|

|

市場調査レポート

商品コード

1740783

アルミナ精製の市場機会、成長促進要因、産業動向分析、予測、2025~2034年Alumina Refining Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| アルミナ精製の市場機会、成長促進要因、産業動向分析、予測、2025~2034年 |

|

出版日: 2025年04月23日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

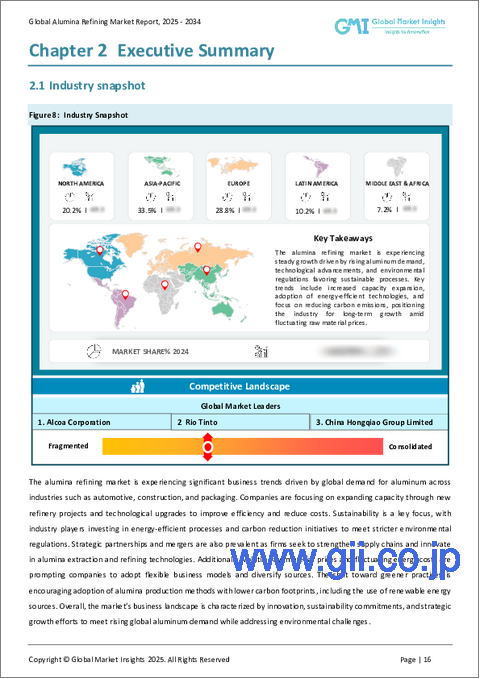

アルミナ精製の世界市場規模は、2024年に475億米ドルとなり、CAGR 3.5%で成長し、2034年には660億米ドルに達すると推定されます。

この成長は主に、アルミニウム生産において重要な前駆物質である一次アルミニウムの需要増加によるものです。自動車、航空宇宙、建設などの産業が拡大を続ける中、アルミニウムのニーズが急増しています。特に電気自動車(EV)分野では、燃費効率を促進する軽量材料の需要が高いです。低燃費の航空機やその他の輸送技術もアルミニウムに大きく依存しており、アルミニウム製錬に使用される主原料である製錬グレードアルミナ(SGA)の必要性を高めています。再生可能エネルギーと電気自動車へのシフトがアルミニウム需要を加速し、その結果、アルミナ精製も加速しています。

技術の進歩も、アルミナ精製市場に拍車をかける重要な要因のひとつです。エネルギー効率の高いキルン、バイエル製法の改善、再生可能エネルギー源の統合などの革新はすべて、より持続可能でコスト効率の高いアルミナ生産に貢献しています。これらの技術開発により、企業は操業コストを削減し、環境規制を遵守し、全体的な生産性を高めることができます。環境基準が厳しくなるにつれ、企業は競争力を維持するため、こうした最先端技術の採用を増やしています。これにより、環境への影響を最小限に抑えながら、アルミニウムの世界の需要の増加に対応することができます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 475億米ドル |

| 予測金額 | 660億米ドル |

| CAGR | 3.5% |

アルミナ精製では、バイエル製法が依然として主流であり、世界市場の93.9%という驚異的なシェアを占めています。この方法が広く使われているのは、特に高級ボーキサイトからアルミナを抽出する効率が高いためです。この方法は、廃棄物を最小限に抑えながら安定した高品質のアルミナを生産するため、大規模な操業に最適です。さらに、バイエル製法は、省エネルギー機器や高度な排ガス規制などの技術的アップグレードに適しているため、企業は大規模なインフラ改修を必要とせずに操業を近代化することができます。

市場はアルミナ品位によってさらに細分化され、製錬所グレードアルミナ(SGA)が87.7%と大きなシェアを占めています。このグレードはアルミニウム製錬に不可欠で、輸送、建設、包装、電子機器など、さまざまな産業で最も一般的に使用されています。特に自動車や航空宇宙分野で軽量素材の需要が高まるにつれ、SGAの需要は引き続き高いです。特に自動車産業は、部品にアルミニウムを使用する低燃費車や電気自動車のニーズが高まる中、この成長の大きな原動力となっています。

米国のアルミナ精製市場は、2024年には世界市場の17.8%を占め、23億米ドルを生み出します。この成長の主な要因は、米国政府がアルミニウムの国内生産を強化し、輸入への依存を減らすことを推進していることです。国内サプライチェーンの強化と国内精製能力の拡大を目指した政策が、市場の拡大を加速させています。自動車、航空宇宙、再生可能エネルギーなどの分野におけるアルミニウム需要の増加が、米国のアルミナ精製産業の成長をさらに後押ししています。産業需要と政府政策の両方が今後数年間の市場開拓をさらに促進するため、この動向は続くと予想されます。

世界のアルミナ精製業界の主要企業には、Rio Tinto、Aluminum Corporation of China(CHALCO)、RUSAL、Norsk Hydro ASA、Alcoa Corporationなどがあります。これらの企業は、技術の進歩や現地生産の強化に投資することで、世界の存在感を強めています。また、主要部門におけるアルミニウム需要の増加に対応するため、精製プロセスにも戦略的に投資しています。これらの企業の先見的な戦略により、アルミニウムとその合金のニーズの高まりに対応しながら、急速に成長する市場で競争力を維持することができます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 一次アルミニウムの世界の需要の増加

- 新興経済における急速な工業化

- 自動車および航空宇宙部門の拡大

- 電子機器と半導体の消費量の増加

- 高純度アルミナ(HPA)の需要増加

- 精製プロセスにおける技術的進歩

- 業界の潜在的リスク&課題

- 高いエネルギー強度とそれに伴うコスト

- 赤泥処分に関する環境規制

- ボーキサイトの供給と価格の変動

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

注:上記の貿易統計は主要国についてのみ提供されます

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推定・予測:精製プロセス別、2021-2034年

- 主要動向

- バイエル法

- バイエル焼結法

- その他の代替プロセス

第6章 市場推定・予測:グレード別、2021-2034年

- 主要動向

- 製錬グレードアルミナ(SGA)

- 化学グレードアルミナ(CGA)

- 触媒グレードアルミナ

- 研磨グレードアルミナ

- 耐火グレードアルミナ

- 高純度アルミナ(HPA)

第7章 市場推定・予測:アプリケーション別、2021-2034年

- 主要動向

- 一次アルミニウム生産

- セラミックス・耐火物

- 触媒・吸着剤

- ガラス製造

- 研磨剤

- その他

第8章 市場推定・予測:地域別、2021-2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Alcoa Corporation

- Rio Tinto

- RUSAL(United Company RUSAL Plc)

- Norsk Hydro ASA

- South32 Limited

- China Hongqiao Group Limited

- Alba(Aluminium Bahrain B.S.C.)

- Emirates Global Aluminium(EGA)

- Vedanta Limited

- East Hope Group

The Global Alumina Refining Market was valued at USD 47.5 billion in 2024 and is estimated to grow at a CAGR of 3.5% to reach USD 66 billion by 2034. This growth is primarily driven by the increasing demand for primary aluminum, which is a critical precursor in aluminum production. As industries like automotive, aerospace, and construction continue to expand, the need for aluminum has surged. Particularly in the electric vehicle (EV) sector, lightweight materials that promote fuel efficiency are in high demand. Fuel-efficient aircraft and other transportation technologies also heavily rely on aluminum, driving the need for smelter-grade alumina (SGA), the main feedstock used in aluminum smelting. The shift toward renewable energy and electric vehicles is accelerating the demand for aluminum and, consequently, alumina refining.

Technological advancements are another key factor fueling the alumina refining market. Innovations like energy-efficient kilns, improvements in the Bayer process, and the integration of renewable energy sources are all contributing to more sustainable and cost-effective alumina production. These technological developments allow companies to reduce operational costs, comply with environmental regulations, and boost overall productivity. With environmental standards becoming more stringent, companies are increasingly adopting these cutting-edge technologies to remain competitive. This positions them to capitalize on the growing global demand for aluminum while minimizing environmental impact.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $47.5 Billion |

| Forecast Value | $66 Billion |

| CAGR | 3.5% |

The Bayer process remains the dominant method in alumina refining, commanding an impressive 93.9% share of the global market. Its widespread use is due to its efficiency, particularly for extracting alumina from premium-grade bauxite. This method is perfect for large-scale operations as it produces consistent, high-quality alumina with minimal waste. Moreover, the Bayer process aligns well with technological upgrades, such as energy-saving equipment and advanced emission controls, allowing companies to modernize their operations without needing significant infrastructure overhauls.

The market is further segmented by alumina grade, with smelter-grade alumina (SGA) taking the lion's share at 87.7%. This grade is essential for aluminum smelting and is the most commonly used type across various industries, including transportation, construction, packaging, and electronics. As the demand for lightweight materials grows, especially in the automotive and aerospace sectors, SGA continues to be in high demand. The automotive industry, in particular, is a significant driver of this growth as the need for fuel-efficient and electric vehicles, which rely on aluminum for their components, escalates.

The U.S. alumina refining market accounted for 17.8% of the global market in 2024, generating USD 2.3 billion. A major contributor to this growth is the U.S. government's push for boosting domestic aluminum production and reducing dependence on imports. Policies aimed at strengthening local supply chains and expanding domestic refining capabilities have accelerated the market's expansion. Rising demand for aluminum in sectors such as automotive, aerospace, and renewable energy has further supported the growth of the U.S. alumina refining industry. This trend is expected to continue as both industrial demand and governmental policies fuel further market development in the coming years.

Major players in the Global Alumina Refining Industry include Rio Tinto, Aluminum Corporation of China (CHALCO), RUSAL, Norsk Hydro ASA, and Alcoa Corporation. These companies are strengthening their global presence by investing in technological advancements and local production enhancements. They are also strategically investing in refining processes to meet the rising demand for aluminum in key sectors. Their forward-thinking strategies enable them to remain competitive in a rapidly growing market while addressing the rising need for aluminum and its alloys across industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1.1 Rising global demand for primary aluminum

- 3.6.1.2 Rapid industrialization in emerging economies

- 3.6.1.3 Expansion of automotive and aerospace sectors

- 3.6.1.4 Growing consumption of electronics and semiconductors

- 3.6.1.5 Increase in demand for high-purity alumina (HPA)

- 3.6.1.6 Technological advancements in refining processes

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High energy intensity and associated costs

- 3.6.2.2 Environmental regulations on red mud disposal

- 3.6.2.3 Volatility in bauxite supply and pricing

- 3.7 Trump administration tariffs

- 3.7.1 Impact on trade

- 3.7.1.1 Trade volume disruptions

- 3.7.1.2 Retaliatory measures

- 3.7.2 Impact on the industry

- 3.7.2.1 Supply-side impact (raw materials)

- 3.7.2.1.1 Price volatility in key materials

- 3.7.2.1.2 Supply chain restructuring

- 3.7.2.1.3 Production cost implications

- 3.7.2.2 Demand-side impact (selling price)

- 3.7.2.2.1 Price transmission to end markets

- 3.7.2.2.2 Market share dynamics

- 3.7.2.2.3 Consumer response patterns

- 3.7.2.1 Supply-side impact (raw materials)

- 3.7.3 Key companies impacted

- 3.7.4 Strategic industry responses

- 3.7.4.1 Supply chain reconfiguration

- 3.7.4.2 Pricing and product strategies

- 3.7.4.3 Policy engagement

- 3.7.5 Outlook and future considerations

- 3.7.1 Impact on trade

- 3.8 Trade statistics (HS code)

- 3.8.1 Major exporting countries

- 3.8.1.1 Country 1

- 3.8.1.2 Country 2

- 3.8.1.3 Country 3

- 3.8.2 Major importing countries

- 3.8.2.1 Country 1

- 3.8.2.2 Country 2

- 3.8.2.3 Country 3

- 3.8.1 Major exporting countries

Note: the above trade statistics will be provided for key countries only.

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Refining Process Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Bayer process

- 5.3 Combined bayer-sinter process

- 5.4 Other alternative processes

Chapter 6 Market Estimates and Forecast, By Grade, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Smelter grade alumina (SGA)

- 6.3 Chemical grade alumina (CGA)

- 6.4 Catalyst-grade alumina

- 6.5 Abrasive-grade alumina

- 6.6 Refractory-grade alumina

- 6.7 High-purity alumina (HPA)

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Primary aluminum production

- 7.3 Ceramics & refractories

- 7.4 Catalysts & adsorbents

- 7.5 Glass manufacturing

- 7.6 Abrasives

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alcoa Corporation

- 9.2 Rio Tinto

- 9.3 RUSAL (United Company RUSAL Plc)

- 9.4 Norsk Hydro ASA

- 9.5 South32 Limited

- 9.6 China Hongqiao Group Limited

- 9.7 Alba (Aluminium Bahrain B.S.C.)

- 9.8 Emirates Global Aluminium (EGA)

- 9.9 Vedanta Limited

- 9.10 East Hope Group