|

市場調査レポート

商品コード

1721478

段ボールファンフォールド包装の市場機会、成長促進要因、業界動向分析、2025年~2034年予測Corrugated Fanfold Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 段ボールファンフォールド包装の市場機会、成長促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年04月09日

発行: Global Market Insights Inc.

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

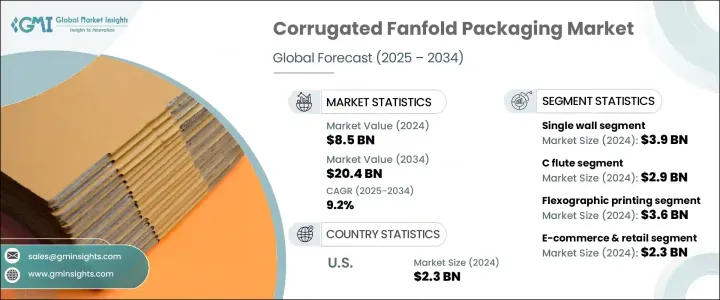

世界の段ボールファンフォールド包装市場は、2024年には85億米ドルと評価され、CAGR 9.2%で成長し、2034年には204億米ドルに達すると推定されています。

この急増は、eコマースの急速な増加、消費者の購買パターンのダイナミックなシフト、持続可能でコスト効率の高いパッケージング・ソリューションへの業界全体の軸足によるところが大きいです。オンライン小売が世界的に拡大するにつれ、よりスマートで柔軟な包装形態への需要が急速に高まっています。あらゆる分野の企業が、業務の合理化、廃棄物の削減、配送コストの削減を実現する適切なサイズの包装を可能にするソリューションを優先しています。段ボールファンフォールド包装は、オペレーションの俊敏性と持続可能性を重視する企業にとって、急速に好ましい選択肢となりつつあります。ファンフォールドフォーマットは、自動化とカスタマイズをサポートする一方で、あらかじめ形成された複数のサイズの箱をストックする必要性をなくします。これにより、保管スペースが大幅に削減され、様々な注文量に合わせたパッケージングが可能になります。消費者の環境意識と、企業に対する二酸化炭素排出量削減の規制圧力は、リサイクル可能で軽量なファンフォールド・ソリューションの採用をさらに加速させています。

技術の進歩とスマート・パッケージング・ソリューションの普及に伴い、メーカーはファンフォールド・パッケージングとシームレスに統合する自動化ツールやオンデマンド製函システムに投資しています。これらの技術革新は、包装効率を向上させるだけでなく、余分な材料の使用を最小限に抑え、物流コストを削減します。さらに、食品配送、エレクトロニクス、ファッションなどの分野からの環境に優しいパッケージングへの需要の高まりが、世界市場全体におけるファンフォールドパッケージングへの持続的な関心を煽っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 85億米ドル |

| 予測金額 | 204億米ドル |

| CAGR | 9.2% |

壁の種類別では、シングルウォールファンフォールドボードセグメントが2024年に39億米ドルを生み出しました。このセグメントは、軽量設計と費用対効果で人気があり、eコマース小売業者やサブスクリプション型サービスの有力な選択肢となっています。特に化粧品、ファッション、食品などの消費者カテゴリーでオンライン購入が増加し続けているため、シングルウォールファンフォールドボードは強度と手頃な価格のバランスが取れた信頼性の高いソリューションを提供しています。食品宅配プラットフォームの継続的な拡大も、持続可能で、さまざまな注文サイズに対応し、廃棄物の削減と配送効率の最適化に貢献するパッケージへの需要を後押ししています。

Cフルートはフルートタイプの中で最大のシェアを占め、2024年には29億米ドルを生み出します。耐久性と耐衝撃性を維持しながら適度な重量を支える能力は、幅広い用途に理想的です。このフルートタイプは、ボトル入り飲料、缶詰、ミールキットなどの飲食品に広く使用されています。その構造的完全性により、安全な輸送が保証されるため、パッケージングにおける性能と持続可能性の両方を高めたい企業にとって好ましい選択肢となっています。

ドイツ段ボールファンフォールド包装2024年の市場規模は4億8,110万米ドル。電子機器、消費財、食品の主要輸出国としての確固たる地位が、カスタムメイドで耐久性のあるパッケージング需要を引き続き牽引しています。ドイツの産業および自動車セクターの成長は、二重および三重壁ファンフォールドボードのニーズをさらに高めています。また、企業はEUの持続可能性指令に沿うよう圧力を強めており、リサイクル可能でバイオベースの代替パッケージの普及を促しています。

段ボールファンフォールド包装の世界市場における主要企業には、Smurfit Kappa Group、Ribble Packaging、Papierfabrik Palm、Stora Enso、Hinojosa Packaging Group、Kite Packaging、Abbe、DS Smith、International Paper Company、Rondo Ganahl、Papeles y Conversiones de Mexico、Corrugated Supplies Company、Mondiなどがあります。これらの企業は、自動化技術に積極的に投資し、電子機器や医薬品などのニッチ産業に対応する製品ポートフォリオを拡大し、FSC認証やリサイクル可能な包装資材を通じてグリーン・イニシアティブに取り組んでいます。eコマース・プラットフォームやロジスティクス・プロバイダーとの戦略的提携により、包装業務の迅速化や配送納期の改善も実現しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- eコマースとオンラインショッピングの台頭

- カスタマイズとパーソナライゼーションの需要の高まり

- 自動化とスマートパッケージングソリューションの増加

- 食品・飲料業界の拡大

- デジタル印刷技術の進歩

- 業界の潜在的リスク&課題

- 自動包装システムへの高額な初期投資

- リサイクルと廃棄物管理の課題

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:壁の種類別、2021 –2034

- 主要動向

- シングルウォール

- 二重壁

- トリプルウォール

第6章 市場推計・予測:フルートの種類別、2021 –2034

- 主要動向

- Bフルート

- Cフルート

- Eフルート

- その他

第7章 市場推計・予測:印刷技術別、2021 –2034

- 主要動向

- フレキソ印刷

- デジタル印刷

- 石版印刷

第8章 市場推計・予測:用途別、2021 –2034

- 主要動向

- eコマースと小売

- 家電

- ヘルスケアと医薬品

- パーソナルケア&化粧品

- 自動車および工業製品

- 食品・飲料

第9章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Abbe

- Corrugated Supplies Company

- DS Smith

- Hinojosa Packaging Group

- International Paper Company

- Kite Packaging

- Mondi

- Papeles y Conversiones de Mexico

- Papierfabrik Palm

- Ribble Packaging

- Rondo Ganahl

- Smurfit Kappa Group

- Stora Enso

- WestRock

The Global Corrugated Fanfold Packaging Market was valued at USD 8.5 billion in 2024 and is estimated to grow at a CAGR of 9.2% to reach USD 20.4 billion by 2034. This surge is largely attributed to the rapid rise in e-commerce, dynamic shifts in consumer purchasing patterns, and an industry-wide pivot toward sustainable and cost-efficient packaging solutions. As online retail expands globally, the demand for smarter, more flexible packaging formats is growing rapidly. Businesses across sectors are prioritizing solutions that enable right-sized packaging to streamline operations, reduce waste, and lower shipping costs. Corrugated fanfold packaging is fast becoming a preferred choice for enterprises focused on operational agility and sustainability. The fanfold format supports automation and customization while eliminating the need for stocking multiple pre-formed box sizes. This significantly reduces storage space and allows companies to tailor packaging for varying order volumes. Environmental consciousness among consumers and regulatory pressure on businesses to cut down on their carbon footprint has further accelerated the adoption of recyclable, lightweight fanfold solutions.

With technological advancement and smart packaging solutions gaining traction, manufacturers are investing in automation tools and on-demand box-making systems that seamlessly integrate with fanfold packaging. These innovations not only improve packaging efficiency but also minimize excess material use and drive down logistics costs. Moreover, the increasing demand for eco-friendly packaging from sectors like food delivery, electronics, and fashion is fueling sustained interest in fanfold packaging across global markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.5 Billion |

| Forecast Value | $20.4 Billion |

| CAGR | 9.2% |

Among wall types, the single wall fanfold boards segment generated USD 3.9 billion in 2024. This segment is popular for its lightweight design and cost-effectiveness, making it the go-to option for e-commerce retailers and subscription-based services. As online purchasing continues to rise-especially for consumer categories like cosmetics, fashion, and food-single wall fanfold boards offer a reliable solution that balances strength with affordability. The continued expansion of food delivery platforms is also fueling demand for packaging that is both sustainable and tailored to different order sizes, helping reduce waste and optimize delivery efficiency.

C flute held the largest share among flute types, generating USD 2.9 billion in 2024. Its ability to support moderate weight while maintaining durability and impact resistance makes it ideal for a wide range of applications. This flute type is widely used for packaged food and beverage items such as bottled drinks, canned goods, and meal kits. Its structural integrity ensures safe transport, making it a preferred option for companies looking to enhance both performance and sustainability in packaging.

Germany Corrugated Fanfold Packaging Market generated USD 481.1 million in 2024. The country's strong position as a major exporter of electronics, consumer goods, and food products continues to drive demand for custom and durable packaging. Growth in Germany's industrial and automotive sectors further boosts the need for double and triple-wall fanfold boards. Businesses are also under increasing pressure to align with EU sustainability directives, encouraging widespread adoption of recyclable and bio-based packaging alternatives.

Key players in the Global Corrugated Fanfold Packaging Market include Smurfit Kappa Group, Ribble Packaging, Papierfabrik Palm, Stora Enso, Hinojosa Packaging Group, Kite Packaging, Abbe, DS Smith, International Paper Company, Rondo Ganahl, Papeles y Conversiones de Mexico, Corrugated Supplies Company, and Mondi. These companies are actively investing in automation technologies, expanding product portfolios to cater to niche industries such as electronics and pharmaceuticals, and aligning with green initiatives through FSC-certified and recyclable packaging materials. Strategic collaborations with e-commerce platforms and logistics providers are also enabling faster packaging operations and improved delivery turnaround.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise of e-commerce and online shopping

- 3.2.1.2 Growing demand for customization and personalization

- 3.2.1.3 Rise in automation and smart packaging solutions

- 3.2.1.4 Expansion in the food and beverage industry

- 3.2.1.5 Advancements in digital printing technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment in automated packaging systems

- 3.2.2.2 Recycling and waste management challenges

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Wall Type, 2021 – 2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Single wall

- 5.3 Double wall

- 5.4 Triple wall

Chapter 6 Market Estimates and Forecast, By Flute Type, 2021 – 2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 B flute

- 6.3 C flute

- 6.4 E flute

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Printing Technology, 2021 – 2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Flexographic printing

- 7.3 Digital printing

- 7.4 Lithographic printing

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 E-commerce & retail

- 8.3 Consumer electronics

- 8.4 Healthcare & pharmaceuticals

- 8.5 Personal care & cosmetics

- 8.6 Automotive & industrial goods

- 8.7 Food & beverage

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbe

- 10.2 Corrugated Supplies Company

- 10.3 DS Smith

- 10.4 Hinojosa Packaging Group

- 10.5 International Paper Company

- 10.6 Kite Packaging

- 10.7 Mondi

- 10.8 Papeles y Conversiones de Mexico

- 10.9 Papierfabrik Palm

- 10.10 Ribble Packaging

- 10.11 Rondo Ganahl

- 10.12 Smurfit Kappa Group

- 10.13 Stora Enso

- 10.14 WestRock