|

市場調査レポート

商品コード

1721538

ポイントオブケア凝固検査製品の市場機会、成長促進要因、業界動向分析、2025年~2034年予測Point of Care Coagulation Testing Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ポイントオブケア凝固検査製品の市場機会、成長促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年04月07日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

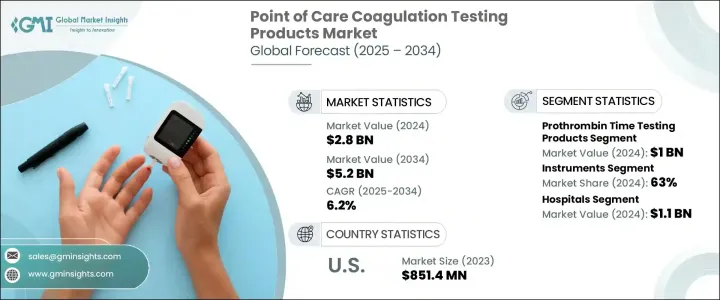

ポイントオブケア凝固検査製品の世界市場規模は2024年に28億米ドルとなり、CAGR 6.2%で成長し、2034年には52億米ドルに達すると予測されています。

これらの革新的な機器は、ベッドサイドや臨床ポイントオブケアで直接リアルタイムの凝固評価を提供し、中央検査室での検査の必要性を排除することで、患者ケアを変革しています。即時かつ信頼性の高い結果への信頼が高まる中、これらの機器は現在、緊急事態、外科的処置、慢性疾患の長期管理において不可欠なものとなっています。市場の成長は、迅速な診断とリアルタイムのモニタリングに対する需要の高まりとともに、心血管疾患と血液疾患の罹患率の増加が牽引しています。ヘルスケアプロバイダーが重要な医学的判断をサポートするためにこうしたツールを利用するようになり、凝固検査製品に対する需要は世界的に高まっています。さらに、医療の分散化モデルや携帯型診断機器へのシフトが、市場の拡大をさらに後押ししています。これらのツールはワークフローを最適化するだけでなく、タイムリーな介入を可能にすることで患者の転帰を向上させる。

市場は活性化凝固時間、dダイマー検査、血小板数、プロトロンビン時間検査、その他のカテゴリーなど、検査の種類によって区分されます。このうち、プロトロンビン時間検査分野がリーダーとして台頭し、2024年には10億米ドルを創出します。2025年から2034年にかけてCAGR 6.3%で成長すると予測されています。このセグメントの優位性は、主に、医師が抗凝固剤の投与量を正確に調整する際に役立つ、迅速で実用的なデータを提供する能力によるものです。凝固モニタリングの遅れが重篤な合併症につながる可能性がある環境では、プロトロンビン時間検査が提供する迅速で信頼性の高い結果は、特に重症患者や長期治療管理における臨床判断に欠かせないものとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 28億米ドル |

| 予測金額 | 52億米ドル |

| CAGR | 6.2% |

製品タイプ別に見ると、市場は器具と消耗品に分かれ、2024年のシェアは器具が63%を占める。このセグメントは、2034年までに33億米ドルを創出すると予想されます。即座に結果を出すことができるため、高圧的な臨床環境における効率性を向上させることができる器具が高く支持されているからです。携帯性に優れ、デジタルヘルスケアシステムとのシームレスな統合が可能なため、救命処置のために迅速な凝固プロファイルが不可欠な病院と外来の両方で不可欠な機器となっています。

米国のポイントオブケア凝固検査製品市場は、2023年に8億5,140万米ドルを創出しました。同地域の市場成長を支えているのは、慢性血液疾患の有病率の上昇とリアルタイム診断ツールに対する需要の高まりです。厳しい規制プロトコールにもかかわらず、米国市場が成長を続けているのは、有利な償還モデルと最新の診断イノベーションの導入に熱心なヘルスケアインフラがあるからです。

Abbott Laboratories、Sysmex Corporation、Thermo Fisher Scientific、Siemens Healthineers、F. Hoffmann-La Rocheなどの大手企業がこの成長の最前線にいます。これらの企業は、ポータブルでユーザーフレンドリーなシステムを迅速な納期で開発することで、絶えず革新を続けています。研究協力への投資、新興市場への進出、クラウドベースの接続性の強化は、市場での存在感を高め、世界的に臨床転帰を改善するための重要な戦略です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性血液疾患の有病率の上昇

- 血液関連疾患を抑制するための政府の取り組みの拡大

- ポイントオブケア検査製品の採用増加

- 技術的進歩

- 業界の潜在的リスク&課題

- 厳格な規制枠組み

- 製品開発コストが高め

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術的情勢

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:テストタイプ別、2021-2034

- 主要動向

- プロトロンビン時間検査製品

- 活性化凝固時間(ACT/APTT)検査製品

- 血小板数

- Dダイマー検査

- その他のテストの種類

第6章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 機器

- 消耗品

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 診断センター

- 在宅ケア環境

- その他の用途

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott Laboratories

- Alere

- A&T Corporation

- Diagnostica Stago Sas

- F. Hoffmann-La Roche

- Genrui Biotech

- Helena Laboratories

- Horiba

- Medtronic

- Nihon Kohden Corporation

- Micropoint Biosciences

- Maccura Biotechnology

- Sysmex Corporation

- Siemens Healthineers

- Thermo Fisher Scientific

The Global Point of Care Coagulation Testing Products Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 6.2% to reach USD 5.2 billion by 2034. These innovative devices are transforming patient care by providing real-time coagulation assessments directly at the bedside or clinical point of care, eliminating the need for central laboratory testing. With a growing reliance on immediate and reliable results, these devices are now integral in emergency situations, surgical procedures, and long-term management of chronic illnesses. The market's growth is driven by the increasing incidence of cardiovascular diseases and blood disorders, alongside the rising demand for rapid diagnoses and real-time monitoring. As healthcare providers turn to these tools to support critical medical decisions, the demand for coagulation testing products is intensifying globally. Moreover, the shift toward decentralized healthcare models and portable diagnostic devices further fuels the market's expansion. These tools not only optimize workflow but also enhance patient outcomes by enabling timely interventions.

The market is segmented based on test types, including activated clotting time, d-dimer tests, platelet count, prothrombin time testing, and other categories. Among these, the prothrombin time testing segment emerged as a leader, generating USD 1 billion in 2024. It is projected to grow at a CAGR of 6.3% between 2025 and 2034. The segment's dominance is primarily due to its ability to provide fast and actionable data that aids physicians in precisely adjusting anticoagulant dosages. In settings where delays in coagulation monitoring can lead to severe complications, the rapid and dependable results offered by prothrombin time tests have become critical in making clinical decisions, particularly in critical care and long-term therapy management.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 6.2% |

In terms of product type, the market divides into instruments and consumables, with instruments holding a 63% share in 2024. This segment is expected to generate USD 3.3 billion by 2034, as instruments are highly favored for their ability to provide immediate results, thereby improving efficiency in high-pressure clinical environments. Their portability and seamless integration with digital healthcare systems make them indispensable in both hospital and outpatient settings, where quick coagulation profiles are essential for life-saving interventions.

The U.S. Point of Care Coagulation Testing Products Market generated USD 851.4 million in 2023. The market's growth in the region is supported by the rising prevalence of chronic hematologic conditions, coupled with a growing demand for real-time diagnostic tools. Despite stringent regulatory protocols, the U.S. market continues to thrive due to favorable reimbursement models and a healthcare infrastructure that is eager to embrace the latest diagnostic innovations.

Leading players such as Abbott Laboratories, Sysmex Corporation, Thermo Fisher Scientific, Siemens Healthineers, F. Hoffmann-La Roche, and others are at the forefront of this growth. These companies are continuously innovating by developing portable, user-friendly systems with rapid turnaround times. Their investment in research collaborations, expansion into emerging markets, and enhancement of cloud-based connectivity are key strategies to increase market presence and improve clinical outcomes globally.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic blood disorders

- 3.2.1.2 Growing government initiatives to curb blood-related diseases

- 3.2.1.3 Increasing adoption of point of care testing products

- 3.2.1.4 Technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory framework

- 3.2.2.2 High cost of product development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Prothrombin time testing products

- 5.3 Activated clotting time (ACT/APTT) testing products

- 5.4 Platelet count

- 5.5 D-dimer test

- 5.6 Others test types

Chapter 6 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Instruments

- 6.3 Consumables

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Diagnostic centers

- 7.4 Home care settings

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Alere

- 9.3 A&T Corporation

- 9.4 Diagnostica Stago Sas

- 9.5 F. Hoffmann-La Roche

- 9.6 Genrui Biotech

- 9.7 Helena Laboratories

- 9.8 Horiba

- 9.9 Medtronic

- 9.10 Nihon Kohden Corporation

- 9.11 Micropoint Biosciences

- 9.12 Maccura Biotechnology

- 9.13 Sysmex Corporation

- 9.14 Siemens Healthineers

- 9.15 Thermo Fisher Scientific