|

市場調査レポート

商品コード

1698269

eコーナーシステム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測e-Corner System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| eコーナーシステム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月05日

発行: Global Market Insights Inc.

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

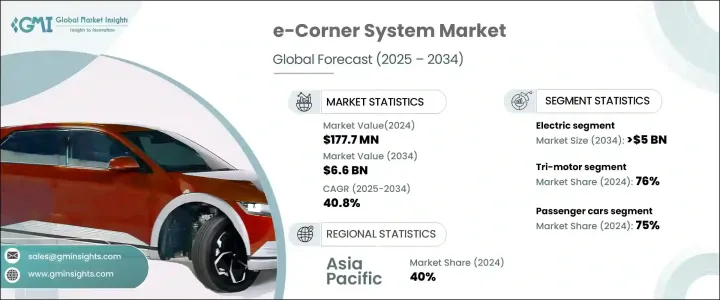

世界のeコーナーシステム市場は2024年に1億7,770万米ドルと評価され、電気自動車(EV)の普及と先進的な車両制御システムの推進により、2025年から2034年にかけて40.8%のCAGRで顕著に拡大すると予測されています。

この急激な成長は、自動車産業が電動化へと移行し、メーカーが持続可能性、効率、走行性能の強化に注力していることが背景にあります。

eコーナーシステムは、ステアリング、ブレーキ、サスペンション、推進力を各車輪に統合することで、EV設計に革命をもたらしています。この技術は、車両の操縦性を高め、正確なトルク制御と安定性の向上を可能にします。自動車メーカーは、エネルギー消費を最適化し、バッテリーの航続距離を延ばす革新的なソリューションを求めて、eコーナーシステムの採用を増やしています。世界各国の政府がより厳しい排ガス規制を実施し、ゼロ・エミッション車を推進する中、こうした先進システムの需要は急増すると予想されます。インテリジェントでアダプティブなモビリティ・ソリューションへの嗜好の高まりが市場拡大をさらに後押ししており、eコーナーシステムは次世代EVの重要なコンポーネントとして位置づけられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1億7,770万米ドル |

| 予測金額 | 66億米ドル |

| CAGR | 40.8% |

推進タイプ別にセグメント化すると、eコーナーシステム市場には電気自動車と内燃機関(ICE)車が含まれます。2024年には電気セグメントが市場シェアの80%を占め、2034年には50億米ドルに達すると予測されています。EVの普及がこの動向を後押しする重要な要因であり、eコーナーシステムは推進効率を最適化し、車両のハンドリングを改善する上で重要な役割を果たしています。これらのシステムは、各車輪の動きを正確に制御することを可能にし、トラクション、安全性、全体的な運転体験を向上させる。世界のEV販売台数が増加傾向にあることから、e-Corner技術の採用は加速すると予想され、自動車工学の将来における重要性がさらに高まっています。

同市場はモーター構成によっても分類され、トライモーターとクアッドモーターが主な選択肢となっています。2024年には、トライモーター・セグメントが市場シェアの76%を占め、優れたトルク配分と強化された車両ダイナミクスを提供します。トライモーター構成は、各ホイールへのパワー配分を最適化し、複雑な走行条件下でのトラクションとコントロールを向上させる。自動車メーカーは、より優れたハンドリング、安定性、性能を実現するため、パワートレイン技術の改良に投資しています。業界が先進的な車両制御システムを優先し続ける中、トライモーター・セットアップは、プレミアムEVや高性能EVにとって好ましい選択肢であり続けています。

地域別では、アジア太平洋市場が2024年に40%のシェアを占める。中国、日本、韓国の自動車メーカーは、先進的な推進・ハンドリング・ソリューションに多額の投資を行っており、eコーナーシステムは現代の電動モビリティにおける重要な技術となっています。エネルギー効率に優れたソリューションが強く求められる中、政府とメーカーは、自動車の安全性と効率を高めるため、高性能で差別化された制御システムの開発に注力しています。アジア太平洋地域でEVの需要が急増し続ける中、eコーナーシステム市場は大幅な成長を遂げ、自動車産業における変革技術としての役割を強化しています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 部品メーカー

- 技術プロバイダー

- 自動車メーカー

- サプライヤー&ディストリビューター

- 最終用途

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュースと取り組み

- 規制状況

- ケーススタディ

- 費用対効果分析

- 影響要因

- 促進要因

- 車両操縦性の向上と高度な駐車ソリューションに対する需要の高まり

- ステア・バイ・ワイヤおよびブレーキ・バイ・ワイヤ技術を統合した自律走行車および電気自動車の採用増加

- 車両の安全性、安定性、動的制御への注目の高まり

- インホイールモーター技術とモジュール式Eコーナーアーキテクチャの進歩

- 業界の潜在的リスク&課題

- 高い開発コストと統合コスト

- 規制と標準化の課題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:モーター構成別、2021年~2034年

- 主要動向

- トライモーター構成

- クアッドモーター構成

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第7章 市場推計・予測:推進別、2021年~2034年

- 主要動向

- ICE

- 電気自動車

- BEV

- HEV

- PHEV

- FCEV

第8章 市場推計・予測:車両形態別、2021年~2034年

- 主要動向

- 2輪駆動(2WD)

- 全輪駆動(AWD)

- 4輪駆動(4WD)

第9章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 油圧

- 電動

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Aptiv

- Benteler

- Canoo

- Continental

- Denso

- Elaphe

- Faurecia

- GKN Automotive

- Hitachi

- Hyundai

- Indigo Technologies

- Mitsubishi

- Nissan

- Protean Electric

- REE Automotive

- Schaeffler

- Siemens

- Valeo

- Zeekr

- ZF Friedrichshafen

The Global e-Corner System Market, valued at USD 177.7 million in 2024, is projected to expand at a remarkable CAGR of 40.8% between 2025 and 2034, driven by the increasing adoption of electric vehicles (EVs) and the push for advanced vehicle control systems. This exponential growth is fueled by the automotive industry's transition toward electrification, with manufacturers focusing on sustainability, efficiency, and enhanced driving performance.

The e-Corner system is revolutionizing EV design by integrating steering, braking, suspension, and propulsion into each wheel. This technology enhances vehicle maneuverability, allowing for precise torque control and improved stability. Automakers are increasingly adopting e-Corner systems as they seek innovative solutions to optimize energy consumption and extend battery range. As governments worldwide implement stricter emission regulations and promote zero-emission vehicles, the demand for these advanced systems is expected to surge. The growing preference for intelligent and adaptive mobility solutions is further boosting market expansion, positioning e-Corner systems as a critical component in next-generation EVs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $177.7 Million |

| Forecast Value | $6.6 Billion |

| CAGR | 40.8% |

Segmented by propulsion type, the e-Corner system market includes electric and internal combustion engine (ICE) vehicles. The electric segment dominated in 2024, capturing 80% of the market share, and is projected to generate USD 5 billion by 2034. The rise in EV adoption is a significant factor driving this trend, as e-Corner systems play a crucial role in optimizing propulsion efficiency and improving vehicle handling. These systems enable precise control over each wheel's movement, enhancing traction, safety, and overall driving experience. With global EV sales on the rise, the adoption of e-Corner technology is expected to accelerate, further cementing its importance in the future of automotive engineering.

The market is also categorized by motor configuration, with tri-motor and quad-motor setups being the primary options. In 2024, the tri-motor segment accounted for 76% of the market share, offering superior torque distribution and enhanced vehicle dynamics. Tri-motor configurations optimize power allocation across individual wheels, improving traction and control in complex driving conditions. Automakers are investing in refining powertrain technologies to deliver better handling, stability, and performance. As the industry continues to prioritize advanced vehicle control systems, tri-motor setups remain the preferred choice for premium and high-performance EVs.

Regionally, the Asia Pacific market held a 40% share in 2024, driven by the region's rapidly expanding EV sector. Automakers across China, Japan, and South Korea are heavily investing in advanced propulsion and handling solutions, making e-Corner systems a key technology in modern electric mobility. With a strong push for energy-efficient solutions, governments and manufacturers are focusing on the development of high-performance, differentiated control systems to enhance vehicle safety and efficiency. As demand for EVs continues to surge across Asia Pacific, the e-Corner system market is poised for substantial growth, reinforcing its role as a transformative technology in the automotive industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Component manufacturers

- 3.1.2 Technology providers

- 3.1.3 Automotive manufacturers

- 3.1.4 Suppliers & distributors

- 3.1.5 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Case studies

- 3.9 Cost-benefit analysis

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Growing demand for enhanced vehicle maneuverability and advanced parking solutions

- 3.10.1.2 Rising adoption of autonomous and electric vehicles integrating steer-by-wire and brake-by-wire technologies

- 3.10.1.3 Increasing focus on vehicle safety, stability, and dynamic control

- 3.10.1.4 Advancements in in-wheel motor technology and modular e-corner architectures

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High development and integration costs

- 3.10.2.2 Regulatory and standardization challenges

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Motor Configuration, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Tri-motor configuration

- 5.3 Quad-motor configuration

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedans

- 6.2.2 Hatchbacks

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric

- 7.3.1 BEV

- 7.3.2 HEV

- 7.3.3 PHEV

- 7.3.4 FCEV

Chapter 8 Market Estimates & Forecast, By Vehicle Configuration, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 2-Wheel Drive (2WD)

- 8.3 All-Wheel Drive (AWD)

- 8.4 4-Wheel Drive (4WD)

Chapter 9 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Hydraulic

- 9.3 Electric

- 9.4 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aptiv

- 11.2 Benteler

- 11.3 Canoo

- 11.4 Continental

- 11.5 Denso

- 11.6 Elaphe

- 11.7 Faurecia

- 11.8 GKN Automotive

- 11.9 Hitachi

- 11.10 Hyundai

- 11.11 Indigo Technologies

- 11.12 Mitsubishi

- 11.13 Nissan

- 11.14 Protean Electric

- 11.15 REE Automotive

- 11.16 Schaeffler

- 11.17 Siemens

- 11.18 Valeo

- 11.19 Zeekr

- 11.20 ZF Friedrichshafen