極低温空気分離ユニットの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Cryogenic Air Separation Unit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 131 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740974

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

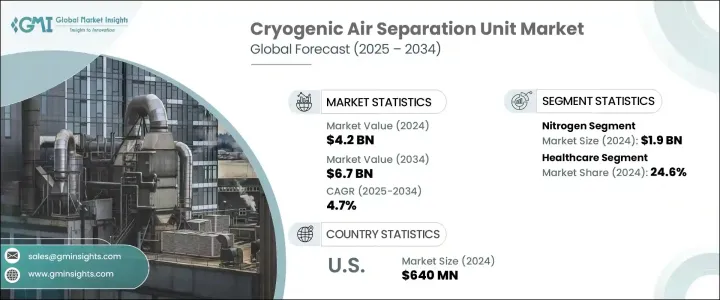

極低温空気分離ユニットの世界市場は、2024年には42億米ドルと評価され、鉄鋼、化学、製造など様々な分野における酸素、窒素、アルゴンなどの工業用ガス需要の増加により、CAGR 4.7%で成長し、2034年には67億米ドルに達すると予測されています。

特に開発途上国で産業活動が拡大するにつれて、これらのガスのニーズが急増し、空気分離技術への投資を促しています。

さらに、COVID-19パンデミックは世界のヘルスケア・システムの脆弱性を浮き彫りにし、特に危機的なピーク時の医療用酸素の不足を浮き彫りにしました。この緊急性が、各国政府と民間ヘルスケア・プロバイダーを動かし、医療用ガス・インフラへの投資を優先させました。その結果、高純度酸素を大規模に生産できる極低温空気分離装置の需要が急増しました。病院や救急医療施設は酸素生成能力のアップグレードを開始し、新規設置や改修につながりました。当面の危機対応にとどまらず、この動向は、特に医療へのアクセスが急速に拡大している新興市場において、ヘルスケアの強靭性を強化するための広範な取り組みの一環として続いています。このシフトはまた、医療用ガスの現地生産を促し、輸入への依存を減らして地域全体の長期的な供給の安定性を確保しました。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 42億米ドル |

| 予測金額 | 67億米ドル |

| CAGR | 4.7% |

アルゴン分野は、精密さを要求される産業用途に欠かせない不活性雰囲気の確立に不可欠な役割を果たすことから、2034年までに14億米ドルに達すると予測されています。製造技術がより専門的になるにつれ、安定した非反応性環境の必要性が高まっています。アルゴンは、TIG溶接、電子機器製造、レーザー切断、特殊ガラスやソーラーパネルの製造などの工程で広く採用されており、その重要性が高まっていることを裏付けています。クリーンエネルギーへの移行、特にソーラー技術の拡大は、アルゴン需要の主要な触媒であり続けています。

ヘルスケア産業は2024年に24.6%のシェアを占め、極低温空気分離ユニットの主要な最終用途セグメントであり続けています。病院、診療所、長期介護センターでは、現場で医療グレードの酸素を生成するために、こうしたシステムへの依存度が高まっています。人口の高齢化と慢性呼吸器疾患が世界のヘルスケア・システムに大きな負担をかける中、このニーズはますます切迫しています。これを受けて、医療ガス・インフラへの投資は、特にヘルスケアへのアクセスと緊急時の即応態勢の強化を目指す地域で拡大しています。

米国極低温空気分離ユニット 2024年の市場規模は6億4,000万米ドルに達します。北米では、シェールガスの探査拡大と、よりクリーンな水素燃料ソリューションの推進に支えられた産業成長が、局所的で大容量のASU設置の需要を生み出しています。こうした施設の多くは、遠隔地や高需要地帯にあり、現地でのガス生成が輸送よりも効率的です。さらに、農業や医薬品製造における窒素需要の高まりは、地域全体の重要なサプライチェーンを支えるASUの役割を強化しています。

世界極低温空気分離ユニット市場の主要企業には、エア・リキード、エアープロダクツ・アンド・ケミカルズ、エア・ウォーター、AMCSコーポレーション、CRYOTEC Anlagenbau GmbH、エナフレックス、海豊空気分離集団、リンデ、メッサー、プラクセア・テクノロジー、ランチ・クライオジェニクス、四川空気分離プラント・グループ、大陽日酸、テクネックス、ユニバーサル・インダストリアル・ガス、インデ・ガスなどがあります。これらの企業は、市場での存在感と技術力を高めるため、合併、買収、提携などの戦略的イニシアティブに注力しています。市場でのプレゼンスを強化するため、企業はいくつかの重要な戦略を採用しています。まず、製品の効率と環境持続可能性を高めるための研究開発に投資しています。これには、再生可能エネルギー源を空気分離装置に組み込んでカーボンフットプリントを削減することも含まれます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 貿易への影響

- 展望と今後の検討事項

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的ダッシュボード

- 戦略的取り組み

- 企業の市場シェア

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:ガスで、2021-2034

- 主要動向

- 窒素

- 酸素

- アルゴン

- その他

第6章 市場規模・予測:最終用途別、2021-2034

- 主要動向

- 鉄鋼

- 石油・ガス

- ヘルスケア

- 化学薬品

- その他

第7章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- Evoqua Water Technologies LLC

- Air Liquide

- Air Products and Chemicals、Inc.

- AIR WATER INC

- AMCS Corporation

- CRYOTEC Anlagenbau GmbH

- Enerflex Ltd.

- KaiFeng Air Separation Group Co.、LTD.

- Linde plc

- Messer

- Praxair Technology、Inc.

- Ranch Cryogenics、Inc.

- Sichuan Air Separation Plant Group

- TAIYO NIPPON SANSO CORPORATION

- Technex

- Universal Industrial Gases、Inc.

- Yingde Gases

目次

The Global Cryogenic Air Separation Unit Market was valued at USD 4.2 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 6.7 billion by 2034, driven by the increasing demand for industrial gases such as oxygen, nitrogen, and argon across various sectors including steel, chemicals, and manufacturing. As industrial activities expand, particularly in developing nations, the need for these gases has surged, prompting investments in air separation technologies.

Additionally, the COVID-19 pandemic highlighted vulnerabilities in global healthcare systems, particularly the shortage of medical-grade oxygen during peak crisis periods. This urgency pushed governments and private healthcare providers to prioritize investments in medical gas infrastructure. As a result, demand surged for cryogenic air separation units capable of producing high-purity oxygen at scale. Hospitals and emergency care facilities began upgrading their oxygen generation capabilities, leading to new installations and retrofits. Beyond the immediate crisis response, this trend has continued as part of broader efforts to strengthen healthcare resilience, especially in emerging markets where healthcare access is expanding rapidly. The shift also encouraged local production of medical gases, reducing reliance on imports and ensuring long-term supply stability across regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Billion |

| Forecast Value | $6.7 Billion |

| CAGR | 4.7% |

The argon segment is projected to hit USD 1.4 billion by 2034, driven by its essential role in establishing inert atmospheres crucial for precision-driven industrial applications. As manufacturing technologies become more specialized, the need for stable, non-reactive environments has intensified. Argon's widespread adoption in processes such as TIG welding, electronics fabrication, laser cutting, and the production of specialty glass and solar panels underscores its growing relevance. The clean energy transition, particularly the expansion of solar technology, continues to be a major catalyst for argon demand, as the gas is indispensable in protecting materials from contamination during high-temperature procedures.

The healthcare industry, accounting for a 24.6% share in 2024, remains a major end-use segment for cryogenic air separation units. Hospitals, clinics, and long-term care centers increasingly depend on these systems to generate medical-grade oxygen onsite. This need is becoming more pressing as aging populations and chronic respiratory conditions place greater strain on healthcare systems worldwide. In response, investments in medical gas infrastructure have grown, particularly in regions seeking to enhance healthcare access and emergency readiness.

U.S. Cryogenic Air Separation Unit Market reached USD 640 million in 2024. Industrial growth in North America, supported by increased exploration of shale gas and a push for cleaner hydrogen fuel solutions, has created demand for localized, high-capacity ASU installations. Many of these facilities are in remote or high-demand zones where on-site gas generation is more efficient than transportation. Additionally, rising nitrogen demand in agriculture and pharmaceutical manufacturing reinforces the role of ASUs in supporting critical supply chains across the region.

Key players in the Global Cryogenic Air Separation Unit Market include Air Liquide, Air Products and Chemicals, Inc., AIR WATER INC, AMCS Corporation, CRYOTEC Anlagenbau GmbH, Enerflex Ltd., KaiFeng Air Separation Group Co., LTD, Linde plc, Messer, Praxair Technology, Inc., Ranch Cryogenics, Inc., Sichuan Air Separation Plant Group, TAIYO NIPPON SANSO CORPORATION, Technex, Universal Industrial Gases, Inc., and Yingde Gases. These companies focus on strategic initiatives such as mergers, acquisitions, and partnerships to enhance their market presence and technological capabilities. To strengthen their presence in the market, companies are adopting several key strategies. Firstly, they are investing in research and development to enhance the efficiency and environmental sustainability of their products. This includes integrating renewable energy sources into air separation units to reduce carbon footprints.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data source

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.1 Impact on trade

- 3.3 Outlook and future considerations

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Strategic initiative

- 4.4 Company market share

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Gas, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Nitrogen

- 5.3 Oxygen

- 5.4 Argon

- 5.5 Others

Chapter 6 Market Size and Forecast, By End Use, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Iron & steel

- 6.3 Oil & gas

- 6.4 Healthcare

- 6.5 Chemicals

- 6.6 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Evoqua Water Technologies LLC

- 8.2 Air Liquide

- 8.3 Air Products and Chemicals, Inc.

- 8.4 AIR WATER INC

- 8.5 AMCS Corporation

- 8.6 CRYOTEC Anlagenbau GmbH

- 8.7 Enerflex Ltd.

- 8.8 KaiFeng Air Separation Group Co., LTD.

- 8.9 Linde plc

- 8.10 Messer

- 8.11 Praxair Technology, Inc.

- 8.12 Ranch Cryogenics, Inc.

- 8.13 Sichuan Air Separation Plant Group

- 8.14 TAIYO NIPPON SANSO CORPORATION

- 8.15 Technex

- 8.16 Universal Industrial Gases, Inc.

- 8.17 Yingde Gases

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 131 Pages

- 納期

- 2~3営業日