|

市場調査レポート

商品コード

1740951

PEF(ポリエチレンフラノエート)の市場機会、成長促進要因、産業動向分析、予測、2025年~2034年PEF (Polyethylene Furanoate) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| PEF(ポリエチレンフラノエート)の市場機会、成長促進要因、産業動向分析、予測、2025年~2034年 |

|

出版日: 2025年04月23日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

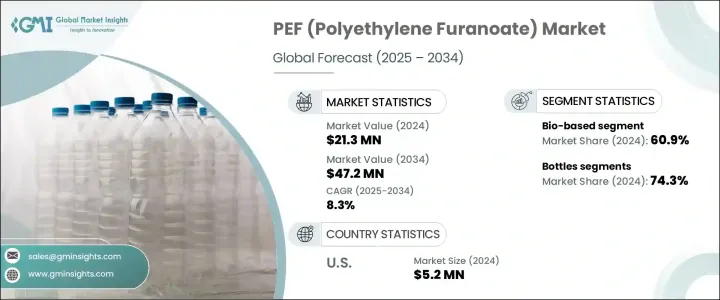

PEF(ポリエチレンフラノエート)の世界市場は、2024年に2,130万米ドルと評価され、CAGR 8.3%で成長し、2034年には4,720万米ドルに達すると推定されます。

PEFは、主に植物由来の糖類を原料とする再生可能な原料から得られる次世代のバイオベースポリエステルです。ポリエチレンテレフタレート(PET)のような従来の石油ベースのプラスチックに代わる環境に優しい代替品として、PEFは、持続可能性への消費者と規制のシフトの増加により、大きな支持を得ています。市場成長の主な要因は、環境に優しい包装ソリューションに対する需要の高まり、プラスチック廃棄物の削減を目的とした規制の強化、PETのような従来のプラスチックよりも優れた利点を提供するPEF固有の材料特性です。

持続可能な包装に対する世界の後押しの高まりは、PEF市場の拡大を促進する重要な要因の一つです。消費者も企業も政府も、包装の環境フットプリントの削減にますます力を注いでおり、再生可能な植物由来のPEFは有望な解決策を提供しています。このポリエステルは従来のプラスチックに比べて二酸化炭素排出量を削減するだけでなく、PEFは生分解性であるため廃棄物の蓄積を減らすことにも貢献します。さらに、PETに比べて酸素、二酸化炭素、水蒸気に対する耐性が高いなど、バリア性に優れているため、製品の品質と賞味期限が重要な食品・飲料包装などの分野で特に重宝されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 2,130万米ドル |

| 予測金額 | 4,720万米ドル |

| CAGR | 8.3% |

PEFの需要が高まり続ける中、市場は世界中の企業からの関心を高めています。特にPEFボトルは、PEF使用量全体の74.3%を占め、市場で最大のシェアを獲得しています。これはPEFの高度なバリア機能によるもので、飲料の鮮度を長期間保つことができます。製品の寿命が重要な飲料業界では、従来のプラスチックからバイオベースの代替品へのシフトは単なる動向ではなく、必要不可欠なものです。さらに、環境の持続可能性をめぐる消費者の意識の高まりが、飲料メーカーにこうしたより環境に優しい素材の採用を促しています。各国政府がプラスチック廃棄物や二酸化炭素排出に関する規制を強化する中、飲料業界の大手企業はPEFのようなバイオベースプラスチックへの転換を進めています。

また、世界のPEF市場は、バイオベースと植物ベースの二種類に大別されます。バイオベースセグメントは、バイオベース原料の多様性により、2024年には60.9%のシェアを占める圧倒的な存在となっています。特定の作物に依存することが多い植物由来の原料とは異なり、バイオベースの製造方法では、メーカーは農業製品別、工業残渣、糖分を多く含むバイオマスなど、幅広い原料を使用することができます。このような柔軟性は、サプライ・チェーンを確保するだけでなく、PEF生産の拡張性と弾力性を強化し、需要の増加に伴う継続的な成長を保証します。

米国はPEF市場における重要なプレーヤーであり、2024年には520万米ドルを生み出します。この成長の主な原動力は、バイオベースの材料の採用を支援する政府の取り組みです。再生可能プラスチックの使用を促進するためのプログラムは、特に連邦政府の調達義務を通じて、PEFにとって有利な状況を作り出しています。これらのイニシアチブは、環境負荷の低減に役立つだけでなく、包装、繊維、フィルムなど多様な用途でPEFの機会を広げています。持続可能なプラスチックの成長を助長する環境を育成することで、米国は環境に優しい素材への世界のシフトにおけるリーダーとしての地位を確立しつつあります。

この急成長市場に資本参加するため、PEF分野の主なプレーヤーは、生産能力の拡大、他の業界リーダーとの戦略的パートナーシップの形成、PEFの生産方法の改善と材料特性の向上のための研究開発への多額の投資など、様々な戦略を採用しています。BASF SE、Avantium、Amcor、Alpla Group、東洋紡などの企業は、この技術革新の最前線に立ち、環境に優しい包装市場の主要プレーヤーとしての地位を確立しています。持続可能なソリューションを採用し、政府のインセンティブを活用することで、これらの企業は急速に進化する包装業界で一歩先を行くことを目指しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 主要メーカー

- 販売代理店

- 業界全体の利益率

- 供給の混乱

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 持続可能なバイオベースの包装材料に対する世界の需要の高まり

- プラスチック廃棄物と炭素排出量の削減に向けた規制圧力の高まり

- PEFはPETに比べてバリア性や機械的強度に優れているなど、優れた性能特性

- 業界の潜在的リスク&課題

- フルクトース由来2,5-フランジカルボン酸(FDCA)などの原料の入手可能性への依存

- PLAやバイオPETなどの他のバイオベースポリマーとの競合

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推定・予測:由来別、2021年~2034年

- 主要動向

- 植物由来

- バイオベース

第6章 市場推定・予測:用途別、2021年~2034年

- 主要動向

- ボトル

- ファイバー

- 膜

- その他

第7章 市場推定・予測:最終用途産業別、2021年~2034年

- 主要動向

- 包装

- テキスタイル

- エレクトロニクス

- 医薬品

- その他

第8章 市場推定・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Alpla Group

- Amcor

- AVA Biochem

- Avantium

- BASF SE

- Origin Materials

- Sulzer

- Swicofil

- Toyobo

The Global PEF (Polyethylene Furanoate) Market was valued at USD 21.3 million in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 47.2 million by 2034. PEF is a next-generation, bio-based polyester derived from renewable feedstocks, primarily derived from plant-based sugars. As an eco-friendly alternative to traditional petroleum-based plastics, such as polyethylene terephthalate (PET), PEF has been gaining significant traction due to the increasing consumer and regulatory shift toward sustainability. The market growth is largely fueled by the rising demand for environmentally friendly packaging solutions, stricter regulations aimed at reducing plastic waste, and the inherent material properties of PEF, which offer superior advantages over conventional plastics like PET.

The growing global push toward sustainable packaging is one of the key factors driving the expansion of the PEF market. Consumers, companies, and governments alike are increasingly focused on reducing the environmental footprint of packaging, and PEF, derived from renewable plant sources, offers a promising solution. This polyester not only reduces the carbon footprint compared to traditional plastics but also contributes to less waste accumulation, as PEF is biodegradable. Moreover, its superior barrier properties, which include better resistance to oxygen, carbon dioxide, and water vapor compared to PET, make it particularly valuable in sectors such as food and beverage packaging, where product quality and shelf life are crucial.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.3 Million |

| Forecast Value | $47.2 Million |

| CAGR | 8.3% |

As demand for PEF continues to rise, the market is seeing increased interest from companies across the globe. PEF bottles, in particular, have captured the largest share of the market, accounting for 74.3% of the overall PEF usage. This is due to PEF's advanced barrier capabilities, which preserve the freshness of beverages for longer periods. In the beverage industry, where product longevity is vital, the shift from traditional plastics to bio-based alternatives is not just a trend but a necessity. Furthermore, the growing consumer awareness surrounding environmental sustainability is pushing beverage manufacturers to adopt these more eco-friendly materials. With governments enforcing stricter regulations on plastic waste and carbon emissions, major corporations in the beverage industry are making the switch to bio-based plastics like PEF.

The global PEF market is also divided into two primary categories: bio-based and plant-based sources. The bio-based segment is dominant, holding a 60.9% share in 2024, thanks to the versatility of bio-based feedstocks. Unlike plant-based sources, which often rely on specific crops, bio-based production methods allow manufacturers to use a wide range of raw materials, such as agricultural byproducts, industrial residues, and sugar-rich biomass. This flexibility not only secures supply chains but also strengthens the scalability and resilience of PEF production, ensuring its continued growth as demand increases.

The United States is a significant player in the PEF market, generating USD 5.2 million in 2024. A major driver of this growth has been government initiatives that support the adoption of bio-based materials. Programs designed to promote the use of renewable plastics, particularly through federal procurement mandates, have created a favorable landscape for PEF. These initiatives not only help reduce the environmental impact but also open up opportunities for PEF across diverse applications, including packaging, textiles, and films. By fostering an environment conducive to the growth of sustainable plastics, the U.S. is establishing itself as a leader in the global shift toward eco-friendly materials.

To capitalize on this rapidly growing market, key players in the PEF sector are employing a range of strategies, including expanding their production capacities, forming strategic partnerships with other industry leaders, and investing heavily in research and development to improve PEF production methods and enhance its material properties. Companies such as BASF SE, Avantium, Amcor, Alpla Group, and Toyobo are at the forefront of this innovation, positioning themselves as key players in the eco-friendly packaging market. By embracing sustainable solutions and leveraging government incentives, these companies aim to stay ahead of the curve in the fast-evolving packaging industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Key manufacturers

- 3.1.2 Distributors

- 3.1.3 Profit margins across the industry

- 3.1.4 Supply disruptions

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic Industry Responses

- 3.2.4.1 Supply Chain Reconfiguration

- 3.2.4.2 Pricing and Product Strategies

- 3.2.4.3 Policy Engagement

- 3.2.5 Outlook and Future Considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major Exporting Countries

- 3.3.2 Major Importing Countries

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising global demand for sustainable and bio-based packaging materials

- 3.7.1.2 Increasing regulatory pressure to reduce plastic waste and carbon emissions

- 3.7.1.3 High performance properties of PEF compared to PET, such as better barrier resistance and mechanical strength

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Dependency on feedstock availability such as fructose-derived 2,5-Furandicarboxylic acid (FDCA)

- 3.7.2.2 Competition from other bio-based polymers such as PLA and bio-PET

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Source, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Plant based

- 5.3 Bio-based

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Bottles

- 6.3 Fibres

- 6.4 Film

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Packaging

- 7.3 Textiles

- 7.4 Electronics

- 7.5 Pharmaceuticals

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alpla Group

- 9.2 Amcor

- 9.3 AVA Biochem

- 9.4 Avantium

- 9.5 BASF SE

- 9.6 Origin Materials

- 9.7 Sulzer

- 9.8 Swicofil

- 9.9 Toyobo