|

|

市場調査レポート

商品コード

1740875

持続可能な繊維加工機器市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Sustainable Textile Processing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 持続可能な繊維加工機器市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月28日

発行: Global Market Insights Inc.

ページ情報: 英文 487 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

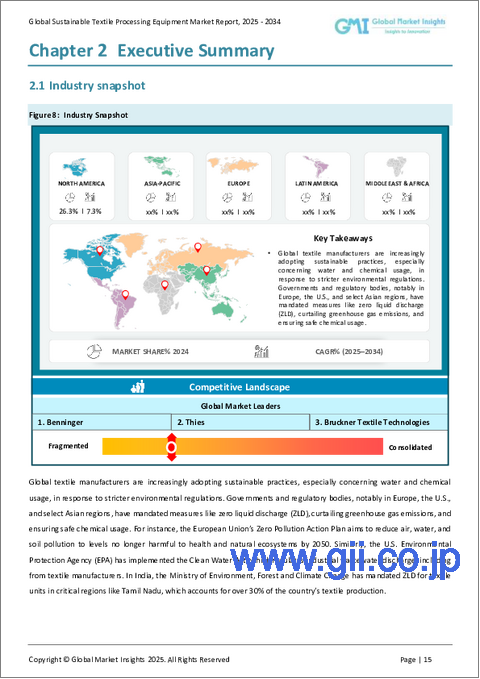

持続可能な繊維加工機器の世界市場規模は、2024年に15億米ドルとなり、CAGR7%で成長し、2034年には29億米ドルに達すると予測されています。

環境規制の強化、持続可能性に対する意識の高まり、消費者の期待の変化などが相まって、繊維メーカーは従来のプロセスを見直し、環境に優しい技術を取り入れる必要に迫られています。特に欧州、北米、アジアの一部などの地域では規制圧力が高まっており、排出削減、節水、安全な化学物質の取り扱いに重点を置いたガイドラインが施行されつつあります。その結果、繊維産業は新たな義務に対応し、急速に進化する世界市場で競争力を維持するため、よりクリーンで効率的な設備への投資を進めています。

サステイナブル・ファッションは引き続き人気を集めており、それに伴い、より環境に優しい生産工程が必要とされています。ブランドはサプライチェーンにより高い持続可能性基準を要求しており、加工業者は時代遅れで資源集約的な機械からの移行を余儀なくされています。このような背景から、業界全体が認める認証の取得が大きな目標となっており、環境への悪影響を低減するよう設計された高度な加工システムの普及を促しています。前処理と仕上げ作業の環境負荷を軽減することに重点を置いているため、水と化学薬品の使用を最小限に抑える機器は特に重要です。これらの機械は、環境保全の目標をサポートするだけでなく、廃水管理や排出ガス規制に関する進化する法的要求にも合致しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 15億米ドル |

| 予測金額 | 29億米ドル |

| CAGR | 7% |

さまざまな製品セグメントの中で、サステイナブル繊維洗濯機が市場で大きなシェアを占めています。2024年にこのセグメントは5億米ドルを超え、2034年には10億米ドルを超えると予想されます。水の使用量を削減し、化学薬品の効率を向上させる洗濯機への嗜好の高まりが、購買決定を形成しています。従来の洗浄システムは、大量の水を消費し、汚染度の高い廃水を発生させていました。最新の環境に優しい機種は、スマート・リサイクル・システム、逆流水設計、革新的な酵素処理技術を組み込んだ高度なソリューションを提供しています。これらの進歩により、繊維メーカーは環境基準を遵守しながら資源使用量を削減することができ、長期的な運営上のメリットを求めるメーカーにとっては価値ある投資となります。

技術面では、水なし処理が有力なソリューションとして台頭しており、2024年のシェアは36%で市場を独占しています。このアプローチは、世界の水不足と廃水汚染への懸念が強まるにつれて定着しつつあります。従来の染色・仕上げ方法は水に大きく依存しており、深刻な環境問題を引き起こしています。これに対応するため、メーカーは現在、水の使用をなくすか大幅に削減する方法を採用し、汚染された排水の高額な処理を回避しています。こうした水なし代替法は、厳しい環境基準を満たすのに役立つだけでなく、大規模な水処理インフラの必要性を減らすことで生産効率全体を向上させる。

持続可能な繊維機器分野では、米国が依然として有力なプレーヤーです。同国の市場規模は2024年に4億米ドル以上に達し、2034年には約7億米ドルにまで上昇すると予想されています。米国メーカーは、産業の持続可能性向上を目的とした連邦および州レベルの環境規制の複雑な情勢に対応しています。水消費量の削減、汚染の抑制、エネルギー効率の奨励にますます重点が置かれるようになっています。規制当局による施行は、環境に配慮した機械の採用拡大につながり、繊維産業全体に大きな変革を促しています。コンプライアンスを遵守するためには設備のアップグレードが不可欠となり、持続可能なソリューションへのシフトは着実に加速しています。

持続可能な繊維加工機器市場の企業は、市場での存在感を高め、環境に優しいソリューションへの需要の高まりに応えるため、革新的な戦略を積極的に採用しています。例えば、スイスの繊維機械メーカーは、エネルギー効率の高い技術で業界をリードしています。こうした取り組みは、持続可能性を中核業務に統合し、環境パフォーマンスと競合優位性の両方を強化しようという、より広範な業界の動向を反映しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- サプライヤーの情勢

- 利益率分析

- 技術概要

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 成長する繊維産業

- 技術的進歩

- 持続可能性への需要の高まり

- 規制強化の監視

- 業界の潜在的リスク&課題

- 初期コストが高め

- 規制当局の監視

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021-2032

- 主要動向

- 洗濯機

- 乾燥機

- 染色機

- 印刷機

- その他(繊維加工機械等)

第6章 市場推計・予測:技術別、2021-2034

- 主要動向

- 水なし処理

- 低アルコール染色

- 超臨界CO2染色

- プラズマ治療

- オゾン仕上げ

- その他(超音波技術など)

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- アパレル製造

- ホームテキスタイル

- テクニカルテキスタイル

- スポーツウェア

- 自動車用繊維

- その他(医療用繊維等)

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 繊維工場

- 衣料品メーカー

- 染色工場

- 繊維研究開発施設

- その他(受託製造部門等)

第9章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 直接

- 間接的

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- A.T.E. Enterprises

- Andritz Kusters

- Benninger

- Biancalani

- Bruckner Textile Technologies

- DiloGroup

- FONG’S

- Goller

- Jupiter Comtex

- Kratzer

- Lakshmi Machine Works

- Loris Bellini

- Monforts

- Santex Rimar Group

- Thies

The Global Sustainable Textile Processing Equipment Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 7% to reach USD 2.9 billion by 2034. A combination of stricter environmental regulations, increasing awareness about sustainability, and shifting consumer expectations is compelling textile manufacturers to overhaul traditional processes and embrace eco-friendly technologies. Regulatory pressure is mounting, especially in regions such as Europe, North America, and parts of Asia, where governing bodies are enforcing guidelines focused on emission reduction, water conservation, and safe chemical handling. As a result, textile businesses are investing in cleaner, more efficient equipment to comply with new mandates and to maintain their competitive standing in a rapidly evolving global market.

Sustainable fashion continues to gain traction, and with it comes the need for greener production processes. Brands are demanding higher sustainability standards from their supply chains, leading processors to transition away from outdated, resource-intensive machinery. In this context, achieving certifications recognized across the industry has become a major objective, encouraging the widespread adoption of advanced processing systems designed to reduce environmental harm. Equipment that minimizes water and chemical use is especially critical, given the focus on lessening the environmental burden of pre-treatment and finishing operations. These machines not only support conservation goals but also align with evolving legislative demands regarding wastewater management and emissions control.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.9 Billion |

| CAGR | 7% |

Among the different product segments, sustainable textile washing machines hold a major share of the market. In 2024, this segment exceeded USD 500 million and is expected to surpass USD 1 billion by 2034. The increasing preference for machines that reduce water usage and improve chemical efficiency is shaping purchasing decisions. Traditional washing systems consume excessive amounts of water and generate highly contaminated wastewater. Newer eco-friendly models offer advanced solutions, incorporating smart recycling systems, counterflow water designs, and innovative enzymatic treatment technologies. These advancements allow textile producers to cut back on resource usage while remaining compliant with environmental standards, making them a worthwhile investment for manufacturers seeking long-term operational benefits.

On the technology front, waterless processing is emerging as the leading solution, dominating the market with a 36% share in 2024. This approach is gaining ground as concerns about global water scarcity and wastewater pollution intensify. Traditional dyeing and finishing methods rely heavily on water, contributing to severe environmental issues. In response, manufacturers are now adopting methods that eliminate or drastically reduce water use, thereby avoiding the costly treatment of contaminated effluents. These waterless alternatives not only help in meeting strict environmental benchmarks but also enhance overall production efficiency by reducing the need for extensive water treatment infrastructure.

The United States remains a prominent player in the sustainable textile equipment space. The country's market size reached over USD 400 million in 2024 and is anticipated to climb to approximately USD 700 million by 2034. U.S. manufacturers are responding to a complex landscape of federal and state-level environmental regulations aimed at improving industrial sustainability. Policies are increasingly focused on reducing water consumption, controlling pollution, and encouraging energy efficiency. Enforcement by regulatory agencies has led to greater adoption of eco-conscious machinery, prompting a major transformation across the textile industry. As equipment upgrades become essential for compliance, the shift toward sustainable solutions is accelerating at a steady pace.

Companies in the sustainable textile processing equipment market are actively adopting innovative strategies to bolster their market presence and meet the growing demand for eco-friendly solutions. Swiss textile machinery manufacturers, for instance, are leading the way with energy-efficient technologies. These initiatives reflect a broader industry trend towards integrating sustainability into core operations, enhancing both environmental performance and competitive advantage.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.2 Price volatility in key materials

- 3.2.2.3 Supply chain restructuring

- 3.2.2.4 Production cost implications

- 3.2.2.5 Demand-side impact (selling price)

- 3.2.2.6 Price transmission to end markets

- 3.2.2.7 Market share dynamics

- 3.2.2.8 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Profit margin analysis

- 3.5 Technological overview

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Growing textile industry

- 3.8.1.2 Technological advancements

- 3.8.1.3 Increasing demand for sustainability

- 3.8.1.4 Growing regulatory scrutiny

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High initial cost

- 3.8.2.2 Regulatory scrutiny

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2032 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Washing machine

- 5.3 Drying machine

- 5.4 Dyeing machine

- 5.5 Printing machine

- 5.6 Others (fiber processing machine, etc.)

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2034 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Waterless processing

- 6.3 Low-liquor dyeing

- 6.4 Supercritical CO2 dyeing

- 6.5 Plasma treatment

- 6.6 Ozone finishing

- 6.7 Others (ultrasound technology, etc.)

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Apparel manufacturing

- 7.3 Home textiles

- 7.4 Technical textiles

- 7.5 Sportswear

- 7.6 Automotive textiles

- 7.7 Others (medical textile, etc.)

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Textile mills

- 8.3 Garment manufacturers

- 8.4 Dye houses

- 8.5 Textile R&D facilities

- 8.6 Others (contract manufacturing units, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 A.T.E. Enterprises

- 11.2 Andritz Kusters

- 11.3 Benninger

- 11.4 Biancalani

- 11.5 Bruckner Textile Technologies

- 11.6 DiloGroup

- 11.7 FONG’S

- 11.8 Goller

- 11.9 Jupiter Comtex

- 11.10 Kratzer

- 11.11 Lakshmi Machine Works

- 11.12 Loris Bellini

- 11.13 Monforts

- 11.14 Santex Rimar Group

- 11.15 Thies