|

市場調査レポート

商品コード

1740766

車載用ワイヤレスモジュールの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Automotive Wireless Module Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 車載用ワイヤレスモジュールの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月21日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

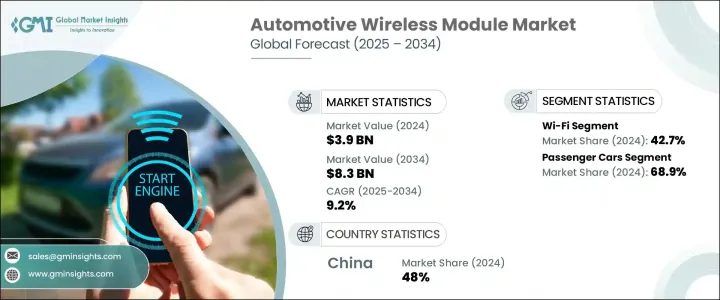

車載用ワイヤレスモジュールの世界市場規模は、2024年に39億米ドルとなり、コネクテッドカーに対する消費者需要の増加と、5GやV2X通信などの次世代ワイヤレス技術の急速な展開により、CAGR 9.2%で成長し、2034年には83億米ドルに達すると推定されます。

自動車産業がデジタルトランスフォーメーションへと大きくシフトする中、無線モジュールはよりスマートで安全、そしてよりコネクテッドなドライビング体験を提供する上で不可欠なコンポーネントとなりつつあります。シームレスなインフォテインメントシステムの実現から、予知保全や遠隔診断のサポートまで、これらのモジュールは自動車が環境やユーザーとどのように相互作用するかを再構築しています。

自動車メーカーは、利便性、安全性、性能を高めるために、ワイヤレス接続機能を倍増させています。今日の消費者が求めているのは、先進的なエンジンや洗練されたデザインだけではありません。高速ワイヤレス技術の統合は、ドライバーや同乗者と自動車との関わり方を変え、自動車メーカーに新たな価値提案を生み出しています。自律走行、電動化、コネクテッドサービスへの注目が高まるにつれ、広帯域幅で低遅延の通信システムへの需要が高まっています。ワイヤレスモジュールは現在、インテリジェント交通システムのバックボーンと見なされており、リアルタイムナビゲーション、車両追跡、リモートソフトウェア更新、スマートシティ統合などの機能を可能にしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 39億米ドル |

| 予測金額 | 83億米ドル |

| CAGR | 9.2% |

常時接続車両へのシフトは、自動車業界全体の期待を再定義しています。今日の自動車購入者は、従来のテレマティクス以上のものを求めています。彼らは、ライブ交通データへのアクセス、モバイルアプリベースの車両制御、ストリーミングエンターテイメント、リアルタイムの車両健康状態の更新を求めています。これらの機能は、車両、クラウド、その他のコネクテッドインフラストラクチャ間の中断のない相互作用を保証する堅牢な無線通信モジュールに依存しています。5GとV2X(Vehicle-to-Everything)通信の普及は、高度な無線ソリューションの必要性をさらに高めています。これらの技術は、車両、インフラ、歩行者、そしてより広範なモビリティエコシステム間の超高信頼性、低遅延接続を約束します。安全規制が進化し、自動化レベルが高まるにつれて、一貫性のある高速データ伝送の必要性は高まるばかりで、自動車メーカーはすべてのモデルに無線モジュールを優先的に組み込む必要に迫られています。

多くの接続オプションがある中で、Wi-Fiは引き続き車載用ワイヤレスモジュール市場をリードしており、2024年には42.7%のシェアを占めています。この優位性は今後も続くとみられ、予測期間を通じて2桁成長の可能性が高いです。Wi-Fiは、OTA(Over-The-Air)アップデート、ビデオストリーミング、ナビゲーション、車載コネクティビティなど、データ量の多いアプリケーションに最適な技術です。自動車メーカーはWi-Fiモジュールを使ってリアルタイム診断を行い、サービスセンターに出向くことなくソフトウェアの機能強化を実現しています。電気自動車やハイブリッド車では、Wi-Fi対応システムがバッテリーの使用状況の監視、性能の最適化、充電ステーションとのシームレスな通信にも役立っています。よりスマートで環境に優しい自動車を求める動きが加速するにつれ、エネルギーシステムの管理と分析におけるWi-Fiの役割はますます重要になってきています。

車載用ワイヤレスモジュール市場は乗用車が圧倒的に多く、2024年のシェアは68.9%です。このセグメントが市場をリードしているのは、プレミアムセダンからコンパクトハッチバックまで、すべての車両クラスでコネクテッド機能が急速に進化し標準化されたおかげです。消費者は今や、クラウドベースのインフォテインメントシステム、アプリベースのコントロール、予測診断、音声アシスト機能を運転体験の一部として持つことに慣れています。自動車メーカーは、これらの機能をより効果的に提供し、総合的な顧客満足度を高めるために、ワイヤレスモジュールを車両アーキテクチャに組み込んでいます。競争が激化するにつれて、エントリーモデルでさえ高度なコネクティビティソリューションが搭載されるようになり、車載テクノロジーに対する期待のベースラインが高まっています。

中国の車載用ワイヤレスモジュール市場は、2024年に7億7,860万米ドルを創出し、世界シェア48%を占める。中国の優位性は、世界最大の自動車製造エコシステムに支えられた、コネクテッドモビリティと自律型モビリティへの積極的な取り組みに起因します。技術に精通した電気自動車に対する同国の需要の高まりは、政府の手厚い優遇措置や急速な5Gインフラの展開と相まって、V2Xや無線通信モジュールの高い普及率を後押ししています。国内自動車メーカーは、この勢いを利用してスマート機能を統合し、国内外市場で存在感を高めています。自動車エレクトロニクスへの継続的な投資とデジタルトランスフォーメーションの重視により、中国はワイヤレス車両接続の世界的リーダーとしての地位をさらに強固なものにすると予想されます。

Qualcomm Technologies, Mobileye, VALEO, NVIDIA, Aisin Seiki, Denso, Robert Bosch, Continental, BorgWarner, and ZF Friedrichshafen などの主要企業は、技術革新と戦略的パートナーシップに注力することで、市場での存在感を高めています。これらの企業は、5GとV2Xアプリケーションをサポートするために無線プラットフォームを強化し、AI機能を統合し、EVと自律走行車用のスケーラブルで電力効率の高いモジュールを展開しています。生産の現地化とクラウドベースのサービス提供の拡大により、コネクティビティ、自動化、リアルタイムのデータ交換によって急速に変化する市場環境の中で優位に立つことを目指しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 製造業者

- 原材料サプライヤー

- 自動車OEM

- 流通チャネル

- 最終用途

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 価格分析

- 推進

- 地域

- 影響要因

- 促進要因

- コネクテッドカーの需要の高まり

- 5GとV2X通信の採用増加

- IoTとスマートモビリティの進歩

- 車載機能に対する消費者の需要増加

- 業界の潜在的リスク&課題

- 高度な無線モジュールの高コスト

- サイバーセキュリティとデータプライバシーの懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:接続性別、2021-2034

- 主要動向

- Wi-Fi

- Bluetooth

- セルラー

- その他

第6章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV

- 商用車

- 軽作業

- 中型

- ヘビーデューティー

第7章 市場推計・予測:推進力別、2021-2034

- 主要動向

- ガソリン

- ディーゼル

- 電気

- PHEV

- ハイブリッド車

- 燃料電池自動車

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- ナビゲーション

- テレマティクス

- インフォテインメント

- 車両の安全と緊急サービス

- その他

第9章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Aisin Seiki

- Autotalks

- BorgWarner

- Continental

- Delphi Technologies

- Denso

- Harman International

- Huawei Technologies

- Infineon Technologies

- Magna International

- Mobileye

- NVIDIA

- NXP Semiconductors

- Panasonic

- Qualcomm Technologies

- Renesas Electronics

- Robert Bosch

- Skyworks Solutions

- VALEO

- ZF Friedrichshafen

The Global Automotive Wireless Module Market was valued at USD 3.9 billion in 2024 and is estimated to grow at a CAGR of 9.2% to reach USD 8.3 billion by 2034, driven by increasing consumer demand for connected vehicles and the rapid deployment of next-generation wireless technologies like 5G and V2X communication. As the automotive industry experiences a major shift toward digital transformation, wireless modules are becoming essential components in delivering smarter, safer, and more connected driving experiences. From enabling seamless infotainment systems to supporting predictive maintenance and remote diagnostics, these modules are reshaping how vehicles interact with their environment and users.

Automakers are doubling down on wireless connectivity features to enhance convenience, safety, and performance. Today's consumers are not just looking for advanced engines or sleek designs-they expect their vehicles to offer the same level of connectivity as their smartphones. The integration of high-speed wireless technologies is transforming the way drivers and passengers interact with their vehicles, creating new value propositions for automakers. The increasing focus on autonomous driving, electrification, and connected services is fueling the demand for high-bandwidth, low-latency communication systems. Wireless modules are now seen as the backbone of intelligent transportation systems, enabling features like real-time navigation, fleet tracking, remote software updates, and smart city integration.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.9 Billion |

| Forecast Value | $8.3 Billion |

| CAGR | 9.2% |

The shift toward always-connected vehicles is redefining expectations across the automotive landscape. Car buyers today demand more than traditional telematics-they want access to live traffic data, mobile app-based vehicle control, streaming entertainment, and real-time vehicle health updates. These capabilities rely on robust wireless communication modules that ensure uninterrupted interaction between the vehicle, cloud, and other connected infrastructure. The growing rollout of 5G and V2X (vehicle-to-everything) communication is further intensifying the need for advanced wireless solutions. These technologies promise ultra-reliable, low-latency connections between vehicles, infrastructure, pedestrians, and the broader mobility ecosystem. As safety regulations evolve and automation levels rise, the need for consistent, high-speed data transmission will only grow-pushing automakers to prioritize wireless module integration in every model.

Among the many connectivity options available, Wi-Fi continues to lead the automotive wireless module market, commanding a 42.7% share in 2024. This dominance is expected to continue, with strong potential for double-digit growth throughout the forecast period. Wi-Fi remains the go-to technology for data-heavy applications like over-the-air (OTA) updates, video streaming, navigation, and in-vehicle connectivity. Automakers are using Wi-Fi modules to perform real-time diagnostics and deliver software enhancements without requiring physical visits to service centers. In electric and hybrid vehicles, Wi-Fi-enabled systems also help monitor battery usage, optimize performance, and enable seamless communication with charging stations. As the push for smarter, greener vehicles gains momentum, the role of Wi-Fi in managing and analyzing energy systems is becoming increasingly critical.

Passenger vehicles dominate the automotive wireless module market, representing a 68.9% share in 2024. This segment leads the market thanks to the rapid evolution and standardization of connected features across all vehicle classes-from premium sedans to compact hatchbacks. Consumers are now accustomed to having cloud-based infotainment systems, app-based controls, predictive diagnostics, and voice-assisted functions as part of their driving experience. Automakers are embedding wireless modules into vehicle architecture to deliver these features more effectively and boost overall customer satisfaction. As competition intensifies, even entry-level models are being equipped with advanced connectivity solutions, raising the baseline expectations for in-car technology.

The China Automotive Wireless Module Market generated USD 778.6 million in 2024, capturing a 48% share globally. China's dominance stems from its aggressive push toward connected and autonomous mobility, supported by the world's largest automotive manufacturing ecosystem. The country's rising demand for tech-savvy electric vehicles, coupled with generous government incentives and rapid 5G infrastructure rollout, is fueling high adoption of V2X and wireless communication modules. Domestic automakers are leveraging this momentum to integrate smart features and expand their presence in both domestic and international markets. China's continued investment in automotive electronics and its emphasis on digital transformation are expected to further cement its position as a global leader in wireless vehicle connectivity.

Leading companies such as Qualcomm Technologies, Mobileye, VALEO, NVIDIA, Aisin Seiki, Denso, Robert Bosch, Continental, BorgWarner, and ZF Friedrichshafen are accelerating their market presence by focusing on innovation and strategic partnerships. These players are enhancing their wireless platforms to support 5G and V2X applications, integrating AI capabilities, and rolling out scalable, power-efficient modules for EVs and autonomous vehicles. By localizing production and expanding cloud-based service offerings, they aim to stay ahead in a fast-changing market landscape driven by connectivity, automation, and real-time data exchange.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Raw material suppliers

- 3.2.3 Automotive OEM

- 3.2.4 Distribution channel

- 3.2.5 End Use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Pricing analysis

- 3.9.1 Propulsion

- 3.9.2 Region

- 3.10 Impact on forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising demand for connected vehicles

- 3.10.1.2 Rising adoption of 5G and V2X communication

- 3.10.1.3 Advancements in IoT and smart mobility

- 3.10.1.4 Increased consumer demand for in-car features

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High cost of advanced wireless modules

- 3.10.2.2 Cybersecurity and data privacy concerns

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Connectivity, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Wi-Fi

- 5.3 Bluetooth

- 5.4 Cellular

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedans

- 6.2.2 Hatchback

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light duty

- 6.3.2 Medium duty

- 6.3.3 Heavy duty

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Gasoline

- 7.3 Diesel

- 7.4 Electric

- 7.4.1 PHEV

- 7.4.2 HEV

- 7.4.3 FCEV

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Navigation

- 8.3 Telematics

- 8.4 Infotainment

- 8.5 Vehicle safety and emergency services

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Aisin Seiki

- 11.2 Autotalks

- 11.3 BorgWarner

- 11.4 Continental

- 11.5 Delphi Technologies

- 11.6 Denso

- 11.7 Harman International

- 11.8 Huawei Technologies

- 11.9 Infineon Technologies

- 11.10 Magna International

- 11.11 Mobileye

- 11.12 NVIDIA

- 11.13 NXP Semiconductors

- 11.14 Panasonic

- 11.15 Qualcomm Technologies

- 11.16 Renesas Electronics

- 11.17 Robert Bosch

- 11.18 Skyworks Solutions

- 11.19 VALEO

- 11.20 ZF Friedrichshafen