|

市場調査レポート

商品コード

1740818

ステアリングタイロッドの市場機会、成長促進要因、産業動向分析と2025年~2034年予測Steering Tie Rod Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ステアリングタイロッドの市場機会、成長促進要因、産業動向分析と2025年~2034年予測 |

|

出版日: 2025年04月29日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

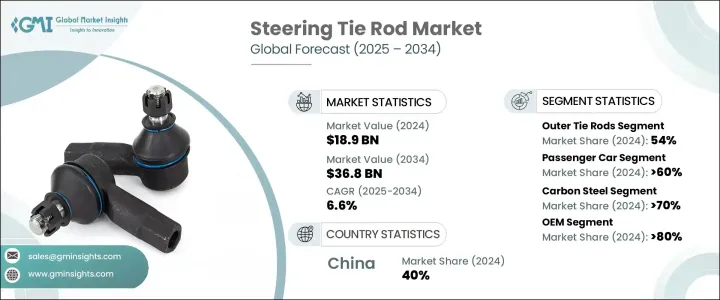

ステアリングタイロッドの世界市場規模は、2024年に189億米ドルとなり、CAGR 6.6%で成長し、2034年には368億米ドルに達すると予測されています。

この成長の主な要因は、自動車産業の急速な拡大であり、特に工業化と都市開発が急速に進んでいる地域で顕著です。より多くの人々がより高い可処分所得を得られるようになり、インフラが改善されるにつれて、自動車需要が大幅に増加します。自動車生産台数の急増は、当然のことながら、ステアリング・タイ・ロッドのような、適切な車両制御を維持し、路上での安全を確保するために不可欠な重要部品の需要増につながります。自動車の性能と寿命に対する期待が高まるにつれ、自動車メーカーと消費者は同様に、現代の走行条件に耐えることができる、高度で耐久性のあるステアリングシステムを求めています。

ステアリング・システムは、自動車技術の革新が自動車セクターの形を変え続けているため、著しい変貌を遂げています。電動パワーステアリング、ステア・バイ・ワイヤ構成、センサーの組み込みといった最新の進歩は、より広まりつつあります。こうした開発は、単に自動車の性能を向上させるだけでなく、燃費効率を高め、より安全な運転を可能にしています。自動車がよりスマートになり、エレクトロニクスへの依存度が高まるにつれ、ステアリング・タイ・ロッドのような精密に設計された部品への需要がさらに重要になっています。これらの部品は、高度なステアリングシステムとの最適な統合を保証するために、より高い精度と信頼性の基準を満たす必要があります。自動化と電子運転支援へのシフトは、精度、最小限の機械的複雑さ、ハンドリングの改善を実現できる部品へのニーズを強めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 189億米ドル |

| 予測金額 | 368億米ドル |

| CAGR | 6.6% |

製品セグメンテーションでは、市場はインナータイロッドとアウタータイロッドに分けられます。アウタータイロッドは2024年に市場の約54%を占め、圧倒的な地位を占めており、予測期間を通じてCAGR 7.2%で成長すると予測されます。これらの部品は、外部に配置されているため交換頻度が高く、環境暴露や摩耗に対してより脆弱です。道路の破片、湿気、過酷な要素に常にさらされているため、劣化が早まる。期限内に交換されない場合、摩耗したアウタータイロッドは、ステアリングレスポンスの低下やタイヤの不均一な摩耗の原因となります。このため、自動車アフターマーケットでの需要が増加し、アウター・タイロッドは収益を牽引する重要なセグメントとなっています。

市場を車種別に見ると、乗用車は2024年の総販売台数の60%以上を占め、2034年まで約6%のCAGRで拡大し続けると予想されます。乗用車は使用期間が長くなる傾向があり、経年劣化に伴って継続的なメンテナンスが必要となるため、交換部品に対する安定した需要が見込まれます。ステアリング・タイロッドは、車両の安全なハンドリングに不可欠であるため、特に走行距離が多い場合や悪路を走行する場合には、定期的な点検と交換が必要になることが多いです。世界的に運転されている乗用車の数が増加しているため、OEMおよびアフターマーケット両方のタイロッド製品に対するニーズが持続しており、市場全体におけるこのセグメントの主導的地位が強化されています。

材料別では、炭素鋼が2024年にステアリング・タイロッドの製造に好まれる選択肢として浮上し、市場シェアの70%以上を占めました。炭素鋼の人気は、高い強度と耐久性の組み合わせに起因しており、長期にわたる継続的な応力と路面からの衝撃に耐えることができます。炭素鋼はまた、アルミニウムやチタンのような代替材料よりもコスト面で有利なため、メーカーは高性能部品を競争力のある価格で提供することができます。このような品質と費用対効果のバランスにより、炭素鋼は、特に自動車部品のような価格に敏感な市場において、OEMとアフターマーケットサプライヤーの両方にとって実用的な選択肢となっています。

販売チャネルの観点から見ると、OEMは2024年のステアリングタイロッド市場の80%以上を占めています。OEMの存在感が強いのは、自動車組立時に純正部品が必要とされるためです。OEM部品は、新車の仕様と正確に一致するように設計されており、性能と互換性を保証する保証が付いています。自動車メーカーは、一貫性、品質保証、車両のオリジナル・エンジニアリング設計をサポートする能力から、これらの部品を好みます。世界の自動車生産の伸びが、このセグメントの需要を大きく牽引しています。

地域的には、中国が2024年の世界シェアの40%近くを占めて市場をリードし、約164億米ドルの売上を生み出しました。このリーダーシップは、同国の自動車生産台数の多さと、自動車部品のサプライチェーンが確立されていることに支えられています。中国は、メーカーとサプライヤーの強力な基盤の恩恵を受けており、ステアリング・タイ・ロッドの効率的な生産と広範な流通を可能にしています。競合価格と高品質規格の組み合わせにより、現地生産者は国内外からの需要に効果的に対応しています。

世界プレーヤーは、製品ラインを拡大し、先進技術を統合するために投資を続けています。戦略的パートナーシップと研究開発イニシアティブは、製品の性能と耐久性を高めるために利用されています。これらの企業は、ステアバイワイヤや電動ステアリングシステムのような革新技術を採用し、最新の自動車市場の進化する需要に沿った製品を提供しています。一方、各地域のメーカー各社は、その地域の要件に合わせて製品をカスタマイズすることに注力し、特定の車種や走行環境に対応したカスタマイズ・ソリューションを提供しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 自動車OEM

- サプライヤー

- 材料および鍛造会社

- アフターマーケットの販売代理店および小売業者

- 最終用途

- サプライヤーの情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 主要原材料の価格変動

- サプライチェーンの再構築

- 最終市場への価格伝達

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 貿易への影響

- 価格動向

- 地域

- 製品

- コスト内訳分析

- 利益率分析

- テクノロジーとイノベーションの情勢

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 世界の自動車生産の増加

- ステアリングシステムの技術的進歩

- 車両の安全性と規制遵守を重視

- 電気自動車と自動運転車の成長

- 業界の潜在的リスク&課題

- 電気自動車と自動運転技術による破壊的変化

- 原材料価格の変動とサプライチェーンの混乱

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- インナータイロッド

- アウタータイロッド

第6章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 軽商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第7章 市場推計・予測:材料別、2021-2034

- 主要動向

- 炭素鋼

- ステンレス鋼

第8章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- ACDelco

- APA Industries

- BorgWarner

- Bosch Group

- Crown Automotive Sales

- CTR

- Delphi Technologies

- Dorman Products

- First Line

- HL Mando

- Ingalls Engineering

- JTEKT

- Mando

- Moog

- Motorcraft

- Nexteer Automotive Group Limited

- NSK

- Sankei Industry

- Synergy Manufacturing

- ZF Friedrichshafen

The Global Steering Tie Rod Market was valued at USD 18.9 billion in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 36.8 billion by 2034. This growth is primarily fueled by the rapid expansion of the automotive industry, especially in regions undergoing fast-paced industrialization and urban development. As more people gain access to higher disposable incomes and infrastructure improves, the demand for vehicles rises significantly. The surge in vehicle production naturally translates into higher demand for crucial components like steering tie rods, which are essential for maintaining proper vehicle control and ensuring safety on the road. With growing expectations for vehicle performance and longevity, automakers and consumers alike are demanding advanced, durable steering systems that can withstand modern driving conditions.

The steering system is undergoing a notable transformation as innovations in vehicle technology continue to reshape the automotive sector. Modern advancements such as electric power steering, steer-by-wire configurations, and the incorporation of sensors are becoming more widespread. These developments are not just enhancing vehicle performance-they are also making cars more fuel-efficient and safer to drive. As vehicles become smarter and more reliant on electronics, the demand for precisely engineered parts like steering tie rods becomes even more important. These components must now meet higher standards of accuracy and reliability to ensure optimal integration with advanced steering systems. The shift toward automation and electronic driving assistance has intensified the need for parts that can deliver precision, minimal mechanical complexity, and improved handling.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.9 Billion |

| Forecast Value | $36.8 Billion |

| CAGR | 6.6% |

In terms of product segmentation, the market is divided into inner and outer tie rods. Outer tie rods held the dominant position in 2024, accounting for around 54% of the market, and are projected to grow at a CAGR of 7.2% throughout the forecast period. These components face more frequent replacements due to their external position, which makes them more vulnerable to environmental exposure and wear. Being constantly subjected to road debris, moisture, and harsh elements leads to quicker degradation. When not replaced in time, worn-out outer tie rods can contribute to poor steering response and uneven tire wear. This naturally increases demand within the automotive aftermarket, making outer tie rods a crucial revenue-driving segment.

When examining the market by vehicle type, passenger cars represented more than 60% of total sales in 2024 and are expected to continue expanding at a CAGR of approximately 6% through 2034. Passenger vehicles tend to remain in service longer and require ongoing maintenance as they age, leading to consistent demand for replacement parts. Steering tie rods, being critical to safe vehicle handling, often need periodic inspection and substitution, especially in high-mileage or rough-road driving scenarios. The growing number of passenger cars in operation globally ensures a sustained need for both OEM and aftermarket tie rod products, reinforcing this segment's leading position in the overall market.

Material-wise, carbon steel emerged as the preferred choice for manufacturing steering tie rods in 2024, accounting for over 70% of the market share. Its popularity stems from a combination of high strength and durability, allowing it to endure continuous stress and road shocks over time. Carbon steel also offers a cost advantage over alternative materials like aluminum or titanium, enabling manufacturers to deliver high-performance parts at competitive pricing. This balance of quality and cost-effectiveness makes carbon steel a practical option for both OEMs and aftermarket suppliers, especially in a price-sensitive market like automotive components.

From a sales channel perspective, OEMs captured more than 80% of the steering tie rod market in 2024. The strong presence of OEMs can be attributed to the need for original parts during vehicle assembly. OEM components are designed to match the exact specifications of new vehicles and come with warranties that assure performance and compatibility. Automakers prefer these components for their consistency, quality assurance, and the ability to support the vehicle's original engineering design. The growth in global vehicle production has significantly driven demand from this segment.

Geographically, China led the market in 2024 with nearly 40% of the global share, generating around USD 16.4 billion in revenue. This leadership is supported by the country's high volume of vehicle production and a well-established supply chain for automotive components. China benefits from a strong base of manufacturers and suppliers, enabling efficient production and widespread distribution of steering tie rods. Competitive pricing, combined with high-quality standards, has allowed local producers to meet both domestic and international demands effectively.

Global players continue to invest in expanding their product lines and integrating advanced technologies. Strategic partnerships and R&D initiatives are being used to enhance product performance and durability. These companies are embracing innovations like steer-by-wire and electric steering systems, ensuring their offerings align with the evolving demands of the modern automotive market. Meanwhile, regional manufacturers focus on tailoring their products to local requirements, offering customized solutions that resonate with specific vehicle types and driving environments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Automotive OEMs

- 3.1.2 Suppliers

- 3.1.3 Material and forging companies

- 3.1.4 Aftermarket distributors and retailers

- 3.1.5 End use

- 3.2 Supplier landscape

- 3.3 Impact of trump administration tariffs

- 3.3.1 Impact on trade

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on the industry

- 3.3.2.1 Price volatility in key materials

- 3.3.2.2 Supply chain restructuring

- 3.3.2.3 Price transmission to end markets

- 3.3.3 Strategic industry responses

- 3.3.3.1 Supply chain reconfiguration

- 3.3.3.2 Pricing and product strategies

- 3.3.1 Impact on trade

- 3.4 Price trend

- 3.4.1 Region

- 3.4.2 Product

- 3.5 Cost breakdown analysis

- 3.6 Profit margin analysis

- 3.7 Technology & innovation landscape

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising global automotive production

- 3.10.1.2 Technological advancements in steering systems

- 3.10.1.3 Emphasis on vehicle safety and regulatory compliance

- 3.10.1.4 Growth in electric and autonomous vehicles

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Disruption from electric and autonomous vehicle technologies

- 3.10.2.2 Fluctuating raw material prices and supply chain disruptions

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021-2034, ($Bn, Units)

- 5.1 Key trends

- 5.2 Inner tie rods

- 5.3 Outer tie rods

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021-2034, ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicle (LCV)

- 6.3.2 Medium commercial vehicle (MCV)

- 6.3.3 Heavy commercial vehicle (HCV)

Chapter 7 Market Estimates & Forecast, By Material, 2021-2034, ($Bn, Units)

- 7.1 Key trends

- 7.2 Carbon steel

- 7.3 Stainless steel

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021-2034, ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 ACDelco

- 10.2 APA Industries

- 10.3 BorgWarner

- 10.4 Bosch Group

- 10.5 Crown Automotive Sales

- 10.6 CTR

- 10.7 Delphi Technologies

- 10.8 Dorman Products

- 10.9 First Line

- 10.10 HL Mando

- 10.11 Ingalls Engineering

- 10.12 JTEKT

- 10.13 Mando

- 10.14 Moog

- 10.15 Motorcraft

- 10.16 Nexteer Automotive Group Limited

- 10.17 NSK

- 10.18 Sankei Industry

- 10.19 Synergy Manufacturing

- 10.20 ZF Friedrichshafen