|

市場調査レポート

商品コード

1844354

迅速診断市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Rapid Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 迅速診断市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年09月30日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

概要

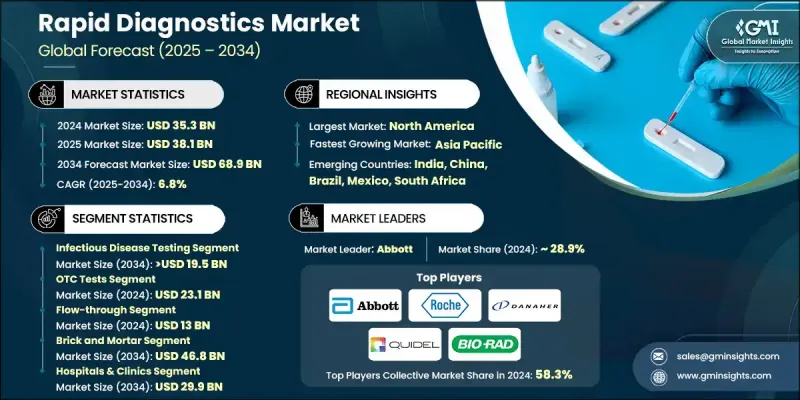

世界の迅速診断市場は、2024年には353億米ドルとなり、CAGR 6.8%で成長し、2034年には689億米ドルに達すると推定されます。

市場は、感染症数の増加、ポイントオブケア検査の普及、診断技術の継続的な革新、ヘルスケアインフラのアップグレードを目的とした投資の着実な増加など、いくつかの要因によって拡大しています。迅速診断検査は、数分から数時間以内に正確な結果が得られるように設計されており、早期発見と迅速な医療対応のための重要なツールとなっています。これらの検査は、クリニック、家庭、薬局などで広く利用され、リアルタイムのヘルスケア判断をサポートしています。分子診断、イムノアッセイ、ラテラル・フロー・アッセイなど、さまざまなプラットフォームを使って、タイムリーで信頼できる結果を提供します。バイオセンサー、マイクロ流体技術、AIベースの診断ツールの進歩により、スピード、精度、有用性がさらに向上しています。市場の成長は、デジタルヘルスシステムとのより広範な統合、診断効率の向上、感染モニタリング以外の用途の拡大によっても支えられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 353億米ドル |

| 予測金額 | 689億米ドル |

| CAGR | 6.8% |

2024年の感染症検査分野のシェアは25.2%でした。肝炎、HIV、結核、マラリア、インフルエンザなどの疾病の早期かつ迅速な発見に対する需要が世界的に引き続き高いことから、この分野がリードしています。世界的な健康リスクの増大と感染率の上昇に伴い、早期診断が最優先課題となっています。迅速検査は、これらの疾病を迅速に特定し、より迅速な治療開始を可能にし、全体的な死亡率の減少に貢献するという重要な役割を果たしています。

2024年、市販(OTC)診断薬セグメントは231億米ドルを生み出し、2034年までCAGR 7.1%で成長すると予想されています。消費者はますます個人の健康管理を優先するようになっており、それが自己検査キットの需要を促進しています。デジタルヘルスリソースへのアクセスが容易になり、家庭用診断を促進するマーケティング活動により、OTCキットの使用に対する信頼が大幅に高まっています。人々は、グルコース値、妊娠、感染症などの健康状態を日常的にモニタリングするために、こうしたツールを受け入れています。

米国の迅速診断市場は2024年に168億米ドルを創出しました。この成長を支えているのは、北米全域に強固なヘルスケアインフラ、高度な検査室、幅広い病院ネットワークが存在することです。これらの要因によって、最先端の診断技術が急速に採用されるための強固な基盤が構築されています。効率的な検査室システムも診断ツールの迅速な展開と拡張を可能にし、同地域における迅速検査の強力な普及に寄与しています。

世界の競合情勢を形成している注目すべき企業には、Trinity Biotech、Abbott、Quidel、Thermo Fisher Scientific、Roche、Sight Diagnostics、ACON、BIOMERIEUX、Alfa Scientific、Meridian Bioscience、Becton、Dickinson and Company(BD)、QIAGEN、Artron、Hologic、BIO-RAD、Danaherなどがあります。迅速診断業界の企業は、より強固な地位を得るために、技術革新とグローバル展開に焦点を当てた積極的な戦略を追求しています。その多くは、高精度で迅速、かつユーザーフレンドリーな検査キットを開発するための研究開発に多額の投資を行っています。ヘルスケアプロバイダーや流通パートナーとの戦略的提携により、これらの企業は新興市場への進出を果たしています。さらに、検査結果の解釈や管理を強化するため、デジタル統合やAI主導型プラットフォームの採用も進んでいます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 感染症の蔓延の増加

- 技術的進歩

- 迅速診断検査の人気の高まり

- 早期診断に関する人々の意識の高まり

- 感染症の診断に対する政府の取り組みの強化

- 業界の潜在的リスク&課題

- 結果の精度が低い

- 代替製品の入手可能性

- 厳格な規制枠組み

- 市場機会

- 新興市場および分散型ケア施設への拡大

- 遠隔医療とデジタルレポートとの統合

- 促進要因

- 成長可能性分析

- 払い戻しシナリオ

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- テクノロジーの情勢

- 現在の技術動向

- 新興技術

- ギャップ分析

- ポーターの分析

- PESTEL分析

- バリューチェーン分析

- 将来の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- グローバル

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ・中東・アフリカ

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 感染症検査

- 呼吸器感染症検査製品

- インフルエンザ

- 肝炎

- HIV

- その他の感染症検査

- 妊娠と生殖能力の検査

- 血液検査製品

- 血糖モニタリング

- 薬物乱用(DoA)検査製品

- 心臓代謝検査

- 凝固検査製品

- コレステロール検査製品

- 尿検査製品

- 腫瘍/がんマーカー検査製品

- 便潜血検査製品

- その他の製品

第6章 市場推計・予測:購入別、2021-2034

- 主要動向

- 市販の検査薬

- 処方箋に基づく検査

第7章 市場推計・予測:テクノロジー/プラットフォーム別、2021-2034

- 主要動向

- フロースルー

- 固相

- ラテラルフロー

- 凝集反応試験

- その他のテクノロジー/プラットフォーム

第8章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 店舗

- eコマース

第9章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院と診療所

- 診断センター

- 在宅ケアの設定

- その他の用途

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Abbott

- ACON

- Alfa Scientific

- Artron

- Becton, Dickinson and Company(BD)

- BIOMERIEUX

- BIO-RAD

- Danaher

- HOLOGIC

- Meridian Bioscience

- QIAGEN

- Quidel

- Roche

- Sight Diagnostics

- Thermo Fisher Scientific

- Trinity Biotech