|

市場調査レポート

商品コード

1521855

ヘルスケアコンサルティングサービス:市場シェア分析、業界動向、成長予測(2024~2029年)Healthcare Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ヘルスケアコンサルティングサービス:市場シェア分析、業界動向、成長予測(2024~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 114 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

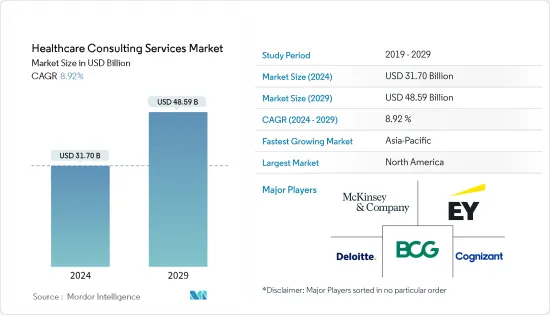

ヘルスケアコンサルティングサービスの市場規模は2024年に317億米ドルと推定され、2029年には485億9,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは8.92%で成長すると予測されます。

市場成長を促進する主な要因としては、ヘルスケア製品に対する需要の高まり、医療の質の向上と医療費削減のニーズの高まりなどが挙げられます。

ヘルスケアはここ数年、増加する患者人口への対応という点で、大きな変化を目の当たりにしてきました。ヘルスケアコンサルティングサービス市場は、世界のデジタル化の急速な導入が主な要因となっています。アジャイルな手法による強固なITサポートは、ヘルスケアプロバイダーにとって、収益性の向上、在庫管理の簡素化、品質の向上、コストの抑制を実現する上で競合優位性を発揮します。

ヘルスケアコンサルティングサービスを医療と統合することで、生活習慣の改善や予防医療が有効な個人の特定、患者特性の分析、予測事象を特定し予防イニシアチブをサポートするための広範な疾患プロファイリングの分類、費用対効果の高い治療法を特定するための治療コストとアウトカムの分析などのメリットがもたらされることが期待されます。例えば、国際糖尿病連合(International Diabetes Federation 2022)の推計によると、2045年までに糖尿病治療にかかる世界の支出は、技術の進歩により1兆540億米ドルにまで拡大する見込みであり、その主な原因はワイヤレス機器やウェアラブル機器、アプリケーションの高い普及率にあります。そのため、慢性疾患に対するこのような巨額の支出は、患者の医療負担を軽減するための戦略を策定するヘルスケアコンサルティングサービスの採用を増加させると予想されます。

さらに、ヘルスケアプロバイダーとヘルスケアコンサルティングサービスプロバイダーの間のパートナーシップの高まりも、予測期間中に調査された市場での需要を増加させ、市場の成長を促進すると予想されます。例えば、2023年6月、データアナリストのヴイット、アドバイザリー会社のデベロップ・コンサルティング、ヘルスケア改善のスペシャリストであるイノベーティブ・オンライン・プロダクツ、トレーニングプロバイダーのクリック2・ラーンの4社によるシンジケートが、英国の国民保健サービス(NHS)のための統合改善パートナーシップを立ち上げました。これは、NHSが英国医療システム内の効率性を実現し、NHS全体の効率性削減と能力向上のための戦略を策定することを支援するものです。

さらに、先進国や発展途上国における政府の好意的な政策により、ITヘルスケアコンサルティングの機会が増加しています。その他の要因としては、ヘルスケアITソリューションに対する政府支援の増加や、予測期間中の技術状況の変化が挙げられます。しかし、導入コストの高さが市場の成長を抑制すると予想されます。

ヘルスケアコンサルティングサービス市場の動向

予測期間中、病院セグメントがヘルスケアコンサルティングサービス市場で大きなシェアを占める見込み

- 病院では、ITセキュリティサービス、サポートサービス、リソースプランニング、ITインフラ管理、モバイルコンピューティング、クラウドベースのソリューションなど、業務のデジタル化が進んでいます。スケーラブルな運用により、ヘルスケアプロバイダーはヘルスケアコンサルティングサービス市場で収益の増加を目の当たりにしています。

- 病院におけるITコンサルティングは、デジタルヘルスケアインフラの中で、より重要かつ継続的な情報の流れを実現するのに役立ちます。アウトソーシングされたITコンサルティングサービスには、分析ダッシュボード、臨床プラットフォームの開発・保守、ネットワーク最適化サービス、IT調達、クラウドサービスなどが含まれます。

- 病院とヘルスケアコンサルティング企業間のパートナーシップの高まりにより、病院の収益成長を維持するためのITコンサルティングサービスの需要が増加し、それによってセグメントの成長が促進されると予想されます。例えば、2023年10月、バーチャルヘルスケアソリューションプロバイダーであるCura社は、サウジアラビア・ドイツ病院グループと提携し、患者のヘルスケアサービスへのアクセスに革命を起こしました。この提携により、患者はオンライン診察、遠隔モニタリング、サウジ・ドイツ・ホスピタル・グループの全拠点で統合された健康情報交換など、さまざまなヘルスケアサービスを利用できるようになった。

- さらに、病院は収益サイクル管理、企業資源計画(ERP)支援サービス、人口健康管理などの支援も受けており、これらも市場の成長に寄与すると予想されます。加えて、フィー・フォー・サービス(FFS)からバリュー・ベース・ケアへの移行は、ヘルスケアプロバイダーへの圧力を高めています。このため、予測期間中は病院が大きな市場シェアを占めると予想されます。

北米が市場で大きなシェアを占めており、予測期間中もその傾向が続くと予想される

- 北米における市場の成長は、医療費支払いや規制の変更に起因しています。その結果、ヘルスケアプロバイダーはヘルスケアITコンサルティング会社への依存度を高めています。

- さらに、米国の規制改革に伴い、コスト削減と顧客満足度を求める支払者間の競争が激化しています。ヘルスケアの支払者と提供者は、コンサルティング会社によるITサポートを必要とする斬新な運営モデルを適用しているため、技術的な変革が進んでいます。

- 米国保健社会福祉省が2024年に公表した年次実績計画・報告書のデータによると、2023年度に州・管轄区の母子・幼児家庭訪問(MIECHV)プログラムが提供した参加者数は164,470人であったのに対し、2024年度は188,067人でした。このように、妊産婦・乳幼児・幼児訪問の増加は、妊産婦・胎児・乳幼児ケアの需要を促進し、ヘルスケアコンサルティングサービス市場の成長を後押ししています。

- さらに米国では、65歳以上の高齢者や州政府と連携した一部の障害者を対象としたメディケア・メディケイド・サービスセンターのようなヘルスケアサービスを提供する政府助成プログラムが市場を押し上げる可能性が高いです。

- 在宅医療領域におけるヘルスケアコンサルティング企業間のパートナーシップの高まりは、市場の成長を促進すると予想されます。例えば、2024年3月、Brinster &Bergmanは、在宅ヘルスケアコンサルティング会社であるGary Carpenter and Associatesとパートナーシップを結び、州の規制や税法を探る戦略で在宅ヘルスケア機関を支援しています。

- さらに、大小のヘルスケアプロバイダーは、ヘルスケアシステムの複雑な変化すべてに対応できないため、ヘルスケアコンサルティングサービスを第三者プロバイダーにアウトソーシングしています。データ・セキュリティーやアナリティクスなどの革新的なアプローチにより、ヘルスケアプロバイダーは患者の体験を向上させることで利益を得ており、その結果、収益も増加しています。これが北米のヘルスケアコンサルティングサービス市場の成長に寄与していると思われます。

ヘルスケアコンサルティングサービス業界の概要

ヘルスケアコンサルティングサービス市場は非常に細分化されており、中小規模のエンドユーザーによるヘルスケアコンサルティングサービスの採用が拡大しているため、健全な成長を遂げています。さらに、アジア太平洋地域ではヘルスケアコンサルティングサービスの市場浸透が進むと予想され、新規参入企業に成長機会を提供しています。市場に参入している企業には、アクセンチュア、デロイトトウシュトーマツ、ボストンコンサルティンググループ、コグニザント、マッキンゼー・アンド・カンパニーなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- ヘルスケア製品に対する需要の高まり

- 医療の質の向上とヘルスケアコスト削減のニーズの高まり

- 市場抑制要因

- 類似技術の存在

- 導入コストの高さ

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(金額ベース市場規模)

- サービスタイプ別

- デジタルコンサルティング

- ITコンサルティング

- コンポーネント別

- サービス

- ソリューション別

- エンドユーザー別

- 病院

- クリニック

- ライフサイエンス企業

- 用途別

- 財務

- 運用管理

- ポピュレーションヘルス

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Deloitte Touche Tohmatsu Limited

- McKinsey & Company

- Accenture Consulting

- Huron Consulting

- PWC

- Ernst & Young

- The Boston Consulting Group

- Bain & Company

- KPMG

- Cognizant

- IQVIA

- ZS

第7章 市場機会と今後の動向

The Healthcare Consulting Services Market size is estimated at USD 31.70 billion in 2024, and is expected to reach USD 48.59 billion by 2029, growing at a CAGR of 8.92% during the forecast period (2024-2029).

The major factors driving the market growth include the rising demand for healthcare products and the rising need to improve the quality of care and reduce healthcare costs.

Healthcare has witnessed substantial changes in the past few years in terms of serving the growing patient population. The healthcare consulting services market is mainly driven by the rapid adoption of global digitalization. Robust IT support with agile methods is a competitive advantage for healthcare providers in achieving increased profitability, simplifying inventory management, improving quality, and controlling costs.

The integration of healthcare consulting services with medicine is expected to deliver benefits, like identifying individuals who may benefit from lifestyle changes or preventative care, analyzing patient characteristics, classifying broad-scale disease profiling to identify predictive events and support prevention initiatives, and analyzing the cost and outcomes of care to identify cost-effective treatments. For example, the International Diabetes Federation 2022 estimated that by 2045, the global expenditures for diabetes treatment are expected to grow to USD 1,054 billion due to technological advancements, which can primarily be attributed to the high adoption of wireless and wearable devices and applications. Therefore, such a huge expenditure on chronic diseases is anticipated to increase the adoption of healthcare consulting services to develop strategies for the reduction of the healthcare burden on patients.

Furthermore, the rising partnerships among the healthcare providers and the healthcare consulting service providers are also anticipated to increase the demand in the market studied during the forecast period, driving the market's growth. For instance, in June 2023, a syndicate of four businesses: data analyst Vuit, advisory firm Develop Consulting, healthcare improvement specialist Innovative Online Products, and training provider Click2 Learn launched an Integrated Improvement Partnership for National Health Service (NHS) in the United Kingdom. This will help the NHS realize efficiencies within the UK healthcare system and develop strategies for efficiency savings and capacity building across the NHS.

Furthermore, there has been a rise in IT healthcare consulting opportunities due to favorable government policies in developed and developing regions. Other factors include increasing government support for healthcare IT solutions and the changing technology landscape during the forecast period. However, the high cost of deployment is expected to restrain the growth of the market.

Healthcare Consulting Services Market Trends

Hospitals Segment Expected to Hold a Significant Share in the Healthcare Consulting Services Market During the Forecast Period

- Hospitals are digitalizing their business practices in IT security services, support services, resource planning, IT infrastructure management, mobile computing, and cloud-based solutions. With scalable operations, healthcare providers have witnessed increased revenues in the healthcare consulting services market.

- IT consulting in hospitals can help achieve a more significant and continuous flow of information within a digital healthcare infrastructure. Outsourced IT consulting services include analytics dashboards, development and maintenance of clinical platforms, network optimization services, IT procurement, and cloud services.

- Rising partnerships among hospitals and healthcare consulting firms are anticipated to increase the demand for IT consulting services to sustain hospital revenue growth and thereby boost segment growth. For instance, in October 2023, Cura, a virtual healthcare solutions provider, partnered with the Saudi German Hospital Group to revolutionize patient access to healthcare services. This partnership allows patients to utilize various healthcare services, including online consultations, remote monitoring, and health information exchange integrated across all Saudi German Hospital Group locations.

- Furthermore, the hospitals are also taking support for revenue cycle management, enterprise resource planning (ERP) support service, and population health, which are also anticipated to contribute to the market's growth. In addition, the transition from fee-for-service (FFS) to value-based care is increasing the pressure on healthcare providers. Thus, hospitals are anticipated to hold a significant market share during the forecast period.

North America Holds a Significant Share in the Market and is Expected to Continue the Same During the Forecast Period

- The market's growth in North America is attributed to changes in medicare payments and regulations. As a result, healthcare providers are increasingly dependent on healthcare IT consulting companies.

- Furthermore, with regulatory reforms in the United States, there is increased competition among payers for cost savings and customer satisfaction. Healthcare payers and providers are undergoing technological transformation as they are applying novel operating models that need IT support from consulting firms.

- According to data published by the United States Department of Health and Human Services in 2024 in the form of an Annual Performance Plan and Report, the number of participants served by the state/jurisdiction maternal, infant, and early childhood home visiting (MIECHV) program in FY2023 was 164,470 compared to 188,067 in FY2024. Thus, the increase in maternal, infant, and early childhood visits fuels the demand for maternal, fetal, and infant care, boosting the growth of the healthcare consulting services market.

- In addition, in the United States, government funding programs that provide healthcare services like the Centers for Medicare and Medicaid Services for people aged 65 years and older, as well as some people with disabilities working in partnership with the state governments, are likely to boost the market.

- Rising partnerships among healthcare consulting firms in the home healthcare domain are anticipated to propel the market's growth. For instance, in March 2024, Brinster & Bergman entered a partnership with Gary Carpenter and Associates, a home healthcare consulting firm, to assist home healthcare agencies with strategies for exploring state regulatory and tax laws.

- Moreover, small and big healthcare providers are outsourcing healthcare consulting services to third-party providers, as they cannot handle all the complex changes in the healthcare system. With innovative approaches, such as data security and analytics, healthcare providers benefit by improving the experience of patients and, therefore, gaining increased revenues. This is likely to contribute to the growth of the healthcare consulting services market in North America.

Healthcare Consulting Services Industry Overview

The healthcare consulting services market is highly fragmented and experiencing healthy growth owing to the greater adoption of healthcare consulting services by smaller and mid-sized end users. Moreover, healthcare consulting service market penetration is expected to increase in Asia-Pacific, offering growth opportunities for new entrants. Some of the players operating in the market are Accenture, Deloitte Touche Tohmatsu LLC, The Boston Consulting Group, Cognizant, and McKinsey and Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Healthcare Products

- 4.2.2 Rising Need to Improve the Quality of Care and Reduce Healthcare Costs

- 4.3 Market Restraints

- 4.3.1 Availability of Similar Technology

- 4.3.2 High Cost of Deployment

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Service Type

- 5.1.1 Digital Consulting

- 5.1.2 IT Consulting

- 5.2 By Component

- 5.2.1 Services

- 5.2.2 Solutions

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Clinics

- 5.3.3 Life Science Companies

- 5.4 By Application

- 5.4.1 Financial

- 5.4.2 Operations Management

- 5.4.3 Population Health

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Deloitte Touche Tohmatsu Limited

- 6.1.2 McKinsey & Company

- 6.1.3 Accenture Consulting

- 6.1.4 Huron Consulting

- 6.1.5 PWC

- 6.1.6 Ernst & Young

- 6.1.7 The Boston Consulting Group

- 6.1.8 Bain & Company

- 6.1.9 KPMG

- 6.1.10 Cognizant

- 6.1.11 IQVIA

- 6.1.12 ZS