|

市場調査レポート

商品コード

1982351

アスコルビルパルミテートの市場機会、成長要因、業界動向分析、および2026年~2035年の予測Ascorbyl Palmitate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| アスコルビルパルミテートの市場機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年02月26日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

概要

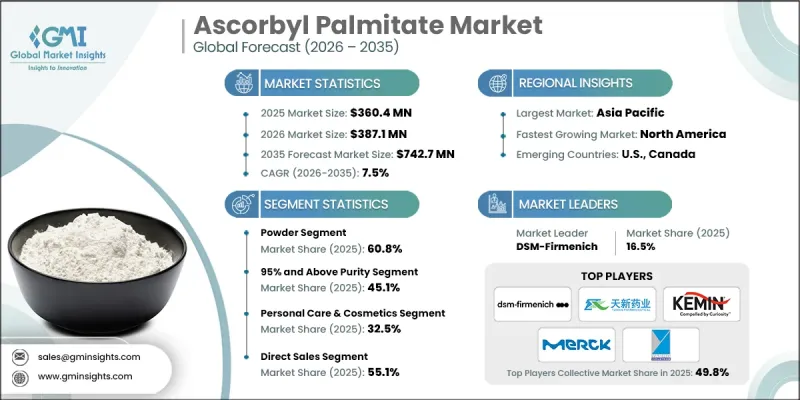

世界のアスコルビルパルミテート市場は、2025年に3億6,040万米ドルと評価され、CAGR 7.5%で成長し、2035年までに7億4,270万米ドルに達すると推定されています。

食品、化粧品、医薬品メーカーが製品の安定性を高め、保存期間を延長するために抗酸化成分の使用を拡大していることから、市場の成長は堅調に推移しています。ビタミンCの脂溶性誘導体であるパルミチン酸アスコルビルは、保管や流通の過程で製品の品質を維持しつつ、酸化による劣化から製剤を保護する上で重要な役割を果たしています。その多機能な抗酸化特性により、スキンケア製品、栄養補助食品、加工食品への用途に適しています。パーソナルケア製品においては、肌の美しさを高め、エイジングケアに役立つ効果をもたらし、食品分野では、油脂の劣化を防ぐ役割を果たします。予防医療やウェルネスに対する消費者の意識の高まりが、抗酸化成分を豊富に含む製品への需要をさらに後押ししています。天然由来や植物由来の化粧品原料への関心の高まりも、その普及を後押ししています。さらに、製剤技術の進歩や、ニュートラシューティカル(機能性食品)および機能性製品カテゴリーへの用途拡大により、世界中のメーカーにとって新たなビジネスチャンスが生まれています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026-2035 |

| 開始時の市場規模 | 3億6,040万米ドル |

| 予測額 | 7億4,270万米ドル |

| CAGR | 7.5% |

2025年には粉末セグメントが60.8%のシェアを占め、2035年までCAGR7.4%で成長すると予測されています。粉末アスコルビルパルミテートは、その優れた安定性、扱いやすさ、および長期保存性により、依然として好まれる形態です。化粧品、ニュートラシューティカル、食品の各製造プロセスにおける高い適合性により、正確な投与量管理と一貫した抗酸化保護が可能となります。スキンケアやサプリメントの配合において、信頼性が高く安定した抗酸化システムの需要が継続することで、このセグメントの持続的な成長が支えられると見込まれます。

純度95%以上のカテゴリーは、2025年に45.1%のシェアを占め、2026年から2035年にかけてCAGR 7.6%で成長すると予測されています。成分の品質が有効性、安全性、および規制順守に直接影響を与えるプレミアム化粧品や医薬品を製造するメーカーの間で、高純度グレードへの需要が高まっています。高度なスキンケア用途、ニュートラシューティカル製剤、および治療用製剤において最適な性能を発揮するためには、高い純度基準が不可欠です。規制当局の監視や消費者の期待が高まり続ける中、より高品質な原料への需要は引き続き堅調であると予想されます。

北米のアスコルビルパルミテート市場は2025年に28.2%のシェアを占め、急速に発展している地域産業としての地位を反映しています。スキンケア製品、パーソナルケア製剤、および栄養補助食品の堅調な消費が、引き続き需要を牽引しています。厳格な規制枠組みに加え、製品の安全性と性能に対する消費者の意識の高まりが、信頼性の高い抗酸化成分へのニーズを強めています。また、製剤の有効性と市場競争力の向上を目指す化粧品およびサプリメントメーカーによる継続的な製品イノベーションが、地域的な市場拡大をさらに後押ししています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 価格動向

- 地域別

- タイプ別

- 今後の市場動向

- 技術・イノベーションの動向

- 現在の技術動向

- 新興技術

- 特許動向

- 貿易統計(HSコード)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境配慮型イニシアチブ

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:形態別、2022-2035

- 粉末

- 液体

第6章 市場推計・予測:純度別、2022-2035

- 純度95%以上

- 純度90~95%

- 純度90%未満

第7章 市場推計・予測:用途別、2022-2035

- パーソナルケア・化粧品

- 食品・飲料

- 栄養補助食品

- 医薬品

- 飼料・動物栄養

- その他(産業用途)

第8章 市場推計・予測:流通チャネル別、2022-2035

- 直接販売

- 卸売業者・商社

- オンライン/eコマースプラットフォーム

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- dsm-firmenich

- Huizhou Comvikin Biotechnology Co., Ltd.

- Jiangxi Tianxin Pharmaceutical Co., Ltd.

- Kemin Industries

- Macsen Labs

- Merck KGaA

- Shandong Yifan Chemical Technology Co., Ltd.

- SURYA LIFE SCIENCES LTD.

- Tartaros Gonzalo Castello S.L.

- Yasho Industries