|

市場調査レポート

商品コード

1740770

脱毛用化粧品原料の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Cosmetic Ingredients for Hair Removal Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 脱毛用化粧品原料の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月25日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

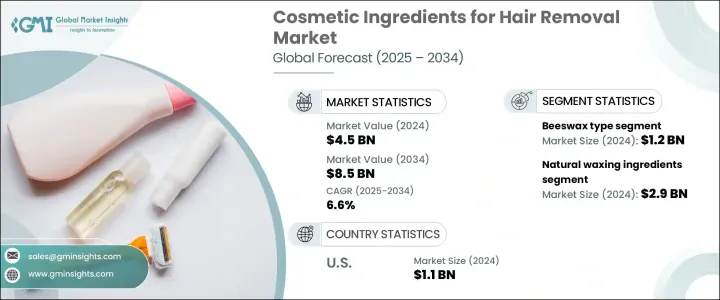

脱毛用化粧品原料の世界市場は、2024年には45億米ドルと評価され、CAGR 6.6%で成長し、2034年には85億米ドルに達すると推定されています。

この成長は、パーソナルグルーミングとウェルネスへの関心の高まり、特に消費者がスキンケア習慣を重視するようになったことが主な要因です。過去10年間、除毛製品に使用される化粧品成分の配合と技術革新の両方において、顕著な進歩が見られました。クリーム、ジェル、ワックス、フォームのいずれにおいても、肌に優しく効果的な除毛を実現する成分への需要が急増しています。特に、より清潔で、より安全で、より持続可能な選択肢を好む消費者の期待に応えるべく、各メーカーは一貫して処方を開発しています。

自然で環境に配慮した製品への消費者行動のシフトが、この市場を大きく形成しています。購入者はますます合成化学物質を避け、天然由来の成分を好むようになっています。このような嗜好は、製品の内容だけでなく、透明性、倫理的調達、環境安全性といった価値観にまで及んでいます。そのため、化粧品ブランドは現在、クリーンラベルの製品に重点を置き、製品の純度と規制遵守を強調しています。人工的な添加物や刺激の強い防腐剤を含まない製品の魅力が、性能に妥協しないケミカルフリーの脱毛ソリューションに対する需要の高まりに寄与しています。この進化は、成分の透明性と製品の安全性が優先されるパーソナルケア分野の広範な動向と密接に一致しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 45億米ドル |

| 予測金額 | 85億米ドル |

| CAGR | 6.6% |

様々な成分タイプの中で、蜜蝋ベースの製剤が大きな牽引力を示しています。2024年、蜜蝋ベースの化粧品用脱毛成分市場は12億米ドルと推定され、2025年から2034年までの予測期間中にCAGR 6.9%で成長すると予測されます。蜜蝋は、その天然由来、良好な皮膚特性、塗布の容易さにより、依然として好まれる成分です。蜜蝋は、布片を必要としないハードワックス製剤に広く使用されており、家庭用ユーザーにも専門家にも適しています。半固形のため、直接塗ることができ、特に敏感な部分には使いやすいです。

天然ワックス成分で作られた脱毛製品への嗜好が高まっています。2024年、天然ワックス成分セグメントは29億米ドルと評価され、2034年までCAGR 6.9%で成長し、65.4%の市場シェアを確保すると予測されています。消費者は、その安全性、最小限の副作用、敏感肌への適合性から、これらの代替品に目を向けています。ホリスティックなセルフケアの需要が高まるにつれて、ウェルネスを重視するライフスタイルに沿った天然由来の素材で作られた製品への関心も高まっています。オーガニック、持続可能、防腐剤フリーの処方を求める動きは、製品開発と購買決定の大きな原動力となっています。クリーンラベリング、オーガニック認証、環境に関する主張は、ブランドが市場でどのような位置づけをするかにおいて重要な役割を果たしています。

米国では、脱毛用化粧品原料市場は2024年に11億米ドルに達し、2025年から2034年までのCAGRは6.9%と予測されています。この地域の成長の原動力となっているのは、個人のウェルネスと衛生に対する消費者の意識の顕著な変化です。米国人は、活動的なライフスタイルやセルフケアに対する意識の高まりに沿った、より効果的で肌に優しい脱毛ソリューションを求めています。この需要は、成分調達と製剤プロセスにおける革新を促し、安全性と有効性の二重のニーズを満たすソリューションを提供することをブランドに促しています。

世界の競合情勢は、バリューチェーンに大きな影響力を持つ企業群を特徴としています。主要参入企業は、成分の完全性と持続可能性への高まる期待に応えるため、研究開発、製品の差別化に力を注いでいます。このセグメントで価格競争が繰り広げられることは比較的珍しいが、技術革新と規制への対応に重点を置くことが競争戦略の要となっています。主要企業は環境認証に投資し、提携や買収を通じて調達能力を拡大しています。ブランドの評判、高品質の原料へのアクセス、B2B処方への要求に応える能力は、市場での存在感を維持するための中心的な要素です。

デジタル化が進むにつれ、ブランドはターゲットを絞ったマーケティングと技術サポートに傾注し、B2Bとの関係を構築してリーチを拡大しています。透明性、安全性、持続的な効果を求める消費者の要望は市場を押し進め続けており、製品の謳い文句が信頼に足る魅力的なものであることを保証するために、製剤技術や臨床試験への継続的な投資を促しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 供給側の影響(原材料)

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国、2021-2024

- 主要輸入国、2021-2024

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 世界の規制枠組みの概要

- FDA規制

- EUの化粧品規制

- 中国の化粧品監督管理局(CSAR)

- 影響要因

- 促進要因

- 家庭用脱毛製品に対する消費者の需要の高まり

- 天然およびオーガニック化粧品原料への嗜好の高まり

- 新興国におけるパーソナルケア市場の拡大

- より安全で肌に優しい処方に対する規制支援

- 業界の潜在的リスク&課題

- 化学成分の使用に関する厳しい規制

- 脱毛剤に関連する皮膚の敏感性とアレルギーの懸念

- 促進要因

- 市場機会

- 天然およびオーガニック処方の開発

- eコマースチャネルの拡大

- 新興経済諸国の未開拓市場

- 臭気中和技術の革新

- 多機能脱毛製品

- 市場参入と拡大戦略

- 市場参入障壁と課題

- 規制上のハードルとコンプライアンスコスト

- 知的財産の制約

- 確立された企業の優位性

- 技術的専門知識の要件

- 市場参入戦略

- 合弁事業と戦略的提携

- ライセンシングと技術移転

- 買収とブラウンフィールドへの参入

- グリーンフィールド投資と有機的成長

- 地理的拡大の機会

- 高成長地域市場

- 未開拓市場の潜在的評価

- 文化的および規制上の考慮事項

- ローカリゼーションと適応戦略

- 製品ポートフォリオ拡大戦略

- ライン拡張と製品バリエーション

- カテゴリー間の拡張

- プレミアムおよびバリューセグメントのターゲティング

- カスタマイズとパーソナライゼーションのアプローチ

- 市場参入障壁と課題

- リスク評価と軽減戦略

- 市場リスク

- 需要の変動性と循環性

- 競争の激化と価格圧力

- 代替製品と技術

- 消費者の嗜好の変化

- 運用リスク

- サプライチェーンの混乱

- 品質管理と製品安全

- 製造と配合の課題

- 人材管理と人材管理

- 規制およびコンプライアンスリスク

- 規制状況の変化

- 違反に対する罰金とリコール

- 原材料の制限と禁止

- ラベル表示とマーケティングクレームのリスク

- 市場リスク

- 将来の見通しと市場予測

- 短期市場見通し(1~2年)

- すぐに成長機会

- 短期的な課題

- 競合情勢の進化

- 中期市場見通し(3~5年)

- 新興市場セグメント

- テクノロジー採用曲線

- 需給バランス予測

- 長期市場見通し(5~10年)

- 破壊的技術とイノベーション

- 持続可能性主導の市場変革

- 消費者行動の進化

- 業界の統合と再編のシナリオ

- シナリオ分析と緊急時対応計画

- 最良の成長シナリオ

- ベースケース市場の進化

- 最悪の市場縮小

- 破壊的シナリオ分析

- 短期市場見通し(1~2年)

- 投資機会と戦略的提言

- 投資魅力度評価

- 高成長市場セグメント

- テクノロジー投資機会

- 地理的投資ホットスポット

- M&Aとパートナーシップの機会

- 原料メーカー向けの戦略的提言

- 製品開発とイノベーションの重点分野

- 市場ポジショニングと差別化戦略

- 持続可能性とコンプライアンスのロードマップ

- パートナーシップとコラボレーションの機会

- 最終製品メーカー向けの戦略的推奨事項

- 処方と製品開発の優先順位

- 消費者エンゲージメントとマーケティング戦略

- 流通とチャネルの最適化

- 持続可能性とブランドポジショニング

- 投資家および金融利害関係者への戦略的提言

- 潜在性の高い投資対象

- リスク評価と軽減アプローチ

- ポートフォリオ分散戦略

- 出口戦略の検討

- 投資魅力度評価

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- ロジン酸グリセリル(ロジン)/ガムロジン

- 水素化ロジン

- ビーズワックス

- エッセンシャルオイル

- チオグリコール酸

- ラノリン

- グリセリン

- その他

第6章 市場推計・予測:カテゴリー別、2021-2034

- 主要動向

- 天然ワックス成分

- 合成ワックス成分

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- ソフトワックス

- ハードワックス

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Aadra International

- Arjun Bees Wax Industries

- Ataman Chemical

- BRM Chemicals

- DKSH Holding Ltd.

- Making Cosmetics Inc.

- Guangzhou ECOPOWER

- Gustav Heess Oleochemische Erzeugnisse GmbH

- JKB Infotech PVT LTD

- Koster Keunen

- Koster Keunen LLC

- Knowde

- Mishra Chemical Works

- Rimpro-india

- SpecialChem Arkema Global

- SOPHIM IBERIA S.L

- Strahl and Pitsch

- Synthomer

- Unicorn petroleum industries pvt. Ltd

- Zoic Cosmetics

The Global Cosmetic Ingredients for Hair Removal Market was valued at USD 4.5 billion in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 8.5 billion by 2034. This growth is largely driven by increased interest in personal grooming and wellness practices, particularly as consumers place greater importance on their skincare routines. Over the past decade, there has been notable progress in both the formulation and innovation of cosmetic ingredients used in hair removal products. Whether in creams, gels, waxes, or foams, the demand for ingredients that deliver effective hair removal while being gentle on the skin has surged. Manufacturers are consistently developing formulations that meet evolving consumer expectations, especially those preferring cleaner, safer, and more sustainable options.

The shift in consumer behavior toward natural and eco-conscious products has significantly shaped this market. Buyers are increasingly avoiding synthetic chemicals, showing a clear preference for ingredients derived from natural sources. This preference is not just about product content but extends to values like transparency, ethical sourcing, and environmental safety. As such, cosmetic brands are now focusing heavily on clean-label offerings and emphasizing product purity and regulatory compliance. The appeal of products free from artificial additives or harsh preservatives is contributing to a rise in demand for chemical-free hair removal solutions that do not compromise on performance. This evolution aligns closely with broader trends in the personal care sector, where ingredient transparency and product safety are prioritized.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.5 Billion |

| Forecast Value | $8.5 Billion |

| CAGR | 6.6% |

Among the various ingredient types, beeswax-based formulations have shown significant traction. In 2024, the market for beeswax-based cosmetic hair removal ingredients was estimated at USD 1.2 billion and is anticipated to grow at a CAGR of 6.9% during the forecast period from 2025 to 2034. Beeswax remains a preferred ingredient due to its natural origin, favorable skin properties, and ease of application. It is widely used in hard wax formulations that eliminate the need for cloth strips, making it suitable for at-home users and professionals alike. Its semi-solid consistency allows for direct application, which makes it user-friendly, especially for sensitive areas.

There is a growing preference for hair removal products made with natural waxing components. In 2024, the natural waxing ingredients segment was valued at USD 2.9 billion and is projected to grow at a CAGR of 6.9% through 2034, securing a market share of 65.4%. Consumers are turning to these alternatives due to their perceived safety, minimal side effects, and compatibility with sensitive skin. As the demand for holistic self-care rises, so does interest in products crafted from naturally derived materials that align with wellness-focused lifestyles. The push for organic, sustainable, and preservative-free formulations has become a major driving force behind product development and purchasing decisions. Clean labeling, organic certifications, and environmental claims are playing an essential role in how brands position themselves in the market.

In the United States, the cosmetic ingredients for hair removal market reached USD 1.1 billion in 2024, with projections suggesting a 6.9% CAGR from 2025 to 2034. This regional growth is fueled by a noticeable change in consumer attitudes toward personal wellness and hygiene. Americans are seeking more effective, skin-friendly solutions for hair removal that align with their active lifestyles and heightened awareness around self-care. This demand is fostering innovation in ingredient sourcing and formulation processes, encouraging brands to deliver solutions that meet the dual need for safety and efficacy.

The global landscape features a competitive group of companies that hold significant influence over the value chain. Major participants have centered their efforts around research, development, and product differentiation to meet rising expectations for ingredient integrity and sustainability. While pricing battles are relatively uncommon in this segment, the emphasis on innovation and regulatory readiness has become a cornerstone of competitive strategy. Leading companies are investing in eco-certifications and expanding their sourcing capabilities through partnerships and acquisitions. Brand reputation, access to high-quality raw materials, and the ability to meet B2B formulation demands are central to sustaining a strong market presence.

As digital engagement grows, brands are leaning on targeted marketing and technical support to build B2B relationships and expand reach. Consumer demand for transparency, safety, and long-lasting effectiveness continues to push the market forward, prompting ongoing investment in formulation technology and clinical testing to ensure product claims are both credible and appealing.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Demand-side impact (selling price)

- 3.2.3.1 Price transmission to end markets

- 3.2.3.2 Market share dynamics

- 3.2.3.3 Consumer response patterns

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries, 2021-2024 (Kilo Tons)

- 3.3.2 Major importing countries, 2021-2024 (Kilo Tons)

- 3.4 Supplier landscape

- 3.5 Profit margin analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.7.1 Global regulatory framework overview

- 3.7.2 Fda regulations

- 3.7.3 Eu cosmetics regulation

- 3.7.4 China's csar (cosmetic supervision and administration regulation)

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising consumer demand for at-home hair removal products

- 3.8.1.2 Increasing preference for natural and organic cosmetic ingredients

- 3.8.1.3 Expanding personal care markets in emerging economies

- 3.8.1.4 Regulatory support for safer, skin-friendly formulations

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Stringent regulations around chemical ingredient usage

- 3.8.2.2 Skin sensitivity and allergy concerns related to active depilatory agents

- 3.8.1 Growth drivers

- 3.9 Market opportunities

- 3.9.1 Development of natural and organic formulations

- 3.9.2 Expanding e-commerce channels

- 3.9.3 Untapped markets in developing economies

- 3.9.4 Innovation in odor-neutralizing technologies

- 3.9.5 Multi-functional hair removal products

- 3.10 Market entry and expansion strategies

- 3.10.1 Market entry barriers and challenges

- 3.10.1.1 Regulatory hurdles and compliance costs

- 3.10.1.2 Intellectual property constraints

- 3.10.1.3 Established player dominance

- 3.10.1.4 Technical expertise requirements

- 3.10.2 Market entry strategies

- 3.10.2.1 Joint ventures and strategic alliances

- 3.10.2.2 Licensing and technology transfer

- 3.10.2.3 Acquisition and brownfield entry

- 3.10.2.4 Greenfield investment and organic growth

- 3.10.3 Geographic expansion opportunities

- 3.10.3.1 High-growth regional markets

- 3.10.3.2 Untapped market potential assessment

- 3.10.3.3 Cultural and regulatory considerations

- 3.10.3.4 Localization and adaptation strategies

- 3.10.4 Product portfolio expansion strategies

- 3.10.4.1 Line extensions and product variants

- 3.10.4.2 Cross-category expansion

- 3.10.4.3 Premium and value segment targeting

- 3.10.4.4 Customization and personalization approaches

- 3.10.1 Market entry barriers and challenges

- 3.11 Risk assessment and mitigation strategies

- 3.11.1 Market risks

- 3.11.1.1 Demand volatility and cyclicality

- 3.11.1.2 Competitive intensity and price pressure

- 3.11.1.3 Substitute products and technologies

- 3.11.1.4 Consumer preference shifts

- 3.11.2 Operational risks

- 3.11.2.1 Supply chain disruptions

- 3.11.2.2 Quality control and product safety

- 3.11.2.3 Manufacturing and formulation challenges

- 3.11.2.4 Workforce and talent management

- 3.11.3 Regulatory and compliance risks

- 3.11.3.1 Changing regulatory landscape

- 3.11.3.2 Non-compliance penalties and recalls

- 3.11.3.3 Ingredient restrictions and bans

- 3.11.3.4 Labeling and marketing claim risks

- 3.11.1 Market risks

- 3.12 Future outlook and market projections

- 3.12.1 Short-term market outlook (1-2 years)

- 3.12.1.1 Immediate growth opportunities

- 3.12.1.2 Near-term challenges

- 3.12.1.3 Competitive landscape evolution

- 3.12.2 Medium-term market outlook (3-5 years)

- 3.12.2.1 Emerging market segments

- 3.12.2.2 Technology adoption curves

- 3.12.2.3 Supply-demand balance projections

- 3.12.3 Long-term market outlook (5-10 years)

- 3.12.3.1 Disruptive technologies and innovations

- 3.12.3.2 Sustainability-driven market transformation

- 3.12.3.3 Consumer behavior evolution

- 3.12.3.4 Industry consolidation and restructuring scenarios

- 3.12.4 Scenario analysis and contingency planning

- 3.12.4.1 Best-case growth scenario

- 3.12.4.2 Base-case market evolution

- 3.12.4.3 Worst-case market contraction

- 3.12.4.4 Disruptive scenario analysis

- 3.12.1 Short-term market outlook (1-2 years)

- 3.13 Investment opportunities and strategic recommendations

- 3.13.1 Investment attractiveness assessment

- 3.13.1.1 High-growth market segments

- 3.13.1.2 Technology investment opportunities

- 3.13.1.3 Geographic investment hotspots

- 3.13.1.4 M&a and partnership opportunities

- 3.13.2 Strategic recommendations for ingredient manufacturers

- 3.13.2.1 Product development and innovation focus areas

- 3.13.2.2 Market positioning and differentiation strategies

- 3.13.2.3 Sustainability and compliance roadmap

- 3.13.2.4 Partnership and collaboration opportunities

- 3.13.2.5 Strategic recommendations for end-product manufacturers

- 3.13.2.6 Formulation and product development priorities

- 3.13.2.7 Consumer engagement and marketing strategies

- 3.13.2.8 Distribution and channel optimization

- 3.13.2.9 Sustainability and brand positioning

- 3.13.3 Strategic recommendations for investors and financial stakeholders

- 3.13.3.1 High-potential investment targets

- 3.13.3.2 Risk assessment and mitigation approaches

- 3.13.3.3 Portfolio diversification strategies

- 3.13.3.4 Exit strategy considerations

- 3.13.1 Investment attractiveness assessment

- 3.14 Growth potential analysis

- 3.15 Porter’s analysis

- 3.16 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Glyceryl rosinate (rosin)/gum rosin

- 5.3 Hydrogenated rosin

- 5.4 Beeswax

- 5.5 Essential oils

- 5.6 Thioglycolic acid

- 5.7 Lanolin

- 5.8 Glycerin

- 5.9 Others

Chapter 6 Market Estimates & Forecast, By Category, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Natural waxing ingredients

- 6.3 Synthetic waxing ingredients

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Soft wax

- 7.3 Hard wax

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Aadra International

- 9.2 Arjun Bees Wax Industries

- 9.3 Ataman Chemical

- 9.4 BRM Chemicals

- 9.5 DKSH Holding Ltd.

- 9.6 Making Cosmetics Inc.

- 9.7 Guangzhou ECOPOWER

- 9.8 Gustav Heess Oleochemische Erzeugnisse GmbH

- 9.9 JKB Infotech PVT LTD

- 9.10 Koster Keunen

- 9.11 Koster Keunen LLC

- 9.12 Knowde

- 9.13 Mishra Chemical Works

- 9.14 Rimpro-india

- 9.15 SpecialChem Arkema Global

- 9.16 SOPHIM IBERIA S.L

- 9.17 Strahl and Pitsch

- 9.18 Synthomer

- 9.19 Unicorn petroleum industries pvt. Ltd

- 9.20 Zoic Cosmetics