産業用電気ボイラーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Industrial Electric Boiler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1721624

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

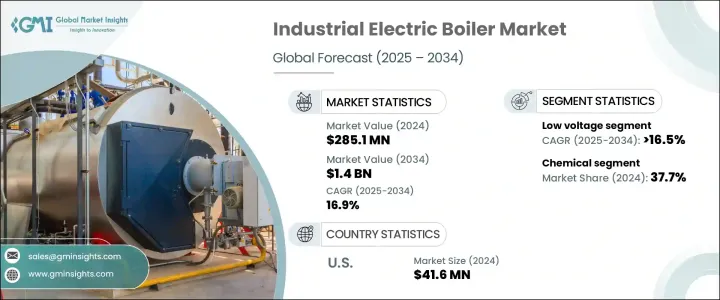

世界の産業用電気ボイラー市場は、2024年に2億8,510万米ドルと評価され、持続可能なエネルギーシステムへの世界の後押しが勢いを増すにつれて、CAGR 16.9%の堅調な成長を遂げ、2034年には14億米ドルに達する見通しです。

エネルギー効率の高いソリューションに対する需要の高まりや、クリーンエネルギーの導入を加速することを目的とした政府の取り組みが主な原因となって、産業界は急速に電気暖房システムにシフトしています。こうした動向は、さまざまな産業環境における電気ボイラーの導入拡大に大きく寄与しています。

進化する規制の枠組みも、企業に暖房インフラの再考を促しています。工業地帯における窒素酸化物(NOx)と硫黄酸化物(SOx)の排出規制が強化されるにつれて、従来の燃料ベースのシステムへの依存を減らすよう企業に求める圧力が高まっています。電気ボイラーは、脱炭素化の目標に沿った、よりクリーンで環境に優しい代替手段であり、運転効率を損なうことなく大きな環境メリットを提供します。技術の進歩、特に大容量ユニットの開発とAIを活用したエネルギー管理ツールとの統合により、電気ボイラーはより広範な産業用途にとってより実行可能で魅力的な選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 2億8,510万米ドル |

| 予測金額 | 14億米ドル |

| CAGR | 16.9% |

先進経済諸国と新興経済諸国の両方で工業化のペースが上昇していることが、市場を前進させる主な要因です。この成長は、エネルギー・インフラの改善に向けた投資の増加や、持続可能な製造プロセスへの関心の高まりによってさらに支えられています。特に、電気ボイラーの性能と効率の改善に焦点を当てた研究開発費の増加が、重要な役割を果たしています。こうした開発は、大容量でエネルギー効率の高い加熱が不可欠な化学処理のような産業の拡大によって補完されています。

産業用電気ボイラーは、近代的な産業施設に不可欠な設備として見なされるようになってきています。電気で熱を発生させるため、燃焼の必要がなく、その結果排出されるガスもありません。また、より静かでコンパクトなシステムであるため、メンテナンスも少なくて済みます。こうした特性により、信頼性が高く、排出ガスを出さない暖房技術を求めるセクターからの関心が高まっています。

クリーンで静かな操業を優先する業界からの需要が顕著に増加しています。中でも飲食品部門は、電気ボイラーの普及拡大に貢献しています。並行して、発電技術の進化と送電網インフラの改善が、電気ボイラーの普及に必要な支援となっています。高出力でありながらスペース効率の高い設計の導入も、スペースに制約のある産業環境での採用率を高める重要な開発です。

市場は定格電圧別に低電圧と中電圧に分類されます。コスト的に安定した効率的な暖房システムへの需要の高まりに対応するため、産業用暖房ネットワークの共有化が進んでいます。これらのネットワークは、特に長期的なエネルギー支出の削減を目指す地域で、電気ボイラーの使用を促進しています。低電圧分野は、2034年までCAGR16.5%以上の成長が見込まれています。その力強い成長軌道は、低電圧ユニットがコンパクトでメンテナンスが容易であるという利点とともに、クリーンエネルギー導入に対する税制優遇措置など、政府の支援政策によるところが大きいです。

用途別では、飲食品、製紙、化学、精製などの産業が含まれます。化学分野が最大のシェアを占め、2024年には市場全体の37.7%を占める。特に発展途上地域を中心に化学製造施設の拡大が続いており、効率的で環境に優しい暖房システムへの大きな需要が生まれています。企業は、厳しい環境基準を満たしながら安定した性能を提供できる電気ボイラーを支持しています。

米国の産業用電気ボイラー市場は着実な成長を示しており、2023年の3,640万米ドル、2022年の3,150万米ドルから、2024年には4,160万米ドルに達します。この上昇動向は、クリーンエネルギー税額控除の拡大や、産業電化を促進する世界の広範な取り組みによって後押しされています。こうした取り組みは、化石燃料ベースのシステムを電気代替品に置き換えることを企業に促し、市場の拡大をさらに後押ししています。

北米地域では、2034年までのCAGRが21.5%を超えると予測されています。同地域の好調は、産業活動の活発化、急速な技術革新、高度な産業インフラの構築を目指した官民パートナーシップに関連しています。このようなダイナミクスにより、北米は世界の電気ボイラー市場における主要プレーヤーとして位置づけられています。

産業用電気ボイラー市場には、先進的で効率的なボイラーシステムを提供することで知られる大手メーカーが複数あります。例えば、ALFA LAVAL、Acme Engineering Products、ACV、Babcock Wanson、Bosch Industriekessel、Cerney、Chromalox、Cleaver-Brooks、Danstoker A/S、Ecotherm Austria、FERROLI、Klopper-Therm、LACAZE ENERGIES、PARAT Halvorsen AS、Precision Boilers、Reimers Electra Steam、Ross Boilers、Thermodyne Boilers、Thermon、Thermona、Vapor Powerなどです。これらの企業は、持続可能な産業用加熱技術に対する世界の需要の高まりに対応するため、製品革新とエネルギー効率の高いソリューションに積極的に投資しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- トランプ政権の関税が貿易と産業全体に与える影響

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:電圧定格別、2021-2034

- 主要動向

- 低電圧

- 中電圧

第6章 市場規模・予測:容量別、2021-2034

- 主要動向

- 10 MMBTU/時未満

- 10~50 MMBTU/時

- 50~100 MMBTU/時

- 100~250 MMBTU/時

- 250 MMBTU/時以上

第7章 市場規模・予測:用途別、2021-2034

- 主要動向

- 食品と飲料

- 紙

- 化学薬品

- 製油所

- その他

第8章 市場規模・予測:製品別、2021-2034

- 主要動向

- お湯

- スチーム

第9章 市場規模・予測:販売チャネル別、2021-2034

- 主要動向

- オンライン

- ディーラー

- 小売り

第10章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- フランス

- 英国

- ポーランド

- イタリア

- スペイン

- ドイツ

- ロシア

- オーストリア

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- インドネシア

- フィリピン

- 中東・アフリカ

- サウジアラビア

- イラン

- アラブ首長国連邦

- エジプト

- ナイジェリア

- ケニア

- モロッコ

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- コロンビア

- チリ

第11章 企業プロファイル

- ALFA LAVAL

- Acme Engineering Products

- ACV

- Babcock Wanson

- Bosch Industriekessel

- Cerney

- Chromalox

- Cleaver-Brooks

- Danstoker A/S

- Ecotherm Austria

- FERROLI

- Klopper-Therm

- LACAZE ENERGIES

- PARAT Halvorsen AS

- Precision Boilers

- Reimers Electra Steam

- Ross Boilers

- Thermodyne Boilers

- Thermon

- Thermona

- Vapor Power

目次

The Global Industrial Electric Boiler Market, valued at USD 285.1 million in 2024, is poised to grow at a robust CAGR of 16.9% to reach USD 1.4 billion by 2034, as the global push toward sustainable energy systems gathers momentum. Industries are rapidly shifting toward electric heating systems, largely due to the rising demand for energy-efficient solutions and government initiatives aimed at accelerating clean energy adoption. These trends are contributing significantly to the increased deployment of electric boilers in various industrial environments.

The evolving regulatory framework is also encouraging businesses to rethink their heating infrastructure. As emission limits for nitrogen oxides (NOx) and sulfur oxides (SOx) tighten in industrial zones, there is growing pressure on companies to reduce their reliance on conventional fuel-based systems. Electric boilers present a cleaner, greener alternative that aligns with decarbonization goals, offering significant environmental benefits without compromising operational efficiency. Technological advancements, especially in the development of high-capacity units and integration with AI-powered energy management tools, are making electric boilers a more viable and attractive option for a wider range of industrial applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $285.1 Million |

| Forecast Value | $1.4 Billion |

| CAGR | 16.9% |

The rising pace of industrialization across both developed and emerging economies is a key factor driving the market forward. This growth is further supported by rising investments in upgrading energy infrastructure and growing interest in sustainable manufacturing processes. In particular, increased R&D spending focused on improving electric boiler performance and efficiency is playing a crucial role. These developments are being complemented by the expansion of industries like chemical processing, where high-capacity, energy-efficient heating is essential.

Industrial electric boilers are increasingly viewed as essential equipment in modern industrial facilities. They rely on electricity to generate heat, eliminating the need for combustion and the resulting emissions. This not only helps reduce the environmental impact of industrial operations but also offers quieter, more compact systems that require less maintenance. These attributes are driving greater interest from sectors seeking reliable, emission-free heating technologies.

There is a noticeable increase in demand from industries that prioritize clean and silent operations. The food and beverage sector, among others, is contributing to the expanding footprint of electric boilers. In parallel, the evolution of power generation technologies and improvements in grid infrastructure are providing the necessary support for widespread electric boiler deployment. The introduction of high-output yet space-efficient designs is another key development enhancing adoption rates across space-constrained industrial settings.

The market is categorized by voltage rating into low voltage and medium voltage segments. A rising number of shared industrial heating networks are emerging as a response to the growing demand for cost-stable, efficient heating systems. These networks are promoting the use of electric boilers, particularly in areas looking to reduce long-term energy expenditures. The low voltage segment is expected to grow at a CAGR of over 16.5% through 2034. Its strong growth trajectory is largely attributed to supportive government policies, such as tax incentives for clean energy adoption, along with the benefits of low voltage units being compact and easy to maintain.

By application, the market includes industries such as food and beverages, paper, chemicals, refinery, and others. The chemical segment holds the largest share, accounting for 37.7% of the total market in 2024. The ongoing expansion in chemical manufacturing facilities, especially across developing regions, is creating significant demand for efficient, environmentally friendly heating systems. Companies are favoring electric boilers due to their ability to deliver consistent performance while meeting stringent environmental standards.

The U.S. industrial electric boiler market has demonstrated steady growth, reaching USD 41.6 million in 2024, up from USD 36.4 million in 2023 and USD 31.5 million in 2022. This upward trend is being fueled by an expanding range of clean energy tax credits and broader global efforts to promote industrial electrification. These initiatives are encouraging companies to replace fossil fuel-based systems with electric alternatives, further supporting market expansion.

Across the North America region, the market is projected to grow at a CAGR of over 21.5% through 2034. The region's strong performance can be linked to increasing industrial activity, rapid technological innovation, and public-private partnerships aimed at building advanced industrial infrastructure. These dynamics are positioning North America as a key player in the global electric boiler space.

The industrial electric boiler market features several leading manufacturers known for offering advanced and efficient boiler systems. These include ALFA LAVAL, Acme Engineering Products, ACV, Babcock Wanson, Bosch Industriekessel, Cerney, Chromalox, Cleaver-Brooks, Danstoker A/S, Ecotherm Austria, FERROLI, Klopper-Therm, LACAZE ENERGIES, PARAT Halvorsen AS, Precision Boilers, Reimers Electra Steam, Ross Boilers, Thermodyne Boilers, Thermon, Thermona, and Vapor Power. These companies are actively investing in product innovation and energy-efficient solutions to meet the growing global demand for sustainable industrial heating technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Impact of trump administration tariffs on trade & overall industry

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Voltage Rating, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Low voltage

- 5.3 Medium voltage

Chapter 6 Market Size and Forecast, By Capacity, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 < 10 MMBTU/hr

- 6.3 10 - 50 MMBTU/hr

- 6.4 50 - 100 MMBTU/hr

- 6.5 100 - 250 MMBTU/hr

- 6.6 > 250 MMBTU/hr

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.3 Paper

- 7.4 Chemical

- 7.5 Refinery

- 7.6 Others

Chapter 8 Market Size and Forecast, By Product, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Hot water

- 8.3 Steam

Chapter 9 Market Size and Forecast, By Sales Channel, 2021 - 2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 Online

- 9.3 Dealer

- 9.4 Retail

Chapter 10 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 France

- 10.3.2 UK

- 10.3.3 Poland

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Germany

- 10.3.7 Russia

- 10.3.8 Austria

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Philippines

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 Iran

- 10.5.3 UAE

- 10.5.4 Egypt

- 10.5.5 Nigeria

- 10.5.6 Kenya

- 10.5.7 Morocco

- 10.5.8 South Africa

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

- 10.6.3 Colombia

- 10.6.4 Chile

Chapter 11 Company Profiles

- 11.1 ALFA LAVAL

- 11.2 Acme Engineering Products

- 11.3 ACV

- 11.4 Babcock Wanson

- 11.5 Bosch Industriekessel

- 11.6 Cerney

- 11.7 Chromalox

- 11.8 Cleaver-Brooks

- 11.9 Danstoker A/S

- 11.10 Ecotherm Austria

- 11.11 FERROLI

- 11.12 Klopper-Therm

- 11.13 LACAZE ENERGIES

- 11.14 PARAT Halvorsen AS

- 11.15 Precision Boilers

- 11.16 Reimers Electra Steam

- 11.17 Ross Boilers

- 11.18 Thermodyne Boilers

- 11.19 Thermon

- 11.20 Thermona

- 11.21 Vapor Power

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日