|

市場調査レポート

商品コード

1665070

自動車配電システム市場の機会、成長促進要因、産業動向分析、2025~2034年の予測Automotive Electrical Distribution Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車配電システム市場の機会、成長促進要因、産業動向分析、2025~2034年の予測 |

|

出版日: 2024年12月11日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

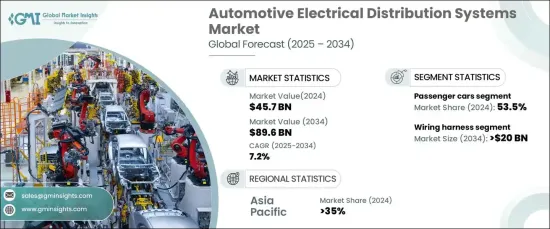

世界の自動車配電システム市場は、2024年に457億米ドルとなり、2025年から2034年にかけてCAGR 7.2%で堅調に拡大すると予測されています。

この成長は、電力管理、エネルギー効率、車両性能全体を最適化するために高度な電気部品に大きく依存する電気自動車やハイブリッド車の採用が急増していることが背景にあります。

市場拡大の主な要因は、ADAS(先進運転支援システム)に対する需要の高まりです。アダプティブ・クルーズ・コントロール、レーンキーピング・アシスタンス、自動駐車、衝突回避、緊急ブレーキといったこれらの最先端技術は、リアルタイムでデータを処理するセンサー、カメラ、レーダー、電子デバイスの複雑なネットワークに依存しています。この複雑さが、ADASの機能性を実現する上で高度な配電システムが果たす重要な役割を浮き彫りにし、市場の成長をさらに後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 457億米ドル |

| 予測金額 | 896億米ドル |

| CAGR | 7.2% |

同市場は、ワイヤーハーネス、ヒューズ・リレーシステム、スイッチ・センサー、コネクター・端子、制御モジュール(ECU)、その他を含むコンポーネント別に区分されます。2024年には、ワイヤーハーネス分野が24%の市場シェアを占め、2034年までに200億米ドルを創出すると予測されています。ワイヤーハーネスは、自動車配電システムに不可欠なもので、さまざまな車両コンポーネントに電力と信号を伝送するための基幹部品として機能します。

車種別では、乗用車、商用車、オフハイウェイ車、電気自動車、ハイブリッド車が含まれます。乗用車は2024年の市場シェア53.5%を占め、生産台数の多さと普及に牽引されています。これらの自動車には、インフォテインメント、空調制御、照明、安全機能、パワートレイン管理、ADASなどの高度なシステムに電力を供給するための幅広い電気部品が組み込まれており、現代の消費者の需要に応えています。

アジア太平洋地域は、自動車配電システム市場において重要なプレーヤーとして台頭し、2024年には35%のシェアを占めています。この優位性は、同地域が自動車製造の世界の中心地であることと、電気自動車の急速な普及に起因しています。中国のような国は、従来型自動車と電気自動車の両方の生産に貢献しており、バッテリー管理システム(BMS)、高電圧ワイヤーハーネス、ECUのような重要な配電部品の需要を促進しています。これらの部品は、特に電気自動車において効率的な配電とエネルギー管理に不可欠です。

報告書の内容

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 自動車OEM

- 技術プロバイダー

- 半導体メーカー

- エンドユーザー

- 利益率分析

- テクノロジーとイノベーションの展望

- コスト内訳

- 特許状況

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 電気自動車とハイブリッド車の採用拡大

- 厳しい排ガス・燃費規制

- ADAS(先進運転支援システム)の需要

- 厳しい排ガス・燃費規制

- 業界の潜在的リスク&課題

- 世界の半導体不足

- 高い製造コスト

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ワイヤーハーネス

- ヒューズ&リレー

- スイッチ&センサー

- コネクター・端子

- 制御モジュール(ECU)

- その他

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- LCV

- HCV

- オフハイウェイ車

- EVとハイブリッド

第7章 市場推計・予測:電圧別、2021~2034年

- 主要動向

- 12V

- 48V

- 400V以上

第8章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 従来型

- 先進技術

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Amphenol

- Aptiv

- Draexlmaier

- Eaton

- Furukawa Electric

- Lear

- Leoni

- Littelfuse

- Magna International

- PKC Group

- Prysmian Group

- Rheinmetall

- Samvardhana Motherson

- Spark Minda

- Sumitomo Electric Industries

- TE Connectivity

- Vitesco Technologies

- Yazaki

The Global Automotive Electrical Distribution System Market was valued at USD 45.7 billion in 2024 and is projected to expand at a robust CAGR of 7.2% between 2025 and 2034. This growth is driven by the surging adoption of electric and hybrid vehicles, which rely extensively on advanced electrical components to optimize power management, energy efficiency, and overall vehicle performance.

A key driver of market expansion is the rising demand for Advanced Driver Assistance Systems (ADAS). These cutting-edge technologies, such as adaptive cruise control, lane-keeping assistance, automatic parking, collision avoidance, and emergency braking, rely on an intricate network of sensors, cameras, radars, and electronic devices to process data in real time. This complexity underscores the critical role of sophisticated electrical distribution systems in enabling ADAS functionalities, further propelling market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $45.7 Billion |

| Forecast Value | $89.6 Billion |

| CAGR | 7.2% |

The market is segmented by components, including wiring harnesses, fuse and relay systems, switches and sensors, connectors and terminals, control modules (ECUs), and others. In 2024, the wiring harness segment held a 24% market share and is anticipated to generate USD 20 billion by 2034. Wiring harnesses are integral to automotive electrical distribution systems, serving as the backbone for transmitting electrical power and signals across various vehicle components.

By vehicle type, the market encompasses passenger cars, commercial vehicles, off-highway vehicles, and electric and hybrid vehicles. Passenger cars dominated the market in 2024, capturing a 53.5% share, driven by high production volumes and widespread adoption. These vehicles incorporate a broad spectrum of electrical components to power advanced systems, including infotainment, climate control, lighting, safety features, powertrain management, and ADAS, catering to modern consumer demands.

The Asia Pacific region emerged as a significant player in the automotive electrical distribution system market, accounting for a 35% share in 2024. This dominance is attributed to the region's position as a global hub for automotive manufacturing and the rapid adoption of electric vehicles. Nations like China are leading contributors to both conventional and electric vehicle production, driving demand for essential electrical distribution components such as battery management systems (BMS), high-voltage wiring harnesses, and ECUs. These components are crucial for efficient power distribution and energy management, particularly in electric vehicles.

Report Content

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Automotive OEMs

- 3.2.2 Technology providers

- 3.2.3 Semiconductor manufacturers

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Cost breakdown

- 3.6 Patent landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Growing adoption of electric and hybrid vehicles

- 3.9.1.2 Stringent emission and fuel efficiency regulations

- 3.9.1.3 Demand for advanced driver assistance systems (ADAS)

- 3.9.1.4 Stringent emission and fuel efficiency regulations

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Global semiconductor shortage

- 3.9.2.2 High manufacturing costs

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Wiring harness

- 5.3 Fuse & relay

- 5.4 Switches & sensors

- 5.5 Connectors & terminals

- 5.6 Control modules (ECUs)

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicle

- 6.3.1 LCV

- 6.3.2 HCV

- 6.4 Off highway vehicle

- 6.5 EVs and hybrid

Chapter 7 Market Estimates & Forecast, By Voltage, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 12v

- 7.3 48v

- 7.4 Above 400V

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Conventional

- 8.3 Advanced

Chapter 9 Market Estimates & Forecast, By End use, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Amphenol

- 11.2 Aptiv

- 11.3 Draexlmaier

- 11.4 Eaton

- 11.5 Furukawa Electric

- 11.6 Lear

- 11.7 Leoni

- 11.8 Littelfuse

- 11.9 Magna International

- 11.10 PKC Group

- 11.11 Prysmian Group

- 11.12 Rheinmetall

- 11.13 Samvardhana Motherson

- 11.14 Spark Minda

- 11.15 Sumitomo Electric Industries

- 11.16 TE Connectivity

- 11.17 Vitesco Technologies

- 11.18 Yazaki