

- buhl-paperform GmbH

- CKF Inc.

- Dart Container Corporation

- Eco Pulp Packaging

- EnviroPAK

- Green Pack.

- Hartmann Packaging

- Henry Molded Products Inc.

- Huhtamaki

- HZ Green Pulp Sdn Bhd

- Keiding、Inc.

- Pacific Pulp Molding、Inc

- Pactiv Evergreen Inc.

- Primapack

- Sabert Corporation

- UFP Technologies、Inc.

- Western Pulp Products Company

The Global Molded Pulp Packaging Market was valued at USD 5.1 billion in 2024 and is projected to grow at a CAGR of 5.1% to reach USD 8.3 billion by 2034. This growth is being driven by the increasing shift toward sustainable packaging solutions alongside a global effort to reduce environmental waste. As stricter regulations on single-use plastics take hold and consumers become more environmentally conscious, the demand for biodegradable and recyclable alternatives continues to rise. Molded pulp packaging, made from renewable fiber-based materials, is gaining traction across various industries, offering a sustainable alternative to traditional plastic packaging. This material's compostability and recyclability make it the preferred choice for brands aiming to meet their environmental goals and bolster their eco-friendly image.

The molded pulp packaging market is also experiencing substantial momentum due to growing restrictions on plastic use, particularly in the e-commerce and retail sectors. These restrictions are pushing companies toward eco-friendly packaging solutions. National and international policies favoring green alternatives are further accelerating the market's adoption, with trade policies, like import tariffs in the U.S., helping to strengthen local supply chains by encouraging domestic sourcing of pulp. This trend could reduce reliance on foreign suppliers, benefiting regional pulp producers, especially if import costs continue to rise.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.1 Billion |

| Forecast Value | $8.3 Billion |

| CAGR | 5.1% |

Among product types, molded pulp trays have become a dominant segment, generating USD 1.9 billion in 2024. This segment is expected to grow at a CAGR of 5.2%, driven by the trays' protective properties and eco-conscious appeal. As industries move toward more sustainable operations, demand for molded pulp trays is expected to increase, fueling segment growth.

The food and beverage industry, valued at USD 2.9 billion in 2024, is also a major driver of market expansion. Projected to grow at a CAGR of 4.9% through 2034, the sector is increasingly adopting molded pulp packaging to comply with regulatory mandates and cater to environmentally aware consumers. As companies prioritize sustainability, they enhance consumer loyalty and encourage the continued adoption of molded pulp packaging in food-related applications.

The Asia Pacific region, which held a 41.1% share of the market in 2024, is forecasted to grow at a CAGR of 5.6%. Rapid industrialization, a booming e-commerce sector, and heightened awareness of sustainable packaging in key markets such as China, India, Japan, and Southeast Asia are driving demand for molded pulp alternatives to plastic. The region's competitive edge is further strengthened by the availability of raw materials, lower production costs, and large-scale manufacturing capabilities.

Leading market players such as Huhtamaki, Eco Pulp Packaging, Dart Container Corporation, Henry Molded Products Inc., Pactiv Evergreen Inc., and UFP Technologies, Inc. are focusing on expanding their product lines and investing in automation to meet growing demand. Strategic partnerships with retailers and FMCG brands are enhancing their distribution networks, while investments in sustainable innovations and biodegradable materials are helping them solidify their market position. Additionally, these companies are entering new regional markets and aligning with circular economy initiatives to foster long-term brand value.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Vendor matrix

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news and initiatives

- 3.8 Industry impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Growing adoption of sustainable packaging in e-commerce

- 3.8.1.2 Increased adoption by healthcare packaging sectors

- 3.8.1.3 Rising regulations promoting eco-friendly packaging

- 3.8.1.4 Rising consumer awareness of environmental impacts

- 3.8.1.5 Emergence of sustainable practices in emerging markets

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Lengthy production cycles

- 3.8.2.2 Competition from bioplastics

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Future market trends

- 3.13 Regulatory landscape

Chapter 4 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Bn & Kilo Tons)

- 4.1 Key trends

- 4.2 Trays

- 4.3 Clamshells

- 4.4 Cups and bowls

- 4.5 Plates

- 4.6 Others

Chapter 5 Market Estimates and Forecast, By Molding Technology, 2021 - 2034 (USD Bn & Kilo Tons)

- 5.1 Key trends

- 5.2 Thick-Wall molding

- 5.3 Transfer molding

- 5.4 Thermoformed pulp

- 5.5 Processed pulp

Chapter 6 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Bn & Kilo Tons)

- 6.1 Key trends

- 6.2 Food & beverage

- 6.3 Electronics

- 6.4 Healthcare

- 6.5 Automotive

- 6.6 Cosmetics & personal care

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Bn & Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 Japan

- 7.4.2 China

- 7.4.3 India

- 7.4.4 South Korea

- 7.4.5 ANZ

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 UAE

- 7.6.3 Saudi Arabia

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Best Plus Pulp Factory

- 8.2 buhl-paperform GmbH

- 8.3 CKF Inc.

- 8.4 Dart Container Corporation

- 8.5 Eco Pulp Packaging

- 8.6 EnviroPAK

- 8.7 Green Pack.

- 8.8 Hartmann Packaging

- 8.9 Henry Molded Products Inc.

- 8.10 Huhtamaki

- 8.11 HZ Green Pulp Sdn Bhd

- 8.12 Keiding, Inc.

- 8.13 Pacific Pulp Molding, Inc

- 8.14 Pactiv Evergreen Inc.

- 8.15 Primapack

- 8.16 Sabert Corporation

- 8.17 UFP Technologies, Inc.

- 8.18 Western Pulp Products Company