生体適合3Dプリンティング材料市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Biocompatible 3D Printing Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1721477

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

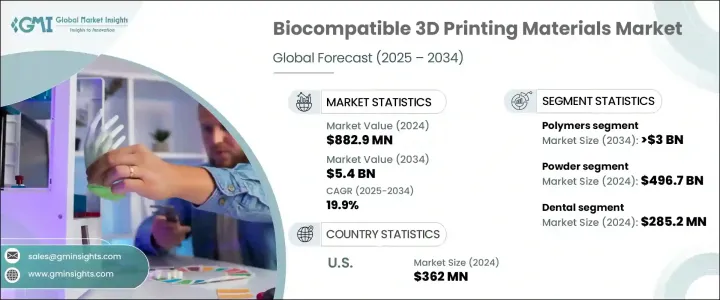

世界の生体適合3Dプリンティング材料市場は、2024年には8億8,290万米ドルと評価され、CAGR 19.9%で成長し、2034年には54億米ドルに達すると推定されています。

この成長軌道は、高いレベルの精度、性能、患者適合性を提供する次世代医療材料に対する需要の高まりを反映しています。特に高齢化社会における高度な医療介入のニーズの高まりが、さまざまなヘルスケア用途における3Dプリント材料の採用に拍車をかけています。世界のヘルスケアシステムがより患者中心のアプローチに軸足を移す中、生体適合3Dプリンティング材料の使用は、カスタマイズされた効率的で低侵襲な医療ソリューションを提供する上で不可欠になっています。整形外科や義肢装具に加え、この材料は歯科治療、手術器具、組織足場、再生医療において広く支持を集めています。これらの材料は、複雑な形状をサポートし、手術結果を向上させ、回復時間を短縮する能力があるため、現代の医療製造において不可欠なコンポーネントとして位置づけられています。有利な規制政策、研究開発投資の拡大、個別化ヘルスケアに対する意識の高まりにより、市場は先進国、新興経済諸国ともに大きな勢いを見せ続けています。

市場の成長は、選択的レーザー焼結(SLS)、ステレオリソグラフィ(SLA)、ダイレクトメタルレーザー焼結(DMLS)などの積層造形技術の急速な進歩にも大きく起因しています。これらの技術により、個々の解剖学的要件に沿った、高精度で生体適合性の高い医療用コンポーネントの製造が可能になります。高性能金属合金、ポリマー、バイオインクの開発により、印刷されたバイオメディカル製品の信頼性、耐久性、適合性が向上し、材料の革新が市場拡大にさらに貢献しています。これらのブレークスルーは、性能の向上と合併症発生率の低減を実現する機能的インプラント、人工器官、手術器具の作製に特に関連しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 8億8,290万米ドル |

| 予測金額 | 54億米ドル |

| CAGR | 19.9% |

市場は、ポリマー、金属、その他の材料タイプに区分され、ポリマーのカテゴリーが今後の成長をリードすると予想されます。このセグメントは2034年までに30億米ドルに達し、CAGR 19.9%で成長すると予測されています。カスタマイズされた3Dプリントポリマーに対する需要の高まりは、患者固有のインプラント、歯科修復物、補綴装置の製造において顕著です。ポリエーテルエーテルケトン(PEEK)、ポリ乳酸(PLA)、生体吸収性ポリマーなどの先端材料は、その優れた強度、生体適合性、複雑な医療要件への適応性により台頭しています。

歯科分野は2024年に2億8,520万米ドルを占め、歯の喪失、歯周病、う蝕のような症状の有病率の増加に牽引されて、着実に拡大しています。SLA、デジタル・ライト・プロセッシング(DLP)、SLSなどの技術は、歯科修復物の精度、強度、適合性を劇的に改善し、歯科専門家や患者の需要を押し上げています。

米国の生体適合3Dプリンティング材料市場は、2024年に3億6,200万米ドルと評価され、高齢化による歯科および整形外科的問題のリスクの高まりにより大きな成長を遂げています。オーダーメイドの補綴物やインプラントを迅速に製造できることから、全国の医療施設で3Dプリンティングの導入が加速しています。

世界市場の主要企業には、Stratasys、3D Systems、GE Additive、Formlabs、Materialise、Renishaw、Royal DSM、Arkema、Solvay、Cellink、Concept Laser、EOS、Evonik Industries、EnvisionTEC、Hoganasなどがあります。これらの企業は、生体適合性と応用精度を向上させるため、先進的な高性能素材に積極的に投資しています。ヘルスケアプロバイダーや研究機関との戦略的提携は、3Dプリンティングの臨床的有用性の拡大に役立っています。さらに、革新的で病態に特化したソリューションに焦点を当てた継続的な製品開発により、市場のリーダー企業は世界な事業展開と競争力の強化を図っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- ヘルスケア業界における生体適合性3Dプリントの需要増加

- 3Dプリント材料の技術的進歩

- パーソナライズ医療の導入拡大

- 業界の潜在的リスク&課題

- 生体適合3Dプリンティング材料の高コスト

- 厳格な規制要件

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材質別、2021-2034

- 主要動向

- ポリマー

- 金属

- その他の素材の種類

第6章 市場推計・予測:形態別、2021-2034

- 主要動向

- 粉

- 液体

- その他の形式

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 歯科

- ドラッグデリバリーシステム

- 手術器具とインプラント

- 組織工学

- 心血管系

- 整形外科

- その他の用途

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Arkema

- BIO INX

- Cellink

- EnvisionTEC

- EOS

- Evonik Industries

- Formlabs

- GE Additive

- Hoganas

- Materialise

- Renishaw

- Royal DSM

- Solvay

- Stratasys

- 3D Systems

目次

The Global Biocompatible 3D Printing Materials Market was valued at USD 882.9 million in 2024 and is estimated to grow at a CAGR of 19.9% to reach USD 5.4 billion by 2034. This growth trajectory reflects the rising demand for next-generation medical materials that offer high levels of precision, performance, and patient compatibility. The increasing need for advanced medical interventions, particularly among the aging population, is fueling the adoption of 3D-printed materials across a variety of healthcare applications. As global healthcare systems pivot toward more patient-centric approaches, the use of biocompatible 3D printing materials is becoming critical in delivering customized, efficient, and minimally invasive medical solutions. In addition to orthopedics and prosthetics, the materials are gaining widespread traction in dental care, surgical tools, tissue scaffolds, and regenerative medicine. The ability of these materials to support complex geometries, enhance surgical outcomes, and reduce recovery times positions them as essential components in modern medical manufacturing. With favorable regulatory policies, growing R&D investments, and expanding awareness about personalized healthcare, the market continues to experience substantial momentum across both developed and emerging economies.

The market's growth is also largely attributed to rapid advancements in additive manufacturing techniques, including Selective Laser Sintering (SLS), Stereolithography (SLA), and Direct Metal Laser Sintering (DMLS). These technologies enable the production of highly accurate and biocompatible medical components that align with individual anatomical requirements. Material innovations further contribute to market expansion, with the development of high-performance metal alloys, polymers, and bioinks improving the reliability, durability, and compatibility of printed biomedical products. These breakthroughs are particularly relevant in creating functional implants, prosthetics, and surgical tools that offer improved performance and reduced complication rates.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $882.9 Million |

| Forecast Value | $5.4 Billion |

| CAGR | 19.9% |

The market is segmented into polymers, metals, and other material types, with the polymers category expected to lead future growth. This segment is projected to reach USD 3 billion by 2034, growing at a CAGR of 19.9%. The rising demand for customized 3D-printed polymers is evident in the production of patient-specific implants, dental restorations, and prosthetic devices. Advanced materials such as Polyether Ether Ketone (PEEK), Polylactic Acid (PLA), and bioresorbable polymers are gaining ground due to their superior strength, biocompatibility, and adaptability to complex medical requirements.

The dental sector accounted for USD 285.2 million in 2024 and is expanding steadily, driven by the increasing prevalence of conditions like tooth loss, periodontal diseases, and dental caries. Technologies such as SLA, Digital Light Processing (DLP), and SLS have dramatically improved the precision, strength, and fit of dental restorations, boosting demand among dental professionals and patients alike.

The U.S. Biocompatible 3D Printing Materials Market was valued at USD 362 million in 2024 and is experiencing significant growth due to the aging population's heightened risk of dental and orthopedic issues. The ability to rapidly manufacture tailored prosthetics and implants has accelerated the adoption of 3D printing in medical facilities across the country.

Key players in the global market include Stratasys, 3D Systems, GE Additive, Formlabs, Materialise, Renishaw, Royal DSM, Arkema, Solvay, Cellink, Concept Laser, EOS, Evonik Industries, EnvisionTEC, and Hoganas. These companies are actively investing in advanced, high-performance materials to improve biocompatibility and application precision. Strategic collaborations with healthcare providers and research organizations are helping to expand the clinical utility of 3D printing. Moreover, ongoing product development focused on innovative, condition-specific solutions is allowing market leaders to enhance their global footprint and competitive positioning.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand of biocompatible 3D printing in healthcare industry

- 3.2.1.2 Technological advancements in 3D printing materials

- 3.2.1.3 Growing adoption of personalized medicine

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of biocompatible 3D printing materials

- 3.2.2.2 Stringent regulatory requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Polymers

- 5.3 Metals

- 5.4 Other material types

Chapter 6 Market Estimates and Forecast, By Form, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Powder

- 6.3 Liquid

- 6.4 Other forms

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Dental

- 7.3 Drug delivery systems

- 7.4 Surgical tools and implants

- 7.5 Tissue engineering

- 7.6 Cardiovascular

- 7.7 Orthopedic

- 7.8 Other applications

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Arkema

- 9.2 BIO INX

- 9.3 Cellink

- 9.4 EnvisionTEC

- 9.5 EOS

- 9.6 Evonik Industries

- 9.7 Formlabs

- 9.8 GE Additive

- 9.9 Hoganas

- 9.10 Materialise

- 9.11 Renishaw

- 9.12 Royal DSM

- 9.13 Solvay

- 9.14 Stratasys

- 9.15 3D Systems

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日