|

市場調査レポート

商品コード

1833632

ヘルスケアコンサルティングサービスの市場機会と促進要因、業界動向分析、2025年~2034年予測Healthcare Consulting Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ヘルスケアコンサルティングサービスの市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年09月02日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

概要

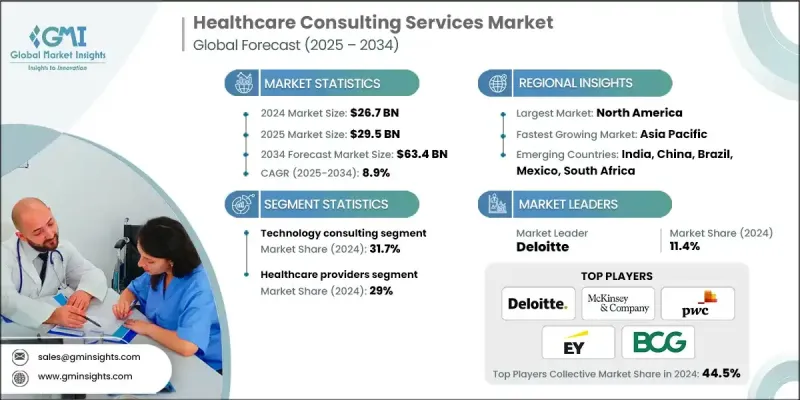

Global Market Insights Inc.が発行した最新レポートによると、世界のヘルスケアコンサルティングサービス市場は2024年に267億米ドルと推定され、CAGR 8.9%で2025年の295億米ドルから2034年には634億米ドルに成長すると予測されています。

電子カルテ(EHR)の導入、遠隔医療プラットフォーム、AIを活用した診断など、デジタル化の推進により、専門家の指導に対する強いニーズが生まれています。ヘルスケアコンサルタントは、臨床とビジネスの目的に沿ったデジタルツールの選択、導入、最適化においてプロバイダーと支払者をサポートします。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 267億米ドル |

| 予測金額 | 634億米ドル |

| CAGR | 8.9% |

テクノロジー・コンサルティングが牽引役に

プロバイダーや支払者が業務の近代化のためにデジタルイニシアチブを加速させていることから、テクノロジーコンサルティング分野が2024年に注目すべきシェアを占める。電子カルテ(EHR)や遠隔医療プラットフォームの導入から、AI主導のアナリティクスやサイバーセキュリティ・ソリューションの展開に至るまで、テクノロジー・コンサルタントは、医療機関がよりデータ中心で接続されたエコシステムに適応するための不可欠なパートナーです。デジタルヘルスの導入が進むにつれ、戦略的で拡張性があり、コンプライアンスに準拠したテクノロジー・ロードマップに対する需要は、コンサルティング会社の主要な促進要因であり続けています。

ヘルスケアプロバイダーの採用増加

ヘルスケアプロバイダー分野は、業務の最適化、患者の転帰の改善、管理間接費の削減の必要性により、2024年に大きな収益を上げました。コンサルタントは医療提供機関と密接に連携し、ケア提供モデルの再設計、バリュー・ベース・ケアの枠組みへの適合、臨床および財務実績の管理を行う。ワークフォースプランニング、デジタル統合、サプライチェーンの最適化など、プロバイダーは急速に変化するヘルスケアの状況に適応するため、専門家のアドバイザーを頼るようになっています。

北米が推進力のある地域として台頭

北米ヘルスケアコンサルティングサービス市場は、先進的なヘルスケアインフラ、高い技術導入レベル、法規制遵守への強い関心が原動力となり、2024年に持続的なシェアを維持した。米国は、大規模な病院ネットワークや保険プロバイダーにおける価値ベースの償還モデル、ポピュレーションヘルス・イニシアチブ、デジタルトランスフォーメーションへの継続的なシフトが需要を牽引しています。コンサルティング会社は、都市部と地方市場の両方でクライアントの多様なニーズに対応するため、専門性の高い人材、現地での提供能力、機能横断的なサービス提供に投資することで存在感を高めています。

ヘルスケアコンサルティングサービス市場の主要プレーヤーは、IQVIA、Guidehouse、L.E.K. Consulting、Vizient、Capgemini、Ernst &Young、Boston Consulting Group、Cognizant、Bain &Company、Deloitte、Oliver Wyman、Accenture、Chartis、PwC、ClearView Healthcare Partners、Kearney、NTT DATA、HURON、McKinsey &Company、KPMGです。

ヘルスケアコンサルティングサービス市場のリーディング・ファームは、そのポジションを強化するために、専門性、拡張性、クライアント中心のイノベーションに焦点を当てた戦略を採用しています。その多くは、支払者戦略、ポピュレーション・ヘルス、規制遵守などの分野で深い専門知識を持つ垂直専門チームを構築しています。企業はまた、買収やヘルステック新興企業との提携を通じてデジタル能力を拡大し、エンドツーエンドのトランスフォーメーション・サービスを提供できるようにしています。さらに、データ・セキュリティと相互運用性が重視され、各社はHIPAAやその他のプライバシー義務に沿ったフレームワークを開発しています。戦略的アドバイザリーと実践的な導入、そして長期的なチェンジ・マネジメントを組み合わせることで、コンサルティング・プロバイダーはヘルスケアの変革に欠かせないパートナーとしての地位を確立しつつあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- ヘルスケア分野における技術の進歩

- 合併・買収活動の増加

- 世界の研究開発費の増加

- 業界の潜在的リスク&課題

- 隠れたコストと運用のダイナミクス

- 市場機会

- デジタルヘルス変革への需要の高まり

- AIとデータ分析の統合の需要

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- テクノロジーの情勢

- 現在の技術動向

- 新興技術

- ギャップ分析

- ポーター分析

- PESTEL分析

- 将来の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- グローバル

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新しいサービスタイプの開始

- 拡張計画

第5章 市場推計・予測:サービス種別、2021-2034

- 主要動向

- テクノロジーコンサルティング

- 戦略コンサルティング

- オペレーションコンサルティング

- 財務コンサルティング

- その他のサービスタイプ

第6章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- ヘルスケア提供者

- ヘルスケア支払者

- ライフサイエンスおよび製薬会社

- ヘルスケアテクノロジーおよびデジタルヘルス企業

- 政府および規制機関

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- Accenture

- Bain &Company

- Boston Consulting Group

- Capgemini

- Chartis

- ClearView Healthcare Partners

- Cognizant

- Deloitte

- Ernst &Young

- Guidehouse

- HURON

- IQVIA

- Kearney

- KPMG

- L.E.K Consulting

- McKinsey &Company

- NTT DATA

- Oliver Wyman

- PricewaterhouseCoopers(PwC)

- Vizient