|

市場調査レポート

商品コード

1721431

電動モーターホーンの市場機会、成長促進要因、産業動向分析、2025~2034年予測Electric Motor Horn Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 電動モーターホーンの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月10日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

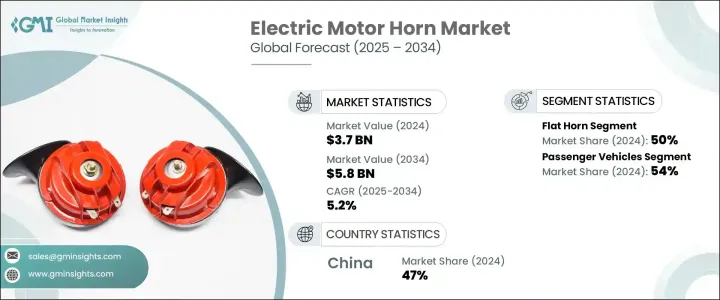

電動モーターホーンの世界市場規模は、2024年に37億米ドルとなり、CAGR 5.2%で成長し、2034年には58億米ドルに達すると推定されています。

この着実な成長の背景には、電気自動車(EV)の普及があり、電気モーターホーンの需要が急増しています。従来の内燃機関車(ICE)に比べて静かに作動するEVは、安全基準を満たすために効率的で低騒音の警告システムを必要とします。その結果、可聴警告システムは歩行者と交通の安全にとって不可欠なものとなっています。EVの普及が進むと同時に、騒音公害や放音基準に関する規制が高まり、メーカー各社は、効果的なだけでなく、政府の義務に準拠したホーンの革新と生産に取り組んでいます。

新興国がより厳格な交通安全法を施行するにつれ、世界市場に変化が生じています。この動向は、EV専用に設計された、規制された低デシベルの電気ホーンの需要を促進しています。開発メーカーは、電気自動車やハイブリッド車に適した、エネルギー効率が高くコンパクトなホーンシステムを開発し、安全性と環境要件の両方を満たす必要に迫られています。持続可能性への注目が高まる中、最適なサウンドレベルを維持しながら消費電力を削減することは、業界にとって重要な課題であり、技術革新の分野となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 37億米ドル |

| 予測金額 | 58億米ドル |

| CAGR | 5.2% |

2024年には、フラットタイプの電動モーターホーン分野が市場シェアの50%を占める。これらのホーンは、コンパクトで場所を取らない設計、堅牢性、コスト効率で支持され、二輪車、乗用車、小型商用車に好んで使用されています。その汎用性と統合の容易さにより、相手先商標製品メーカー(OEM)とアフターマーケットサプライヤーの両方において、市場での優位性を保ち続けています。

乗用車セグメントは2024年に市場の54%のシェアを占め、2025年から2034年にかけてCAGR 5%で安定した成長が見込まれています。この成長の原動力となっているのは、インドや中国などの新興市場で乗用車の人気が高まっていることです。これらの地域では都市化、可処分所得、自動車所有率が上昇しており、信頼性が高く手頃な価格の安全機能に対する需要が高まっています。乗用車における電動モーターホーンの需要は、商用車や二輪車のそれを上回り続けており、最大の消費者セグメントとしての地位を固めています。

中国電動モーターホーン市場は、2024年に7億5,600万米ドルを生み出し、世界市場シェアの47%を占めました。この優位性は、自動車生産台数の多さ、EVの普及、政府による交通安全の義務付けに起因します。コストに敏感な消費者が、耐久性のある先進的なホーン・システムの需要を押し上げています。さらに、自動車所有率の増加がアフターマーケットの成長に拍車をかけており、インテリジェントな低ノイズホーン・ソリューションが需要をさらに押し上げています。

電動モーターホーン世界市場の主要プレーヤーには、HELLA、パナソニック、ジョンソン・エレクトリック、デンソー、UNO Minda、MITSUBA、Imasen Electric Industrial、Robert Bosch、日本電産、FIAMM Technologiesなどがいます。競争力を維持するため、各社は研究開発に投資し、国際的な規制に準拠し、音量をカスタマイズできる小型で低エネルギーのホーンを開発しています。EV自動車メーカーとの戦略的パートナーシップ、成長率の高い新興国市場への事業拡大、車両エレクトロニクスと統合したスマートホーンシステムの開発は、成長のための主要戦略です。メーカーはまた、価格戦略を最適化し、アフターマーケット流通チャネルを通じた交換部品需要の増加に対応するため、現地生産能力を強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料サプライヤー

- 部品メーカー

- 電動モーターホーンメーカー

- OEM(相手先商標製造会社)およびティア1サプライヤー

- アフターマーケットの販売代理店および小売業者

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 主要原材料の価格変動

- サプライチェーンの再構築

- 最終市場への価格伝達

- 主要原材料の価格変動

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 世界の自動車生産の増加

- 世界中の政府が自動車の安全基準を義務付けている

- 電気自動車(EV)の需要増加

- 電動モーターホーンの技術的進歩

- 業界の潜在的リスク&課題

- 厳しい騒音公害規制

- ADASと自動運転車の導入拡大

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- フラット型ホーン

- スパイラル型ホーン

- トランペット

第6章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 二輪車

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第7章 市場推計・予測:音圧別、2021-2034

- 主要動向

- 最大110dB

- 110dB~118dB

- 118 dBを超える

第8章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Chief Enterprises

- CHINT Automotive

- Denso

- FIAMM Technologies

- Grote Industries

- HELLA

- Imasen Electric Industrial

- Jindong Electronic Technology

- Johnson Electric

- MARUKO KEIHOKI

- MITSUBA

- Miyamoto Electric Horn

- Nidec

- Oriental Motor

- Panasonic

- Robert Bosch

- Roots Industries India Limited

- SEGER Horns

- UNO Minda

- Wolo Manufacturing

The Global Electric Motor Horn Market was valued at USD 3.7 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 5.8 billion by 2034. This steady growth is fueled by the increasing adoption of Electric Vehicles (EVs), which have generated a surge in demand for electric motor horns. EVs, which operate quietly compared to traditional internal combustion engine (ICE) vehicles, require efficient, low-noise warning systems to meet safety standards. As a result, audible alert systems have become critical for pedestrian and road safety. Alongside the growing adoption of EVs, rising regulations on noise pollution and sound emission standards are pushing manufacturers to innovate and produce horns that are not only effective but also compliant with government mandates.

The global market is witnessing a shift as emerging economies enforce stricter road safety laws. This trend is driving the demand for regulated, low-decibel electric horns designed specifically for EVs. Manufacturers are under increasing pressure to develop energy-efficient, compact horn systems suitable for electric and hybrid vehicles, which meet both safety and environmental requirements. With a rising focus on sustainability, reducing power consumption while maintaining optimal sound levels has become a key challenge and innovation area for the industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $5.8 Billion |

| CAGR | 5.2% |

In 2024, the flat-type electric motor horns segment accounted for 50% of the market share. These horns are favored for their compact, space-saving design, robustness, and cost-efficiency, making them the preferred choice for motorcycles, passenger cars, and light commercial vehicles. Their versatility and ease of integration ensure their continued dominance in the market, both among original equipment manufacturers (OEMs) and aftermarket suppliers.

The passenger vehicle segment held a 54% share of the market in 2024 and is expected to grow steadily at a 5% CAGR between 2025 and 2034. This growth is driven by the increasing popularity of passenger cars in emerging markets such as India and China. Rising urbanization, disposable income, and vehicle ownership in these regions fuel the demand for reliable and affordable safety features. The demand for electric motor horns in passenger vehicles continues to surpass that of commercial vehicles and two-wheelers, solidifying its position as the largest consumer segment.

China electric motor horn market generated USD 756 million in 2024, accounting for 47% of the global market share. This dominance is attributed to high automotive production volumes, widespread EV adoption, and government-backed road safety mandates. Cost-sensitive consumers are driving the local demand for durable, advanced horn systems. Additionally, the increasing vehicle ownership rate is spurring aftermarket growth, with intelligent low-noise horn solutions further boosting demand.

Key players in the Global Electric Motor Horn Market include HELLA, Panasonic, Johnson Electric, Denso, UNO Minda, MITSUBA, Imasen Electric Industrial, Robert Bosch, Nidec, and FIAMM Technologies. To maintain a competitive edge, companies are investing in research and development to create compact, low-energy horns with customizable sound levels that adhere to international regulations. Strategic partnerships with EV automakers, expanding operations into high-growth emerging markets, and the development of smart horn systems integrated with vehicle electronics are key strategies for growth. Manufacturers are also enhancing local production capacities to optimize pricing strategies and meet the increasing demand for replacement parts through aftermarket distribution channels.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 Electric motor horn manufacturers

- 3.2.4 Original equipment manufacturers (OEMs) and tier 1 suppliers

- 3.2.5 Aftermarket distributors and retailers

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Impact on trade

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on the Industry

- 3.3.2.1 Price volatility in key materials

- 3.3.2.1.1 Supply chain restructuring

- 3.3.2.1.2 Price transmission to end markets

- 3.3.2.1 Price volatility in key materials

- 3.3.3 Strategic industry responses

- 3.3.3.1 Supply chain reconfiguration

- 3.3.3.2 Pricing and product strategies

- 3.3.1 Impact on trade

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 The rise in global automobile production

- 3.9.1.2 Governments worldwide are mandating vehicle safety standards

- 3.9.1.3 Growing demand for electric vehicles (EVs)

- 3.9.1.4 Technological advancements in electric motor horns

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Stringent noise pollution regulations

- 3.9.2.2 Increasing adoption of ADAS & autonomous vehicles

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Flat type horn

- 5.3 Spiral type horn

- 5.4 Trumpet

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Two-Wheelers

- 6.4 Commercial vehicles

- 6.4.1 Light Commercial Vehicles (LCV)

- 6.4.2 Medium Commercial Vehicle (MCV)

- 6.4.3 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Sound Pressure, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Up to 110 dB

- 7.3 110 dB to 118 dB

- 7.4 Greater than 118 dB

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Chief Enterprises

- 10.2 CHINT Automotive

- 10.3 Denso

- 10.4 FIAMM Technologies

- 10.5 Grote Industries

- 10.6 HELLA

- 10.7 Imasen Electric Industrial

- 10.8 Jindong Electronic Technology

- 10.9 Johnson Electric

- 10.10 MARUKO KEIHOKI

- 10.11 MITSUBA

- 10.12 Miyamoto Electric Horn

- 10.13 Nidec

- 10.14 Oriental Motor

- 10.15 Panasonic

- 10.16 Robert Bosch

- 10.17 Roots Industries India Limited

- 10.18 SEGER Horns

- 10.19 UNO Minda

- 10.20 Wolo Manufacturing