|

市場調査レポート

商品コード

1721488

眼アレルギー治療薬の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Eye Allergy Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 眼アレルギー治療薬の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月11日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

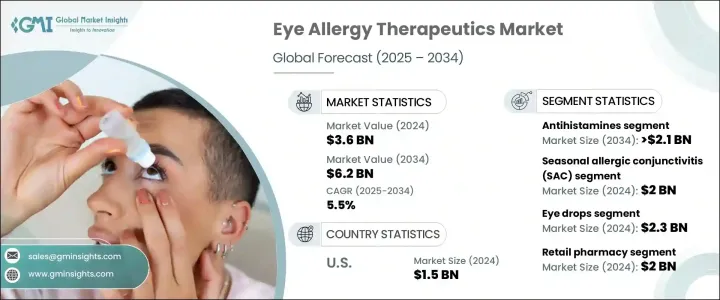

眼アレルギー治療薬の世界市場規模は、2024年に36億米ドルとなり、CAGR 5.5%で成長し、2034年には62億米ドルに達すると予測されています。

世界が大気汚染レベルの上昇と気候変動の影響に直面し続ける中、アレルギー性結膜炎のような眼アレルギーの症例がますます多くなっています。都市化の進展に加え、花粉、ペットのフケ、ダニといった屋内外のアレルゲンにさらされる機会が増え、より効果的で便利な治療法に対する需要が急増しています。人々はエアコンや人工換気された空間で過ごす時間が増え、環境誘因に対する感受性も高まっています。迅速かつ安全で、利用しやすい治療を積極的に求める消費者が増えており、眼アレルギー治療薬の世界市場は着実な成長を遂げています。ドラッグデリバリーシステムの技術的進歩と患者に優しい製剤の重視が競合情勢を大きく変えています。また、個別化医療や標的療法へのシフトは、製薬会社がより早く、より長期の救済を提供する革新的なソリューションを提供する新たな機会を開いています。

製薬メーカーは、副作用を最小限に抑えた先進的な製剤を導入するため、研究開発を強化しています。処方薬と一般用医薬品(OTC)の両方が利用できるようになったことで、治療へのアクセスが広がり、消費者は頻繁に臨床を訪れることなく症状を管理しやすくなりました。米国食品医薬品局(FDA)のような規制当局は、新薬やデリバリー・メカニズムを承認することで、この成長において極めて重要な役割を果たしています。薬剤溶出性コンタクトレンズやデュアルアクションドロップのような製品は、治療の選択肢を広げ、患者のコンプライアンスを向上させています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 36億米ドル |

| 予測金額 | 62億米ドル |

| CAGR | 5.5% |

市場は薬剤クラス別に肥満細胞安定剤、抗ヒスタミン剤、二重作用薬、鬱血除去剤、コルチコステロイド、免疫療法、その他に区分されます。このうち、抗ヒスタミン薬が主要な促進要因となり、CAGR 5.4%で成長し、2034年までに21億米ドルに達すると予測されています。抗ヒスタミン薬は、かゆみ、発赤、流涙などの症状を迅速に緩和するため、ヘルスケアプロバイダーと患者の両方にとって最適な選択肢となっています。抗ヒスタミン剤は、処方箋とOTCの両方のチャネルを通じて簡単に入手できるため、目のアレルギーに悩む患者にとって広く信頼されるソリューションとなっています。

季節性アレルギー性結膜炎(SAC)分野は依然として主要な収益源であり、2024年には20億米ドルを生み出します。SACの症例は、花粉飛散量がピークに達する春と夏に急増し、特に汚染度の高い都市環境では顕著です。消費者は、認知度と利便性を促進する積極的な消費者直結型マーケティング・キャンペーンの影響を受けて、ますますOTC治療薬に目を向けるようになっています。

米国眼アレルギー治療薬市場は2024年に15億米ドルに達し、強力な規制監督とFDAによる新規治療法の承認に支えられて成長を続けています。小売チェーンや薬局で簡単にOTC医薬品が入手できるようになったことで、何百万人もの米国人が治療薬を入手しやすくなりました。

市場をリードする企業には、ボシュ・ヘルス、アッヴィ、ヒクマ・ファーマシューティカルズ、ファイザー、テバ・ファーマシューティカル・インダストリーズ、リジェネロン・ファーマシューティカルズ、サノフィ、マイラン、アルコン、ノバルティス、ジョンソン・エンド・ジョンソン、エイコーン、ニコックス、参天製薬、サンファーマシューティカル・インダストリーズなどがあります。これらの企業は、製品の革新、ユーザーフレンドリーなソリューション、より広範な販売パートナーシップを優先しています。自己投与療法、次世代コンタクトレンズ、戦略的小売提携への投資により、業界大手は消費者との関わりを強化し、世界市場での存在感を強めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 汚染と気候変動によるアレルギー性結膜炎の有病率の上昇

- より高い効果を得るための併用療法の採用増加

- 市販のアレルギー用点眼薬の成長

- ドラッグデリバリーシステムの進歩

- 業界の潜在的リスク&課題

- 長期にわたる薬の使用による副作用

- 低価格のジェネリック医薬品やOTC代替品の入手可能性

- 促進要因

- 成長可能性分析

- 規制情勢

- パイプライン分析

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:薬剤クラス別、2021-2034

- 主要動向

- 抗ヒスタミン薬

- 肥満細胞安定剤

- 二重作用剤

- コルチコステロイド

- 鼻づまり解消薬

- 免疫療法

- その他の薬物クラス

第6章 市場推計・予測:アレルギーの種類別、2021-2034

- 主要動向

- 季節性アレルギー性結膜炎(SAC)

- 通年性アレルギー性結膜炎(PAC)

- 春季カタル(VKC)

- アトピー性角結膜炎(AKC)

- 巨大乳頭結膜炎(GPC)

第7章 市場推計・予測:剤形別、2021-2034

- 主要動向

- 目薬

- 注射剤

- 経口錠剤/カプセル

- ジェルと軟膏

第8章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 病院薬局

- 小売薬局

- eコマース

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AbbVie

- Akorn

- Alcon

- Bausch Health

- Hikma Pharmaceuticals

- Johnson &Johnson

- Mylan

- Nicox

- Novartis

- Pfizer

- Regeneron Pharmaceuticals

- Sanofi

- Santen Pharmaceutical

- Sun Pharmaceutical Industries

- Teva Pharmaceutical Industries

The Global Eye Allergy Therapeutics Market was valued at USD 3.6 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 6.2 billion by 2034. As the world continues to face rising levels of air pollution and the impact of climate change, cases of eye allergies such as allergic conjunctivitis are becoming increasingly common. Growing urbanization, along with extended exposure to indoor and outdoor allergens like pollen, pet dander, and dust mites, is triggering a spike in demand for more effective and convenient treatments. People are spending more time in air-conditioned and artificially ventilated spaces, which has also increased their sensitivity to environmental triggers. With more consumers actively seeking quick, safe, and accessible treatments, the global market for eye allergy therapeutics is witnessing steady growth. Technological advancements in drug delivery systems and a greater emphasis on patient-friendly formulations are reshaping the competitive landscape. The shift toward personalized medicine and targeted therapies is also opening up new opportunities for pharmaceutical companies to deliver innovative solutions that offer faster and longer-lasting relief.

Pharmaceutical manufacturers are ramping up research and development efforts to introduce advanced formulations with minimal side effects. The availability of both prescription and over-the-counter (OTC) products has broadened treatment access, making it easier for consumers to manage symptoms without frequent clinical visits. Regulatory authorities like the U.S. Food and Drug Administration (FDA) are playing a pivotal role in this growth by approving new drugs and delivery mechanisms. Products like drug-eluting contact lenses and dual-action drops are expanding therapeutic options and improving patient compliance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $6.2 Billion |

| CAGR | 5.5% |

The market is segmented by drug class into mast cell stabilizers, antihistamines, dual-action agents, decongestants, corticosteroids, immunotherapy, and others. Among these, antihistamines are anticipated to be the primary growth driver, projected to grow at a CAGR of 5.4% and reach USD 2.1 billion by 2034. These medications offer rapid relief from symptoms such as itching, redness, and tearing, making them the go-to choice for both healthcare providers and patients. With easy availability through both prescription and OTC channels, antihistamines have become a widely trusted solution for eye allergy sufferers.

The seasonal allergic conjunctivitis (SAC) segment remains a major revenue generator, producing USD 2 billion in 2024. SAC cases surge in spring and summer when pollen levels peak, particularly in highly polluted urban environments. Consumers are increasingly turning to OTC remedies, influenced by aggressive direct-to-consumer marketing campaigns that promote awareness and convenience.

The U.S. Eye Allergy Therapeutics Market reached USD 1.5 billion in 2024 and continues to grow, supported by strong regulatory oversight and the FDA's approval of novel therapies. Easy OTC availability in retail chains and pharmacies has streamlined access to treatments for millions of Americans.

Leading market players include Bausch Health, AbbVie, Hikma Pharmaceuticals, Pfizer, Teva Pharmaceutical Industries, Regeneron Pharmaceuticals, Sanofi, Mylan, Alcon, Novartis, Johnson & Johnson, Akorn, Nicox, Santen Pharmaceutical, and Sun Pharmaceutical Industries. These companies are prioritizing product innovation, user-friendly solutions, and broader distribution partnerships. With investments in self-administered therapies, next-gen contact lenses, and strategic retail alliances, industry leaders are enhancing consumer engagement and strengthening their presence across the global market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of allergic conjunctivitis due to pollution and climate change

- 3.2.1.2 Increasing adoption of combination therapies for better efficacy

- 3.2.1.3 Growth in OTC allergy eye drops

- 3.2.1.4 Advancements in drug delivery systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects of long-term medication use

- 3.2.2.2 Availability of low-cost generics and OTC alternatives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Antihistamines

- 5.3 Mast cell stabilizers

- 5.4 Dual-action agents

- 5.5 Corticosteroids

- 5.6 Decongestants

- 5.7 Immunotherapy

- 5.8 Other drug classes

Chapter 6 Market Estimates and Forecast, By Allergy Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Seasonal allergic conjunctivitis (SAC)

- 6.3 Perennial allergic conjunctivitis (PAC)

- 6.4 Vernal keratoconjunctivitis (VKC)

- 6.5 Atopic keratoconjunctivitis (AKC)

- 6.6 Giant papillary conjunctivitis (GPC)

Chapter 7 Market Estimates and Forecast, By Dosage Form, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Eye drops

- 7.3 Injectables

- 7.4 Oral tablets/capsules

- 7.5 Gels and ointments

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacy

- 8.3 Retail pharmacy

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Akorn

- 10.3 Alcon

- 10.4 Bausch Health

- 10.5 Hikma Pharmaceuticals

- 10.6 Johnson & Johnson

- 10.7 Mylan

- 10.8 Nicox

- 10.9 Novartis

- 10.10 Pfizer

- 10.11 Regeneron Pharmaceuticals

- 10.12 Sanofi

- 10.13 Santen Pharmaceutical

- 10.14 Sun Pharmaceutical Industries

- 10.15 Teva Pharmaceutical Industries