|

市場調査レポート

商品コード

1740816

自動車用カムシャフトの市場機会、成長促進要因、産業動向分析、2025~2034年予測Automotive Camshaft Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用カムシャフトの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月30日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

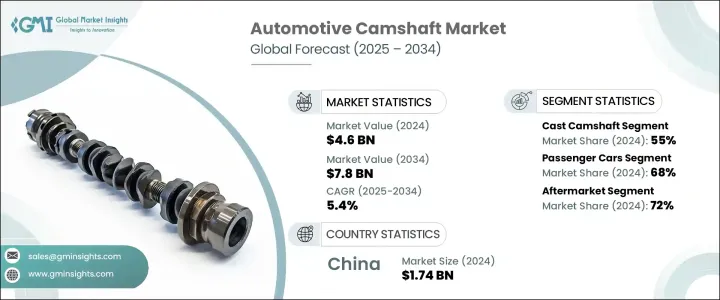

自動車用カムシャフトの世界市場規模は、2024年に46億米ドルとなり、CAGR 5.4%で成長し、2034年には78億米ドルに達すると予測されています。

この成長には、高性能エンジンへのニーズの高まりと、世界の自動車生産の一貫した増加が寄与しています。乗用車メーカーも商用車メーカーも最新のエンジン技術を採用し、カムシャフトをエンジン強化戦略の中核に据えています。自動車メーカーは、軽量素材、精密工学、可変バルブタイミングなどの先進技術を統合した次世代カムシャフト設計に投資しています。これらの技術革新は、出力を最適化し、燃費を向上させ、排出ガスを削減すると同時に、さまざまな車両クラスでスムーズな加速と応答性の向上を実現します。また、カムシャフトはエンジンの長寿命化にも貢献しており、高性能モデルだけでなく、日常的な自動車にも欠かせないものとなっています。エンジン性能と燃費の向上への関心が高まっているのは、北米に限ったことではないです。可処分所得の増加、自動車所有の増加、効率的な自動車への需要の高まりが、アジア太平洋とラテンアメリカの新興市場での旺盛な需要を牽引しています。このような動向は、世界中でカムシャフトの開発と製造の将来を形作る一助となっています。

市場セグメンテーションは、製品別に鋳造、鍛造、組立カムシャフトに区分されます。鋳造カムシャフトは2024年に市場の約55%を占め、2034年までのCAGRは6%以上で成長すると予測されています。鋳造カムシャフトが広く使用されているのは、コスト効率が高く、大量生産が容易なためです。鋳造カムシャフトは、特にエコノミーおよびミッドレンジセグメントの車両向けの大規模製造において、引き続き最有力候補です。改善された冶金方法や金型設計などの鋳造技術の進歩は、鋳造カムシャフトの性能と耐久性の向上に役立っています。これらの開発により、鋳造カムシャフトは鍛造カムシャフトと競合し、その優位性をより強固なものにしています。鋳造カムシャフトは、鍛造カムシャフトよりも製造コストが低く、先進国市場と新興国市場の両方で採用されている主な要因です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 46億米ドル |

| 予測金額 | 78億米ドル |

| CAGR | 5.4% |

車種別では、カムシャフト市場は乗用車と商用車に分けられます。乗用車は2024年に市場の68%を占めて最大のシェアを占め、このセグメントは2034年までCAGR 5%以上で成長すると予想されます。この動向を支えているのは、特に発展途上地域における自動車生産の増加です。ターボチャージングや可変バルブタイミングなどの技術によりエンジンシステムが高度化するにつれ、これらの改良に対応できるカムシャフトの需要が高まっています。厳しい排ガス規制も、自動車メーカーにより高度なカムシャフト技術の統合を促しています。内燃機関を使用し続けるハイブリッド車や電気自動車は、性能と効率をバランスさせるように設計された特注カムシャフトの需要をさらに高めています。

販売チャネルに関しては、市場は相手先商標製品メーカー(OEM)とアフターマーケットに分類されます。2024年の市場シェアはアフターマーケット部門が72%で優位を占めており、2025年から2034年までのCAGRは6%以上で成長すると予測されています。自動車の所有者の中には、自分でアップグレードやカスタマイズを行う人が増えており、アフターマーケットのカムシャフト製品の人気が高まっています。これらの部品はeコマースプラットフォームで簡単に入手できるため、消費者は製品を比較し、レビューを読み、十分な情報を得た上で購入することができます。SUV、ピックアップトラック、オフロードモデルなどの車両では、高性能部品が必要とされ、特にこの分野を牽引しています。メーカー各社は、出力と燃費のニーズに対応する性能特化型カムシャフトのイノベーションで、この需要に応えています。

2024年には、中国がアジア太平洋地域で圧倒的な地位を占め、市場全体の約38%を占め、17億4,000万米ドルの売上を生み出しました。自動車保有台数の継続的な増加と、エネルギー効率の高い輸送を目指す政府の後押しが、最新のカムシャフト技術への需要を支えています。また、同国の強固な自動車製造エコシステムは、OEMとアフターマーケットの両チャネルで安定した需要を確保する上で重要な役割を果たしています。都市部の消費者は、性能アップグレードのために耐久性が高く手頃な価格のカムシャフトを求めるようになっており、これがこの主要地域におけるアフターマーケット分野の拡大を支えています。

自動車用カムシャフト分野の主要企業には、精密工学と高強度材料で限界に課題する世界の主要メーカーが含まれます。これらの企業は、スマートカムシャフトシステムと可変バルブタイミング機能の統合に注力しており、これによりエンジンはさまざまな走行条件に適応し、燃料使用量を改善することができます。これらの技術は、ハイブリッド車や将来の車両プラットフォームに不可欠なものとなっており、カムシャフトは、すべての車両カテゴリーで信頼性が高く高性能なエンジンを確保しながら、最新の効率と排出ガス基準を満たすために重要なコンポーネントであり続けています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 製造業者

- 原材料サプライヤー

- 自動車OEM

- 流通チャネル

- 最終用途

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 価格動向分析

- 製品

- 地域

- コスト内訳分析

- 影響要因

- 促進要因

- 世界の自動車生産の増加

- エンジン設計における技術的進歩

- 高性能車や高級車の需要増加

- 材料と製造の改善

- ハイブリッド車の導入

- 業界の潜在的リスク&課題

- 製造業への高額な資本投資

- 電気自動車(EV)への移行

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 鋳造カムシャフト

- 鍛造カムシャフト

- 組み立てられたカムシャフト

第6章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車

- 中型商用車

- 大型商用車

第7章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第9章 企業プロファイル

- Aichi Forge

- Camshaft Machine

- Comp Performance

- Crane Cams

- Elgin Industries

- Engine Power Components

- Estas Camshaft

- Hirschvogel

- JD Norman

- KAUTEX TEXTRON

- Linamar

- Mahle

- Musashi Seimitsu

- Piper Cams

- Precision Camshafts

- Riken

- Schaeffler

- Shadbolt

- ThyssenKrupp

- Varroc Group

The Global Automotive Camshaft Market was valued at USD 4.6 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 7.8 billion by 2034. This growth is being fueled by the increasing need for high-performance engines and the consistent rise in vehicle production across the globe. Both passenger and commercial vehicle manufacturers are adopting modern engine technologies, placing camshafts at the core of engine enhancement strategies. Automakers are investing in next-generation camshaft designs that integrate lightweight materials, precision engineering, and advanced technologies like variable valve timing. These innovations help optimize power output, enhance fuel efficiency, and reduce emissions while ensuring smoother acceleration and improved responsiveness in various vehicle classes. Camshafts are also instrumental in extending engine longevity, making them essential not just for high-performance models but also for everyday vehicles. The growing interest in enhanced engine performance and fuel economy is not limited to North America. Rising disposable income, increased vehicle ownership, and a growing demand for efficient vehicles are driving strong demand in emerging markets across Asia-Pacific and Latin America. This widespread trend is helping to shape the future of camshaft development and manufacturing around the world.

The automotive camshaft market is segmented by product into cast, forged, and assembled camshafts. Cast camshafts accounted for approximately 55% of the market in 2024 and are projected to grow at a CAGR of over 6% through 2034. Their widespread use is attributed to their cost-efficiency and the ease of mass production. Cast camshafts continue to be the top choice for large-scale manufacturing, particularly for vehicles in the economy and mid-range segments. Advancements in casting techniques, such as improved metallurgical methods and mold designs, are helping enhance the performance and durability of cast camshafts. These developments make cast versions more competitive with forged alternatives, further solidifying their dominance. Cast camshafts are substantially more affordable to produce than forged ones, a key factor contributing to their adoption in both developed and emerging automotive markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.6 Billion |

| Forecast Value | $7.8 Billion |

| CAGR | 5.4% |

When it comes to vehicle types, the camshaft market is divided into passenger cars and commercial vehicles. Passenger cars held the largest share in 2024, accounting for 68% of the market, and this segment is expected to grow at a CAGR of more than 5% through 2034. Increasing vehicle production, especially in developing regions, continues to support this trend. As engine systems become more advanced with technologies like turbocharging and variable valve timing, the demand for camshafts that can keep up with these improvements is rising. Stringent emissions standards are also encouraging automakers to integrate more sophisticated camshaft technologies. Hybrid and electric vehicles that continue to use internal combustion engines further boost the demand for custom-engineered camshafts designed to balance performance and efficiency.

In terms of sales channels, the market is categorized into original equipment manufacturers (OEMs) and the aftermarket. The aftermarket segment dominated in 2024 with a market share of 72% and is projected to grow at a CAGR of more than 6% from 2025 to 2034. A growing number of vehicle owners are turning to do-it-yourself upgrades and customizations, increasing the popularity of aftermarket camshaft products. These components are easily accessible via e-commerce platforms, allowing consumers to compare products, read reviews, and make informed purchases. The need for high-performance components in vehicles such as SUVs, pickup trucks, and off-road models is especially driving this segment. Manufacturers are responding to the demand with performance-specific camshaft innovations that cater to power and fuel efficiency needs.

In 2024, China held a dominant position in the Asia-Pacific region, capturing about 38% of the total market and generating USD 1.74 billion in revenue. Continued growth in vehicle ownership and the government's push toward energy-efficient transportation are sustaining demand for modern camshaft technologies. The robust automotive manufacturing ecosystem in the country also plays a significant role in ensuring consistent demand across both OEM and aftermarket channels. Urban consumers are increasingly seeking durable and affordable camshafts for performance upgrades, which supports the expansion of the aftermarket segment in this key region.

Leading companies in the automotive camshaft space include major global manufacturers that are pushing boundaries with precision engineering and high-strength materials. These players are focused on smart camshaft systems and integrating variable valve timing features, which allow engines to adapt to different driving conditions and improve fuel usage. With these technologies becoming vital in hybrid and future vehicle platforms, camshafts remain a critical component in meeting modern efficiency and emissions standards while ensuring reliable and high-performing engines across all vehicle categories.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Raw material suppliers

- 3.2.3 Automotive OEM

- 3.2.4 Distribution channel

- 3.2.5 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Pricing trend analysis

- 3.9.1 Product

- 3.9.2 Region

- 3.10 Cost breakdown analysis

- 3.11 Impact on forces

- 3.11.1 Growth drivers

- 3.11.1.1 Rising global vehicle production

- 3.11.1.2 Technological advancements in engine design

- 3.11.1.3 Increased demand for performance and luxury vehicles

- 3.11.1.4 Improvements in materials and manufacturing

- 3.11.1.5 Hybrid vehicle adoption

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High capital investment for manufacturing

- 3.11.2.2 Shifts toward electric vehicles (EVs)

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Cast camshaft

- 5.3 Forged camshaft

- 5.4 Assembled camshaft

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles

- 6.3.2 Medium commercial vehicles

- 6.3.3 Heavy commercial vehicles

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Aichi Forge

- 9.2 Camshaft Machine

- 9.3 Comp Performance

- 9.4 Crane Cams

- 9.5 Elgin Industries

- 9.6 Engine Power Components

- 9.7 Estas Camshaft

- 9.8 Hirschvogel

- 9.9 JD Norman

- 9.10 KAUTEX TEXTRON

- 9.11 Linamar

- 9.12 Mahle

- 9.13 Musashi Seimitsu

- 9.14 Piper Cams

- 9.15 Precision Camshafts

- 9.16 Riken

- 9.17 Schaeffler

- 9.18 Shadbolt

- 9.19 ThyssenKrupp

- 9.20 Varroc Group