水冷変圧器市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Water Cooled Transformer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740789

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

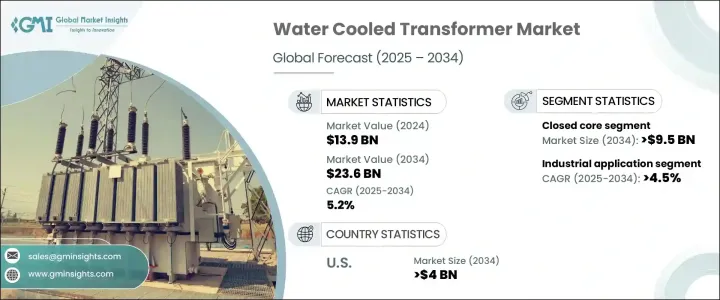

世界の水冷変圧器市場は2024年に139億米ドルと評価され、エネルギー需要の急増、熱管理システムの革新、大型産業や公益事業における高性能ソリューションの緊急ニーズなどを背景に、CAGR 5.2%で成長し、2034年には236億米ドルに達すると予測されています。

世界の電力インフラが進化するにつれ、産業界は効率性、信頼性、長寿命を確保する技術を求めています。水冷式変圧器は、コンパクトでありながら大容量の電源セットアップを必要とする業務、特に放熱が重要な業務に最適な選択肢となりつつあります。エネルギー使用を最適化し、機器のダウンタイムを最小化するというプレッシャーが高まる中、企業は設置面積や拡張性を犠牲にすることなく、優れた熱管理を実現する冷却ソリューションに多額の投資を行っています。都市化、スマートシティプロジェクト、再生可能エネルギー統合の動向は、効果的な熱制御と運転寿命の延長が譲れないコンパクトなモジュール式変電所への需要をさらに高めています。

今日の業界情勢は、変圧器設計における高度な熱工学への決定的なシフトを目の当たりにしており、エネルギー伝達効率を高めながらコア損失と迷走損失を最小限に抑えることを目指しています。スペースの制約とエネルギー負荷が激しい都市環境では、高度な水冷システムの必要性が変圧器技術を再構築しています。一方、リアルタイム監視、IoT対応センサー、予測診断の統合は、公益事業や産業部門全体のメンテナンス戦略を変革しています。事業者は、計画外停止を制限し、資産管理を改善するために、状態ベースのメンテナンスと早期故障検出を優先するようになってきています。このようなデジタル化、持続可能性、運用効率の強力な融合は、次世代水冷変圧器システムの広範な採用を推進し続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 139億米ドル |

| 予測金額 | 236億米ドル |

| CAGR | 5.2% |

クローズドコア変圧器は、その優れた負荷耐性とIoTベースの保守技術とのシームレスな統合により、製品ランドスケープを支配し、2034年までに95億米ドルを生み出すと予測されています。ベリーコアとシェルコアの設計も、そのコンパクトなプロファイルと効率の優位性で注目を集めており、再生可能エネルギー施設やスマートシティグリッドの進化するニーズに完全に合致しています。産業用アプリケーション・セグメントは2024年に50.1%の市場シェアを獲得し、CAGR 4.5%で成長しています。これは、過酷な運用負荷の下で堅牢で信頼性の高い電力供給を必要とする重工業、石油化学、大規模生産などの部門が牽引しています。データセンターや高層開発などの商業分野では、エネルギー効率と運用の継続性を確保すると同時に環境への影響を低減するため、よりスペースに最適化された水冷システムの採用が進んでいます。電力会社は、既存の送電網への再生可能エネルギーのシームレスな統合をサポートするため、改修プログラムやデジタルアップグレードへの投資を強化しています。

米国の水冷変圧器市場は2024年に21億米ドルを生み出し、積極的な送電網近代化の取り組み、再生可能エネルギープロジェクトの急増、エネルギー効率規制の強化に後押しされて、2034年には40億米ドルに達すると予測されています。しかし、貿易制限や材料関税が潜在的な課題となり、短期的には設備コストや納入スケジュールに影響を及ぼします。TBEA、CEEG、Neeltran、Control Transformer、RoMan Manufacturing、Crossmars Energy、Noratel、Sensata Technologies、Jackson Transformer Company、Baobian Electric、BEST Transformer、Automation International、GPD Transformers、ARCHIT ELECTRICALといった主要企業が市場革新を主導しています。戦略的イニシアチブは、自動化、モジュラー設計開発、地域サプライチェーンの最適化、IoT対応性能追跡を中心に展開され、世界のエネルギー情勢の急速な進化に対応する高性能変圧器ソリューションを提供する部門に力を与えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略的ダッシュボード

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:コア別、2021-2034

- 主要動向

- 閉鎖

- シェル

- ベリー

第6章 市場規模・予測:製品別、2021-2034

- 主要動向

- 配電用変圧器

- 電力変圧器

- その他

第7章 市場規模・予測:巻き取り式、2021-2034

- 主要動向

- 2巻き

- オートトランスフォーマー

第8章 市場規模・予測:電圧別、2021-2034

- 主要動向

- 中電圧

- 高電圧

第9章 市場規模・予測:断熱材別、2021-2034

- 主要動向

- ガス

- 油

- 固体

- その他

第10章 市場規模・予測:評価順、2021-2034

- 主要動向

- 10 MVA未満

- 10 MVA以上から100 MVA以下

- 100 MVA以上から600 MVA以下

- 600MVA以上

第11章 市場規模・予測:用途別、2021-2034

- 主要動向

- 商業用

- 産業

- ユーティリティ

第12章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- ロシア

- 英国

- イタリア

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- エジプト

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第13章 企業プロファイル

- ARCHIT ELECTRICAL

- Automation International

- Baobian Electric

- BEST Transformer

- CEEG

- Control Transformer

- Crossmars Energy

- GPD Transformers

- Jackson Transformer Company

- Neeltran

- Noratel

- RoMan Manufacturing

- Sensata Technologies

- TBEA

目次

The Global Water-Cooled Transformer Market was valued at USD 13.9 billion in 2024 and is projected to grow at a CAGR of 5.2% to reach USD 23.6 billion by 2034, fueled by surging energy demands, innovations in thermal management systems, and the urgent need for high-performance solutions in heavy-duty industrial and utility settings. As the global power infrastructure evolves, industries are pushing for technologies that ensure efficiency, reliability, and longevity. Water-cooled transformers are becoming the go-to choice for operations that require compact yet high-capacity power setups, especially where heat dissipation is critical. With increasing pressure to optimize energy use and minimize equipment downtime, companies are investing heavily in cooling solutions that deliver superior thermal management without compromising on footprint or scalability. The trend toward urbanization, smart city projects, and renewable energy integration further amplifies the demand for compact, modular substations where effective heat control and extended operational life are non-negotiable.

Today's industrial landscape is witnessing a decisive shift toward advanced thermal engineering in transformer design, aiming to minimize core and stray losses while boosting energy transfer efficiency. In urban environments where space constraints and energy loads are intense, the need for sophisticated water-cooled systems is reshaping transformer technology. Meanwhile, the integration of real-time monitoring, IoT-enabled sensors, and predictive diagnostics is transforming maintenance strategies across utilities and industrial sectors. Operators are increasingly prioritizing condition-based maintenance and early fault detection to limit unplanned outages and improve asset management. This strong convergence of digitalization, sustainability, and operational efficiency continues to drive the widespread adoption of next-generation water-cooled transformer systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.9 Billion |

| Forecast Value | $23.6 Billion |

| CAGR | 5.2% |

Closed core transformers dominate the product landscape and are projected to generate USD 9.5 billion by 2034, thanks to their superior load tolerance and seamless integration with IoT-based maintenance technologies. Berry and shell core designs are also capturing attention for their compact profiles and efficiency advantages, aligning perfectly with the evolving needs of renewable energy facilities and smart city grids. The industrial applications segment captured a 50.1% market share in 2024 and is growing at a 4.5% CAGR, driven by sectors such as heavy manufacturing, petrochemicals, and large-scale production that require rugged, reliable power delivery under extreme operational loads. Commercial segments, including data centers and high-rise developments, are adopting more space-optimized water-cooled systems to ensure energy efficiency and operational continuity while reducing their environmental impact. Utilities are intensifying investments in retrofit programs and digital upgrades to support the seamless integration of renewables into existing grids.

The U.S. water-cooled transformer market generated USD 2.1 billion in 2024 and is forecasted to reach USD 4 billion by 2034, propelled by aggressive grid modernization efforts, a surge in renewable energy projects, and tighter energy efficiency regulations. However, trade restrictions and material tariffs pose potential challenges, impacting equipment costs and delivery schedules in the short term. Key players such as TBEA, CEEG, Neeltran, Control Transformer, RoMan Manufacturing, Crossmars Energy, Noratel, Sensata Technologies, Jackson Transformer Company, Baobian Electric, BEST Transformer, Automation International, GPD Transformers, and ARCHIT ELECTRICAL are leading market innovation. Strategic initiatives revolve around automation, modular design development, regional supply chain optimization, and IoT-enabled performance tracking, empowering the sector to deliver high-performance transformer solutions that meet the rapidly evolving demands of the global energy landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Core, 2021 - 2034 (USD Million, ‘000 Units)

- 5.1 Key trends

- 5.2 Closed

- 5.3 Shell

- 5.4 Berry

Chapter 6 Market Size and Forecast, By Product, 2021 - 2034 (USD Million, ‘000 Units)

- 6.1 Key trends

- 6.2 Distribution transformer

- 6.3 Power transformer

- 6.4 Others

Chapter 7 Market Size and Forecast, By Winding, 2021 - 2034 (USD Million, ‘000 Units)

- 7.1 Key trends

- 7.2 Two winding

- 7.3 Auto transformer

Chapter 8 Market Size and Forecast, By Voltage, 2021 - 2034 (USD Million, ‘000 Units)

- 8.1 Key trends

- 8.2 Medium voltage

- 8.3 High voltage

Chapter 9 Market Size and Forecast, By Insulation, 2021 - 2034 (USD Million, ‘000 Units)

- 9.1 Key trends

- 9.2 Gas

- 9.3 Oil

- 9.4 Solid

- 9.5 Others

Chapter 10 Market Size and Forecast, By Rating, 2021 - 2034 (USD Million, ‘000 Units)

- 10.1 Key trends

- 10.2 ≤ 10 MVA

- 10.3 > 10 MVA to ≤ 100 MVA

- 10.4 > 100 MVA to ≤ 600 MVA

- 10.5 > 600 MVA

Chapter 11 Market Size and Forecast, By Application, 2021 - 2034 (USD Million, ‘000 Units)

- 11.1 Key trends

- 11.2 Commercial

- 11.3 Industrial

- 11.4 Utility

Chapter 12 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, ‘000 Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.2.3 Mexico

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 France

- 12.3.3 Russia

- 12.3.4 UK

- 12.3.5 Italy

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 Japan

- 12.4.3 South Korea

- 12.4.4 India

- 12.4.5 Australia

- 12.5 Middle East & Africa

- 12.5.1 Saudi Arabia

- 12.5.2 UAE

- 12.5.3 Qatar

- 12.5.4 Egypt

- 12.5.5 South Africa

- 12.6 Latin America

- 12.6.1 Brazil

- 12.6.2 Argentina

Chapter 13 Company Profiles

- 13.1 ARCHIT ELECTRICAL

- 13.2 Automation International

- 13.3 Baobian Electric

- 13.4 BEST Transformer

- 13.5 CEEG

- 13.6 Control Transformer

- 13.7 Crossmars Energy

- 13.8 GPD Transformers

- 13.9 Jackson Transformer Company

- 13.10 Neeltran

- 13.11 Noratel

- 13.12 RoMan Manufacturing

- 13.13 Sensata Technologies

- 13.14 TBEA

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日