|

市場調査レポート

商品コード

1721415

電気商用車MRO市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Electric Commercial Vehicle MRO (Maintenance, Repair, Overhaul) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 電気商用車MRO市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月07日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

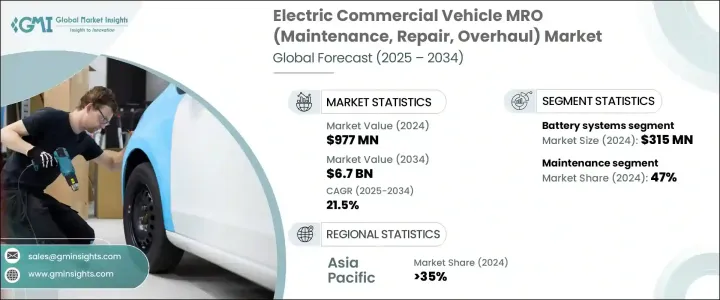

世界の電気商用車MRO市場は、2024年には9億7,700万米ドルと評価され、CAGR 21.5%で成長し、2034年には67億米ドルに達すると予測されています。

電気商用車(ECV)が様々な産業で広く受け入れられるようになり、市場は力強い勢いを増しています。内燃機関車(ICE)から電気自動車へのシフトは、環境問題への関心の高まり、厳しい排出ガス規制、政府によるEV優遇措置などにより加速しています。フリートは、持続可能性の目標を達成し、総所有コストを削減するために、ますます電動化に向かっています。電気商用車が公共および民間の輸送システム、特にラスト・マイル・デリバリー、ロジスティクス、公共交通機関などの分野に浸透し続けるにつれ、信頼性が高く、迅速で、専門的なMROサービスに対する需要が急速に拡大しています。車両メンテナンスと並んで、充電インフラや診断ツールなど、ECVを支えるエコシステムも進化しています。カスタマイズされたメンテナンスプログラム、部品交換、ソフトウェアベースの診断に対するニーズの高まりにより、新たな複雑性が加わり、MROプロバイダーはダイナミックな情勢の中で競争力を維持するために次世代のツールや技術を採用する必要に迫られています。

この市場拡大に大きく貢献しているのは、EV充電インフラの広範な開拓であり、これは電気商用車の普及を直接的に支えています。特に遠隔地やサービスが行き届いていない地域で充電ステーションが増えるにつれて、フリートオペレーターは従来の燃料システムから電動モビリティへの切り替えがますます現実的になっていることを実感しています。充電器、コネクター、内部配線、ソフトウェアなど、こうしたインフラを維持することは、MROサービスの需要拡大にさらに貢献します。ECVがロジスティクス、配送、公共輸送業務に不可欠になるにつれて、それぞれに合わせた修理・サービスサポートが必要となり、北米、アジア太平洋、ラテンアメリカ、欧州、中東・アフリカなどの地域で成長を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 9億7,700万米ドル |

| 予測金額 | 67億米ドル |

| CAGR | 21.5% |

コンポーネント別では、電動ドライブトレイン、熱管理システム、充電システム、バッテリーシステム、その他が含まれます。2024年の市場規模は、バッテリーシステムが3億1,500万米ドルで、30%の圧倒的シェアを占めています。これらのコンポーネントは自動車の航続距離と効率に不可欠であり、その性能は運転稼働時間に直接影響します。充電サイクルの繰り返し、極端な温度への暴露、使用による摩耗はバッテリーを劣化させることが多く、定期的な評価とタイムリーな交換が求められます。フリートオペレーターは、コストのかかるダウンタイムを避けるためにバッテリーの健全性を優先するため、重点的にバッテリー管理サービスを提供する専門的なMROプロバイダーに対する安定した需要が確保されます。

市場セグメンテーションをサービスタイプ別に分類すると、市場にはメンテナンス、修理、オーバーホールが含まれ、2024年のシェアはメンテナンスが47%を占める。ECVは従来の自動車に比べて機械部品が少ないとはいえ、ソフトウェア診断、ブレーキ検査、部品の適合といった精密なケアが必要です。車両の寿命を延ばし、安全性を高め、性能を最適化するためには、定期的なメンテナンスが不可欠であることに変わりはないです。フリート・オペレーターは、予測可能なコストと最小限の中断を提供し、サービス・プロバイダーの一貫した収益源を支える予防メンテナンス・プログラムに大きく依存しています。

中国の電気商用車MRO市場は、2024年に9,210万米ドルを創出しました。強力な国内生産、政策支援、急速な車両配備により、同国は世界のトップランナーとなっています。急成長する都市配送、公共輸送、ロジスティクス部門は、診断から複雑な修理に至るまで、堅牢な技術対応MROサービスの必要性を高め続けています。

ダイムラー、エレメント・フリート・マネジメント、ATSユーロマスター、BPパルス、フェルドッティ・モーター・サービス、スカニア、ライオン・エレクトリック、MAN世界、マーチャンツ・フリート、ボルボといった業界の主要企業は、MROポートフォリオを拡大しています。これらの企業は、EV専用サービスセンターの設立、技術者トレーニングプログラムの強化、予知保全のためのテレマティクスの活用を進めています。自動車メーカーやフリートオペレーターとの戦略的パートナーシップにより、効率的なサービス提供を実現しています。AIを活用した診断と遠隔監視は、修理サイクルを加速し、車両のダウンタイムを最小限に抑えるための標準ツールになりつつあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- オリジナル機器メーカー

- 独立系サービスプロバイダー

- 部品サプライヤー

- テクノロジープロバイダー

- 最終用途

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- ケーススタディ

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 電気商用車の導入増加

- 充電インフラの拡張

- 電気自動車とバッテリーのコスト低下

- クリーンで持続可能な交通手段の需要の増加

- 業界の潜在的リスク&課題

- 電気商用車の初期コストが高め

- 熟練労働力の不足

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:車両別、2021-2034

- 主要動向

- 小型商用車

- MCV

- HCV

第6章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- バッテリーシステム

- 熱管理システム

- 充電システム

- 電動ドライブトレイン

- その他

第7章 市場推計・予測:サービス別、2021-2034

- 主要動向

- メンテナンス

- 修理

- オーバーホール

第8章 市場推計・予測:サービスプロバイダー別、2021-2034

- 主要動向

- OEMサービスセンター

- 独立系サービスプロバイダー

- 艦隊整備業務

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- ATS Euromaster

- BP Pulse

- Daimler

- Element Fleet Management

- Ferdotti Motor Services

- Kerlin Bus Sales &Leasing

- Lightning eMotors

- Lion Electric

- MAN Global

- Merchants Fleet

- Northeastern Bus Rebuilders

- Orange EV

- Scania

- Sonny Merryman

- Transdev

- VDL Company

- VEV Services Limited

- Volvo

- WattEV

- YES EU

The Global Electric Commercial Vehicle MRO Market was valued at USD 977 million in 2024 and is estimated to grow at a CAGR of 21.5% to reach USD 6.7 billion by 2034. The market is gaining robust momentum as electric commercial vehicles (ECVs) become more widely accepted across various industries. The shift from internal combustion engine (ICE) vehicles to electric alternatives is accelerating due to rising environmental concerns, stringent emissions regulations, and government-backed EV incentives. Fleets are increasingly moving toward electrification to meet sustainability goals and reduce the total cost of ownership. As electric commercial vehicles continue to penetrate public and private transport systems, especially in sectors such as last-mile delivery, logistics, and public transit, the demand for reliable, fast, and specialized MRO services is expanding rapidly. Alongside vehicle maintenance, the ecosystem supporting ECVs-including charging infrastructure and diagnostic tools-is also evolving. The rising need for customized maintenance programs, parts replacement, and software-based diagnostics has added new layers of complexity, driving MRO providers to adopt next-gen tools and technologies to remain competitive in a dynamic landscape.

A significant contributor to this market expansion is the widespread development of EV charging infrastructure, which directly supports greater adoption of electric commercial vehicles. As more charging stations emerge, particularly in remote or underserved regions, fleet operators find it increasingly feasible to switch from traditional fuel-powered systems to electric mobility. Maintaining this infrastructure-such as chargers, connectors, internal cabling, and software-further contributes to the growing demand for MRO services. As ECVs become integral to logistics, delivery, and public transport operations, they require tailored repair and service support, pushing growth across regions including North America, Asia Pacific, Latin America, Europe, and the Middle East & Africa.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $977 Million |

| Forecast Value | $6.7 Billion |

| CAGR | 21.5% |

By component, the market includes electric drivetrain, thermal management systems, charging systems, battery systems, and others. In 2024, battery systems held a dominant 30% market share, valued at USD 315 million. These components are critical to a vehicle's range and efficiency, and their performance directly impacts operational uptime. Repeated charging cycles, exposure to extreme temperatures, and usage wear often degrade batteries, prompting routine assessments and timely replacements. Fleet operators prioritize battery health to avoid costly downtimes, ensuring steady demand for expert MRO providers that offer focused battery management services.

Segmented by service type, the market includes maintenance, repair, and overhaul, with maintenance commanding a 47% share in 2024. Even though ECVs have fewer mechanical components than traditional vehicles, they require precise care such as software diagnostics, brake inspections, and component calibration. Scheduled maintenance remains essential to prolonging vehicle life, enhancing safety, and optimizing performance. Fleet operators rely heavily on preventive maintenance programs, which provide predictable costs and minimal disruptions, supporting a consistent revenue stream for service providers.

China's Electric Commercial Vehicle MRO Market generated USD 92.1 million in 2024. Strong domestic production, policy support, and rapid fleet deployment have made the country a global frontrunner. Its booming urban delivery, public transport, and logistics sectors continue to elevate the need for robust, tech-enabled MRO services-from diagnostics to complex repairs.

Key industry players such as Daimler, Element Fleet Management, ATS Euromaster, BP Pulse, Ferdotti Motor Services, Scania, Lion Electric, MAN Global, Merchants Fleet, and Volvo are expanding their MRO portfolios. These companies are establishing dedicated EV service centers, enhancing technician training programs, and leveraging telematics for predictive maintenance. Strategic partnerships with automakers and fleet operators help them ensure efficient service delivery. AI-powered diagnostics and remote monitoring are becoming standard tools to accelerate repair cycles and minimize vehicle downtime.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Original equipment manufacturers

- 3.2.2 Independent service providers

- 3.2.3 Component suppliers

- 3.2.4 Technology providers

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Case study

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increased adoption of electric commercial fleets

- 3.9.1.2 Expansion of charging infrastructure

- 3.9.1.3 Declining costs of electric vehicles and batteries

- 3.9.1.4 Rise in demand for clean and sustainable transportation

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High Initial cost of electric commercial vehicles

- 3.9.2.2 Limited availability of skilled workforce

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 LCV

- 5.3 MCV

- 5.4 HCV

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Battery systems

- 6.3 Thermal management systems

- 6.4 Charging system

- 6.5 Electric drivetrain

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Service, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Maintenance

- 7.3 Repair

- 7.4 Overhaul

Chapter 8 Market Estimates & Forecast, By Service Provider, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 OEM service centers

- 8.3 Independent service providers

- 8.4 Fleet maintenance operations

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 ATS Euromaster

- 10.2 BP Pulse

- 10.3 Daimler

- 10.4 Element Fleet Management

- 10.5 Ferdotti Motor Services

- 10.6 Kerlin Bus Sales & Leasing

- 10.7 Lightning eMotors

- 10.8 Lion Electric

- 10.9 MAN Global

- 10.10 Merchants Fleet

- 10.11 Northeastern Bus Rebuilders

- 10.12 Orange EV

- 10.13 Scania

- 10.14 Sonny Merryman

- 10.15 Transdev

- 10.16 VDL Company

- 10.17 VEV Services Limited

- 10.18 Volvo

- 10.19 WattEV

- 10.20 YES EU