|

市場調査レポート

商品コード

2038343

電気自動車用減速機市場の機会、成長要因、業界動向分析、および2026年~2035年の予測Electric Vehicle Reducer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 電気自動車用減速機市場の機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年04月16日

発行: Global Market Insights Inc.

ページ情報: 英文 285 Pages

納期: 2~3営業日

|

概要

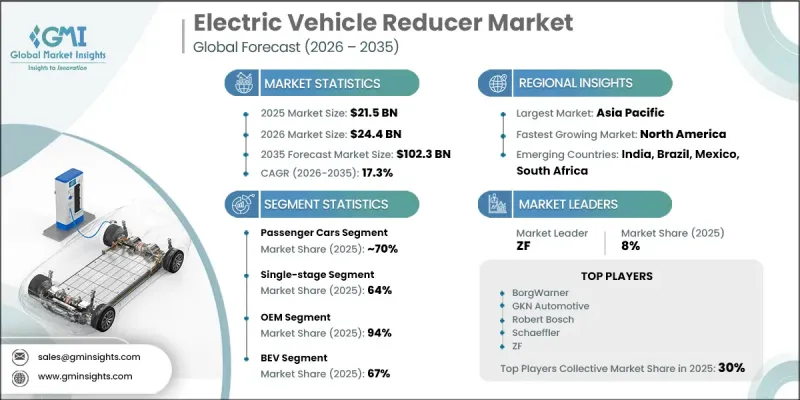

世界の電気自動車用減速機市場は、2025年に215億米ドルと評価され、2035年までにCAGR 17.3%で成長し、1,023億米ドルに達すると予測されています。

電気自動車の普及が加速する中、モーターの回転速度を効率的に利用可能なトルクに変換する高度な減速機システムへの需要が、ますます重要になってきています。電気自動車の生産台数の増加に伴い、メーカー各社はコンパクトで軽量、かつ高性能な減速機ソリューションの開発に注力するようになっています。企業がエネルギー効率の向上と車両性能の最適化を目指す中、ドライブトレイン設計の継続的な改善が市場の成長をさらに後押ししています。電気パワートレイン技術の進歩に支えられた自動車業界の変革は、減速機システムにおけるイノベーションの新たな機会を生み出しています。さらに、電気自動車の生産およびインフラへの投資拡大が需要を後押ししており、減速機技術は持続可能なモビリティへの移行において不可欠な要素としての地位を確立しつつあります。

| 市場の範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 215億米ドル |

| 予測額 | 1,023億米ドル |

| CAGR | 17.3% |

電気自動車用減速機市場は、複数の車種にまたがる電動化輸送手段の急速な拡大によって、さらに後押しされています。電動モビリティソリューションへの需要の高まりは、多様な運用要件に対応できる堅牢かつ効率的な減速機システムに対する強いニーズを生み出しています。電気自動車の製造およびインフラ開発への投資増加が普及率の向上に寄与している一方、国内生産能力の強化に向けた取り組みは、サプライチェーンへの依存度を低減し、長期的な市場成長を支えています。

乗用車セグメントは2025年に70%のシェアを占め、2026年から2035年にかけてCAGR18%超で成長すると予想されています。電気乗用車の普及拡大は、性能とエネルギー効率を向上させる減速機システムへの需要を大幅に押し上げています。自動車メーカーが新たな電気自動車モデルを次々と投入する中、最適化された駆動系コンポーネントの重要性はますます高まっており、車両全体の機能性と運転体験を支えています。

単段減速機セグメントは2025年に64%のシェアを占め、2026年から2035年にかけてCAGR17%で成長すると予測されています。そのシンプルな設計と部品構成の簡素化により、電気自動車メーカーにとってコスト効率に優れたソリューションとなっています。手頃な価格と製造プロセスの効率化への注力が導入を後押ししており、特に業界が電気自動車の普及拡大に取り組む中でその傾向は顕著です。また、高速モーター技術との互換性も、その利用拡大にさらに寄与しています。

中国の電気自動車用減速機市場は、2025年に54%のシェアを占め、56億米ドルの市場規模を記録しました。強力な政策支援と電気自動車の普及を促進する取り組みが、生産と需要の両方の拡大において重要な役割を果たしてきました。国内製造の促進と電動化の加速を目的とした政府主導の施策により、中国は世界市場における主要な貢献国としての地位を強化しています。その結果としての電気自動車生産の増加は、減速機システムに対する大きな需要を引き続き牽引しています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 世界のEV普及の拡大

- e-アクスルおよび統合型ドライブトレインシステムの進展

- 高トルク密度および高効率への需要

- 高性能およびプレミアムEVの成長

- 業界の潜在的リスク&課題

- 高精度な製造要件

- 騒音・振動・不快感(NVH)の問題

- 原材料価格の変動

- EVプラットフォーム間の標準化が限定的

- 市場機会

- 商用電気自動車の拡大

- マルチスピード減速機の登場

- 新興市場における成長

- 軽量材料のイノベーション

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 環境保護庁(EPA)

- 米国道路交通安全局(NHTSA)-FMVSS 500

- 労働安全衛生局(OSHA)

- カナダ自動車安全基準(CMVSS)

- 州ごとの道路利用規制

- 欧州

- EU機械指令

- CEマーキングの適合性

- 低電圧指令(LVD)

- 電磁両立性(EMC)指令

- 各国の道路型式認定要件

- アジア太平洋地域

- 中国のEVおよびLSVに関する規制の枠組み

- インド中央自動車規則(CMVR)

- 日本の道路運送車両法

- ASEANにおけるEV政策の調和に向けた取り組み

- オーストラリア設計規則(ADR)

- ラテンアメリカ

- ブラジル国家交通評議会(CONTRAN)の規制

- メキシコのNOM基準

- 地域別の都市モビリティおよびEVインセンティブプログラム

- 中東・アフリカ

- GCC地域の車両適合性および型式認定規制

- 南アフリカ共和国道路交通法(NRTA)

- 観光およびフリーゾーンの運営基準

- 北米

- ポーター分析

- PESTEL分析

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格分析(1次調査に基づく)

- 過去の価格動向分析

- 事業者タイプ別の価格戦略(プレミアム/バリュー/コストプラス)

- 貿易データ分析(有料調査に基づく)

- 輸出入量および輸出入額の動向

- 主要な貿易回廊と関税の影響

- コスト内訳分析

- 特許分析(1次調査に基づく)

- 持続可能性および環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境配慮型イニシアチブ

- カーボンフットプリントに関する考察

- AIおよび生成AIが市場に与える影響

- AIによる既存ビジネスモデルの変革

- セグメント別のGenAIの使用事例と導入ロードマップ

- リスク、制約、および規制上の考慮事項

- 生産能力および生産動向(1次調査に基づく)

- 地域別・主要生産者別の導入容量

- 稼働率および拡張計画

- 予測の前提条件およびシナリオ分析(1次調査に基づく)

- ベースケース-CAGRを牽引する主要なマクロ経済および業界変数

- 楽観的シナリオ- マクロ経済および業界における追い風

- 悲観シナリオ- マクロ経済の減速または業界の逆風

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ(MEA)

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- パートナーシップおよび提携

- 新製品の発売

- 事業拡大計画と資金調達

- 企業のティア別ベンチマーク

- ティア分類基準および選定基準

- 売上高、地域、イノベーション別のティア位置付けマトリックス

第5章 市場推計・予測:車両別、2022-2035

- 乗用車

- セダン

- SUV

- ハッチバック

- 商用車

- LCV

- MCV

- 大型車(HCV)

- オフハイウェイ車両

- 二輪車および三輪車

第6章 市場推計・予測:減速機別、2022-2035

- 単段式

- 多段式

第7章 市場推計・予測:EV別、2022-2035

- BEV

- PHEV

- FCEV

- HEV

第8章 市場推計・予測:販売チャネル別、2022-2035

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- 東南アジア

- ANZ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ(MEA)

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- 世界企業

- BorgWarner

- Bosch

- Dana

- GKN Automotive

- Nidec

- Valeo

- Vitesco Technologies

- ZF Friedrichshafen

- 地域プレイヤー

- HL Mando

- Hyundai Mobis

- Hyundai Wia

- Jatco

- LG Magna e-Powertrain

- Punch Powertrain

- Ricardo

- TATA AutoComp

- Zhejiang Wanliyang

- 新興企業

- SAMHYUN

- OOKSAN IMT

- Youngjin Mobility

- RSB Global