|

|

市場調査レポート

商品コード

1740756

自動車用アクティブロールコントロールシステムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Automotive Active Roll Control System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 自動車用アクティブロールコントロールシステムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月21日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

自動車用アクティブロールコントロールシステムの世界市場規模は2024年に37億米ドルとなり、CAGR 4.2%で成長し、2034年には53億米ドルに達すると予測されます。

これは、車両の安定性、安全性、乗り心地の向上に対するニーズの高まり、特に成長著しいSUVや高級車セグメントにおけるニーズが原動力となっています。運転体験と路上での安全性を優先する消費者が増えるにつれ、アクティブロールコントロールシステムのような先進サスペンション技術の採用が加速し続けています。これらのシステムは、コーナリング時や不整地走行時のボディのロールを低減し、ハンドリングの精度と全体的な安全性を大幅に向上させる上で重要な役割を果たしています。快適性を損なうことなく、洗練されたパフォーマンス志向の乗り心地を提供することを目指す自動車メーカーが増える中、アクティブロールコントロールシステムは、最新の車両設計に不可欠なものと見なされるようになっています。

この市場は、SUVやクロスオーバー車の販売急増のおかげで勢いを増しており、どちらも重心が高く、スムーズで安全な走りを確保するために、より優れた動的制御が必要とされています。また、特に都市部や郊外の環境では、予測不可能な路面や高速コーナリングが一般的になっているため、消費者は実走行条件下での自動車の性能をより意識するようになっています。自動車メーカーは現在、顧客の期待に応え、ブランド価値を高めるため、プレミアム車だけでなく中級車にもアクティブロールコントロールシステムを搭載しています。同時に、電気自動車やハイブリッド車の占有面積が拡大しており、バッテリーシステムによって重量が増加することが多いため、特殊なサスペンションや安定性システムが必要とされ、アクティブロールコントロール技術の需要がさらに高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 37億米ドル |

| 予測金額 | 53億米ドル |

| CAGR | 4.2% |

欧州や北米といった主要地域の安全規制は、自動車メーカーに最先端技術への投資を促す上で大きな役割を果たしています。各国政府が自動車の安全性と性能に関するコンプライアンス基準をより厳しく課す中、メーカーは自動車の安全性プロファイルを強化する必要に迫られています。アクティブロールコントロールシステムは、このような規制上の要求を満たすと同時に、優れたドライビング体験を提供するものであり、将来の製品ラインアップの充実を目指すOEMにとって賢明な投資です。

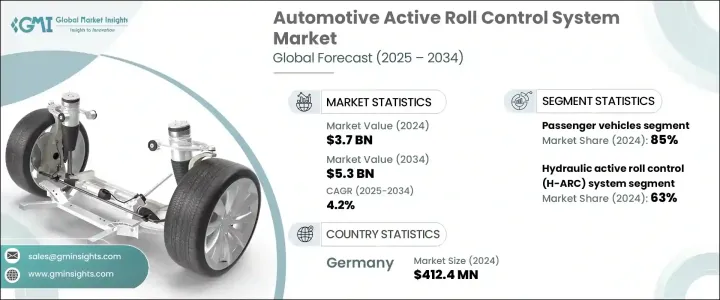

自動車用アクティブロールコントロールシステム市場は、油圧式アクティブロールコントロール(H-ARC)と電気機械式アクティブロールコントロール(eARC)の2つの主要技術に区分されます。2024年時点では、油圧システムが市場シェアの約63%を占め、この分野を支配しています。高い作動力、信頼性、速い応答時間で知られるH-ARCシステムは、優れた安定性と性能が譲れないSUVや高級車に広く使われています。これらのシステムは、特に重量のある車両に適しており、堅牢な性能を優先するメーカーにとって最適なソリューションであり続けています。

一方、電気機械式アクティブロールコントロールシステムは、特に自動車メーカーがよりエネルギー効率が高く、コンパクトで電子制御のソリューションを模索していることから、徐々に普及しつつあります。eARCが市場に占める割合はまだ小さいが、次世代EVやハイブリッド車への統合により、今後10年間で着実に普及が進むと予想されます。電動化とソフトウェア定義型車両へのシフトは、より精密な制御と車両エレクトロニクスとの統合を提供するeARCシステムの能力とよく合致しています。

乗用車は、2024年の世界市場シェアの約85%を占める主要な自動車カテゴリーです。このセグメントをリードしているのは、最高級の安全機能と相まってプレミアムな運転体験を提供する自動車への嗜好が高まっていることに起因しています。自動車メーカーが電気自動車やハイブリッド車の生産を拡大するにつれて、独自の設計や重量配分の課題に適応できる革新的なサスペンションシステムの必要性が高まっています。アクティブロールコントロールシステムはこの方程式に完璧に適合し、エネルギー効率を犠牲にすることなく制御性と快適性を向上させる。

ドイツは主要企業として際立っており、2024年の世界自動車用アクティブロールコントロールシステム市場で29%のシェアを占めています。世界トップクラスの高級車メーカーや高性能車メーカーを擁する堅調な自動車部門を擁するドイツは、最先端の自動車技術の採用でリードし続けています。強力な研究開発投資、成熟したサプライヤー基盤、厳格な規制の枠組みにより、ドイツは自動車カテゴリー全体への先進安定性システムの導入で主導的地位を維持しています。

この市場の主要企業には、ZF Friedrichshafen、ThyssenKrupp、Hyundai Mobis、Denso、Schaeffler、Robert Bosch、HELLA GmbH、Magna International、Continentalなどがあります。これらの企業は、よりスマートでコスト効率の高いロール制御ソリューションを開発するため、研究開発に多額の投資を行い、イノベーションを倍増させています。世界な自動車メーカーとの協力関係は、特にEVやハイブリッドモデルへのこれらのシステムの統合において、その範囲を広げています。規制の調整、技術の進歩、新興国でのプレゼンスに強力に注力することで、これらの企業は競争力を維持しながら、安全性、快適性、高性能運転に対する需要の高まりに応えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 部品サプライヤー

- ティア1サプライヤー

- 自動車メーカー(OEM)

- ソフトウェアおよびテクノロジープロバイダー

- 研究開発機関

- 利益率分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 他国による報復措置

- 業界への影響

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 価格動向

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 車両の安定性と操縦性の向上に対する需要の増加

- SUVや高級車の販売増加

- 安全機能を義務付ける厳格な政府規制

- 先進運転支援システム(ADAS)および自動運転技術との統合

- サスペンション技術の進歩

- 業界の潜在的リスク&課題

- 初期コストが高め

- 統合と調整の複雑さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- アクチュエータ

- 電子制御ユニット(ECU)

- センサー

- リンケージとマウント

第6章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- 油圧式アクティブロールコントロール(H-ARC)システム

- 電気機械式アクティブロールコントロール(eARC)システム

第7章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第8章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM(オリジナル機器メーカー)

- アフターマーケット

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Benteler

- BWI Group

- Continental

- Denso

- Eibach

- HELLA GmbH

- Hitachi Astemo

- Hyundai Mobis

- Infineon Technologies

- JTEKT Corporation

- KYB Corporation

- Magna International

- Mando Corporation

- Robert Bosch

- Schaeffler

- Tenneco

- ThyssenKrupp

- TRW Automotive

- WABCO

- ZF Friedrichshafen

The Global Automotive Active Roll Control System Market was valued at USD 3.7 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 5.3 billion by 2034, driven by the rising need for enhanced vehicle stability, safety, and ride comfort-especially in the growing SUV and luxury vehicle segments. As more consumers prioritize driving experience and on-road safety, the adoption of advanced suspension technologies like active roll control systems continues to accelerate. These systems play a vital role in reducing body roll when cornering or driving on uneven terrain, significantly improving handling precision and overall safety. With more automakers aiming to deliver a refined, performance-oriented ride without compromising comfort, active roll control systems are now seen as critical to modern vehicle design.

This market is witnessing increased momentum thanks to the surge in SUV and crossover vehicle sales, both of which have a higher center of gravity and require better dynamic control to ensure a smooth and safe ride. Consumers are also becoming more conscious of how vehicles perform in real-world driving conditions, especially with unpredictable road surfaces and high-speed cornering becoming more common in urban and suburban environments. Automakers are now integrating active roll control systems not only in premium vehicles but also in mid-range models to meet customer expectations and boost brand value. At the same time, the growing footprint of electric and hybrid vehicles-which often carry additional weight due to battery systems-calls for specialized suspension and stability systems, further fueling demand for active roll control technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 4.2% |

Safety regulations across key regions like Europe and North America are playing a major role in pushing automakers to invest in cutting-edge technologies. As governments impose stricter compliance norms around vehicle safety and performance, manufacturers are under pressure to enhance the safety profiles of their vehicles. Active roll control systems help meet these regulatory demands while simultaneously offering a superior driving experience, making them a smart investment for OEMs looking to future-proof their product lines.

The automotive active roll control system market is segmented into two primary technologies: hydraulic active roll control (H-ARC) and electromechanical active roll control (eARC). As of 2024, hydraulic systems dominate the space, accounting for nearly 63% of the market share. Known for their high actuation force, reliability, and fast response times, H-ARC systems are widely used in SUVs and luxury vehicles where superior stability and performance are non-negotiable. These systems are particularly suited for heavier vehicles and continue to be the go-to solution for manufacturers prioritizing robust performance.

On the other hand, electromechanical active roll control systems are gradually gaining traction, especially as automakers explore more energy-efficient, compact, and electronically controlled solutions. While eARC still holds a smaller portion of the market, its integration into next-gen EVs and hybrids is expected to drive steady adoption over the next decade. The shift toward electrification and software-defined vehicles aligns well with the capabilities of eARC systems, which offer more precise control and integration with vehicle electronics.

Passenger cars represent the dominant vehicle category, capturing around 85% of the global market share in 2024. This segment's lead stems from the growing preference for cars that offer a premium driving experience coupled with top-tier safety features. As automakers ramp up the production of electric and hybrid cars, there is an increasing need for innovative suspension systems that can adapt to unique design and weight distribution challenges. Active roll control systems fit perfectly into this equation, offering enhanced control and comfort without sacrificing energy efficiency.

Germany stands out as a major player, holding a 29% share of the global automotive active roll control system market in 2024. With its robust automotive sector-home to some of the world's top luxury and performance car manufacturers-Germany continues to lead in the adoption of cutting-edge vehicle technologies. Strong R&D investment, a mature supplier base, and stringent regulatory frameworks have helped the country maintain a leadership position in deploying advanced stability systems across vehicle categories.

Key players in this market include ZF Friedrichshafen, ThyssenKrupp, Hyundai Mobis, Denso, Schaeffler, Robert Bosch, HELLA GmbH, Magna International, and Continental. These companies are doubling down on innovation by investing heavily in R&D to develop smarter, more cost-effective roll control solutions. Collaborations with global automakers are expanding their reach, especially in integrating these systems into EVs and hybrid models. A strong focus on regulatory alignment, technology advancement, and presence in emerging economies is allowing these companies to stay competitive while meeting rising demand for safety, comfort, and high-performance driving.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component suppliers

- 3.2.2 Tier 1 suppliers

- 3.2.3 Automotive manufacturers (OEMs)

- 3.2.4 Software and technology providers

- 3.2.5 Research and development institutions

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price Volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Production cost implications

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Price trends

- 3.7 Patent analysis

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing demand for enhanced vehicle stability and handling

- 3.10.1.2 Increasing sales of SUVs and luxury vehicles

- 3.10.1.3 Stringent government regulations mandating safety features

- 3.10.1.4 Integration with advanced driver-assistance systems (ADAS) and autonomous driving technologies

- 3.10.1.5 Advancements in suspension technologies

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High initial cost

- 3.10.2.2 Complexity of integration and calibration

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Actuators

- 5.3 Electronic Control Units (ECUs)

- 5.4 Sensors

- 5.5 Linkages and mounts

Chapter 6 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Hydraulic active roll control (H-ARC) system

- 6.3 Electromechanical active roll control (eARC) system

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Medium Commercial Vehicles (MCV)

- 7.3.3 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 OEMs (Original Equipment Manufacturers)

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Benteler

- 10.2 BWI Group

- 10.3 Continental

- 10.4 Denso

- 10.5 Eibach

- 10.6 HELLA GmbH

- 10.7 Hitachi Astemo

- 10.8 Hyundai Mobis

- 10.9 Infineon Technologies

- 10.10 JTEKT Corporation

- 10.11 KYB Corporation

- 10.12 Magna International

- 10.13 Mando Corporation

- 10.14 Robert Bosch

- 10.15 Schaeffler

- 10.16 Tenneco

- 10.17 ThyssenKrupp

- 10.18 TRW Automotive

- 10.19 WABCO

- 10.20 ZF Friedrichshafen