|

市場調査レポート

商品コード

1721496

ガスタービン部品市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測Gas Turbine Component Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ガスタービン部品市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月10日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

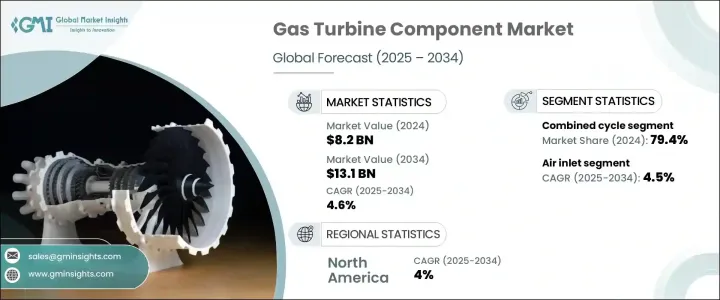

ガスタービン部品の世界市場規模は、2024年に82億米ドルとなり、CAGR 4.6%で成長し、2034年には131億米ドルに達すると推定されます。

この成長の主な要因は、低排出技術へのシフトであり、特にピーカープラントやコンバインドサイクルシステムにおいて効率的なタービン部品の需要が増加しています。産業部門や公益事業部門における既存のガスタービン・インフラの近代化と改修は、先進部品の採用を促進し、タービンの効率と性能を高めると予想されます。燃焼器、ノズル、ブレードを中心とした材料と設計の継続的な革新は、タービン全体の性能を向上させると同時に、進化する排出基準を満たす上で重要な役割を果たしています。世界がよりクリーンで柔軟な発電をますます優先するようになるにつれ、ガスタービン部品はエネルギーインフラの近代化に不可欠なものとなっています。

高性能タービン部品の需要は、単結晶ブレードや耐熱合金のニーズが高まり続けている航空宇宙産業による進歩によってさらに強化されています。特に遠隔地や非電化地域での分散型エネルギーシステムやバックアップ電源ソリューションの重要性が高まっていることも、信頼性の高いタービン部品の必要性を高めています。多くの場合、再生可能エネルギー源と統合されるこれらのシステムは、最新のハイブリッド電力インフラの開発に不可欠です。エネルギー生産者が環境と運用の両方の要求を満たそうとするにつれ、高品質のタービン部品の重要性は増し、より広範なエネルギー移行に不可欠なものとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 82億米ドル |

| 予測金額 | 131億米ドル |

| CAGR | 4.6% |

エアインレットコンポーネント分野は、粉塵、湿気、工業汚染物質などの環境汚染物質からタービンを保護するという重要な役割を担っているため、2034年までCAGR 4.5%で成長すると予想されます。これらの部品は、タービンの完全性を維持し、燃焼効率を向上させ、メンテナンスの必要性を減らし、最終的に運転コストを削減する上で極めて重要です。先進国市場と新興国市場の両方で、特にクリーンエネルギーの移行に重点を置く地域で天然ガスインフラが拡大するにつれて、進化するエネルギー情勢を支える信頼性の高いろ過システムの需要が高まっています。

オープンサイクルタービンコンポーネント分野は、燃料の柔軟性と排出ガス制御の革新に牽引され、2034年までCAGR 4%で成長すると予測されます。これらのシステムは柔軟性があり、厳しい二酸化炭素削減規制を遵守しながら、再生可能エネルギー投入によるハイブリッド・アプリケーションをサポートすることができます。オープンサイクルのタービンは、断続的な再生可能エネルギー源のバランスを取る上で重要な役割を果たし続けており、大規模な公益事業プロジェクトに不可欠です。クリーンエネルギーを支援する各国政府の政策は、進化するエネルギー・ミックスにおけるこれらのシステムの関連性をさらに高めています。

2024年、米国のガスタービン部品市場は5億7,690万米ドルを創出し、よりクリーンで効率的なガスタービン技術への移行が進んでいます。ガスタービンは、太陽光や風力などの再生可能エネルギー源とシームレスに統合しながら、グリッドの安定性を確保し、需要の変化に迅速に対応する能力で好まれています。

世界ガスタービン部品市場の主要企業は、MAN Energy Solutions、Solar Turbines、Ansaldo Energia、Woodward、Rolls-Royce、三菱電機、Suzler、Parker Hannifin、IHI Corporation、GE Vernova、Baker Hughes、Siemens Energy、MTU Aero Engines、Wartsila、Doncasters Group、Chromalloy Gas Turbine、Doosan、川崎重工業、Precision Castparts、Bharat Heavy Electricals Limitedなどです。市場の主導権を維持するため、これらの企業は先進合金、冷却技術、積層造形ソリューションの開発に注力し、タービンの耐久性と運転効率を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- トランプ政権の関税が貿易と産業全体に与える影響

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:コンポーネントタイプ別、2021-2034

- 主要動向

- 空気入口

- コンプレッサー

- 燃焼器

- タービン

- 燃料ノズル

- 排気

- 補助システム

- その他

第6章 市場規模・予測:技術別、2021-2034

- 主要動向

- オープンサイクル

- 複合サイクル

第7章 市場規模・予測:製品別、2021-2034

- 主要動向

- 航空機派生型

- ヘビーデューティー

第8章 市場規模・予測:用途別、2021-2034

- 主要動向

- 発電所

- 石油・ガス

- プロセスプラント

- 航空

- 海洋

- その他

第9章 市場規模・予測:サービスプロバイダー別、2021-2034

- 主要動向

- OEM

- 非OEM

第10章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- オランダ

- ギリシャ

- ポーランド

- アジア太平洋地域

- 中国

- オーストラリア

- 日本

- 韓国

- インドネシア

- タイ

- マレーシア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- オマーン

- エジプト

- トルコ

- バーレーン

- イラク

- 南アフリカ

- アルジェリア

- ラテンアメリカ

- ブラジル

- アルゼンチン

- ペルー

第11章 企業プロファイル

- Ansaldo Energia

- Baker Hughes

- Bharat Heavy Electricals Limited(BHEL)

- Chromalloy Gas Turbine LLC

- Doncasters Group

- Doosan

- GE Vernova

- IHI Corporation

- Kawasaki Heavy Industries

- MAN Energy Solutions

- Mitsubishi Power

- MTU Aero Engines

- Parker Hannifin

- Precision Castparts

- Rolls-Royce

- Siemens Energy

- Solar Turbines

- Sulzer

- Wartsila

- Woodward

The Global Gas Turbine Component Market was valued at USD 8.2 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 13.1 billion by 2034. This growth is primarily fueled by the shift toward lower-emission technologies, increasing the demand for efficient turbine components, particularly in peaker plants and combined-cycle systems. The modernization and retrofitting of existing gas turbine infrastructure across industrial and utility sectors are expected to drive the adoption of advanced parts, enhancing turbine efficiency and performance. The continued innovation in materials and design, specifically in combustors, nozzles, and blades, plays a critical role in meeting evolving emission standards, while also improving overall turbine performance. As the world increasingly prioritizes cleaner, more flexible power generation, gas turbine components are becoming integral to the modernization of energy infrastructure.

The demand for high-performance turbine components is further strengthened by advancements driven by the aerospace industry, where the need for single-crystal blades and heat-resistant alloys continues to rise. The increasing importance of decentralized energy systems and backup power solutions, particularly in remote or off-grid locations, also fuels the need for reliable turbine components. These systems, often integrated with renewable energy sources, are vital to the development of modern hybrid power infrastructure. As energy producers seek to meet both environmental and operational demands, the importance of high-quality turbine components grows, making them essential to the broader energy transition.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.2 Billion |

| Forecast Value | $13.1 Billion |

| CAGR | 4.6% |

The air inlet component segment is expected to grow at a CAGR of 4.5% through 2034, owing to its vital role in safeguarding turbines from environmental contaminants such as dust, moisture, and industrial pollutants. These components are crucial in preserving turbine integrity, improving combustion efficiency, and reducing maintenance needs, ultimately lowering operational costs. As natural gas infrastructure expands in both developed and emerging markets, particularly in areas focused on clean energy transitions, reliable filtration systems are in high demand to support the evolving energy landscape.

The open-cycle turbine component segment is projected to grow at a CAGR of 4% through 2034, driven by innovations in fuel flexibility and emissions control. These systems offer flexibility, enabling them to support hybrid applications with renewable inputs while complying with stringent carbon reduction regulations. Open-cycle turbines continue to play a significant role in balancing intermittent renewable energy sources, making them vital to large-scale utility projects. Governments' policies supporting clean energy further enhance the relevance of these systems in the evolving energy mix.

In 2024, the U.S. Gas Turbine Component Market generated USD 576.9 million, fueled by the country's ongoing transition to cleaner, more efficient gas turbine technologies. Gas turbines are preferred for their ability to rapidly respond to demand changes, ensuring grid stability while integrating seamlessly with renewable energy sources like solar and wind.

Key players in the Global Gas Turbine Component Market include MAN Energy Solutions, Solar Turbines, Ansaldo Energia, Woodward, Rolls-Royce, Mitsubishi Power, Suzler, Parker Hannifin, IHI Corporation, GE Vernova, Baker Hughes, Siemens Energy, MTU Aero Engines, Wartsila, Doncasters Group, Chromalloy Gas Turbine, Doosan, Kawasaki Heavy Industries, Precision Castparts, and Bharat Heavy Electricals Limited. To maintain market leadership, these companies focus on developing advanced alloys, cooling technologies, and additive manufacturing solutions, boosting turbine durability and operational efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Impact of trump administration tariffs on trade & overall industry

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Component Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Air inlet

- 5.3 Compressor

- 5.4 Combustor

- 5.5 Turbine

- 5.6 Fuel nozzle

- 5.7 Exhaust

- 5.8 Auxiliary systems

- 5.9 Others

Chapter 6 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Open cycle

- 6.3 Combined cycle

Chapter 7 Market Size and Forecast, By Product, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Aero-derivative

- 7.3 Heavy duty

Chapter 8 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Power plant

- 8.3 Oil & gas

- 8.4 Process plant

- 8.5 Aviation

- 8.6 Marine

- 8.7 Others

Chapter 9 Market Size and Forecast, By Service Provider, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Non-OEM

Chapter 10 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 France

- 10.3.3 Germany

- 10.3.4 Russia

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.3.7 Greece

- 10.3.8 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Australia

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Indonesia

- 10.4.6 Thailand

- 10.4.7 Malaysia

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Qatar

- 10.5.4 Oman

- 10.5.5 Egypt

- 10.5.6 Turkey

- 10.5.7 Bahrain

- 10.5.8 Iraq

- 10.5.9 South Africa

- 10.5.10 Algeria

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

- 10.6.3 Peru

Chapter 11 Company Profiles

- 11.1 Ansaldo Energia

- 11.2 Baker Hughes

- 11.3 Bharat Heavy Electricals Limited (BHEL)

- 11.4 Chromalloy Gas Turbine LLC

- 11.5 Doncasters Group

- 11.6 Doosan

- 11.7 GE Vernova

- 11.8 IHI Corporation

- 11.9 Kawasaki Heavy Industries

- 11.10 MAN Energy Solutions

- 11.11 Mitsubishi Power

- 11.12 MTU Aero Engines

- 11.13 Parker Hannifin

- 11.14 Precision Castparts

- 11.15 Rolls-Royce

- 11.16 Siemens Energy

- 11.17 Solar Turbines

- 11.18 Sulzer

- 11.19 Wartsila

- 11.20 Woodward