神経障害性疼痛治療市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Neuropathic Pain Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1721408

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

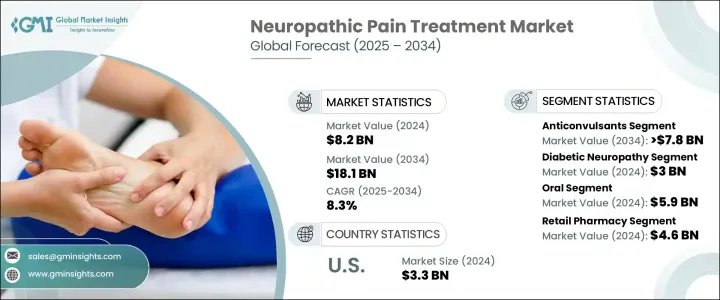

世界の神経障害性疼痛治療市場は、2024年に82億米ドルと評価され、CAGR 8.3%で成長し、2034年には181億米ドルに達すると推定されています。

この力強い成長軌道は、世界の高齢化、生活習慣病、糖尿病やがんのような慢性疾患の急増などの要因によって、神経障害性疼痛障害の負担が世界的に増加していることが背景にあります。神経関連の痛みやその衰弱に対する意識が高まるにつれて、早期診断と効果的な治療戦略に対する需要が急増し続けています。さらに、厳しい政府規制や安全性への懸念の高まりから、オピオイドをベースとした治療薬からの大幅なシフトが進み、患者の嗜好が進化していることも市場を後押ししています。ドラッグデリバリーシステム、バイオテクノロジー、新規製剤の進歩は、治療の展望に新たな扉を開いた。デジタルヘルスプラットフォームや遠隔医療サービスが利用可能になったことで、特に恵まれない地域における専門医療へのアクセスが強化され、神経障害性疾患の診断とタイムリーな介入が加速しています。

慢性疼痛の有病率の増加と、より安全な代替治療への緊急のニーズが、次世代治療薬の開発を促進しています。メーカー各社は、非オピオイド薬、遺伝子治療薬、モノクローナル抗体、バイオシミラーなど、急性・慢性両方の神経障害性疼痛に対応するよう設計された革新的な医薬品パイプラインに注力しています。これらの画期的な治療薬は、副作用を最小限に抑えながら、標的を絞った長期的な緩和を提供することを目的としており、疼痛管理における大きな飛躍を意味します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 82億米ドル |

| 予測金額 | 181億米ドル |

| CAGR | 8.3% |

薬剤クラス別では、抗けいれん薬が引き続き市場を独占しており、CAGR 8.5%で成長し、2034年には78億米ドルに達すると予測されます。プレガバリン、ガバペンチン、カルバマゼピンなどの広く処方されている薬剤は、その高い有効性と良好な安全性プロファイルにより、第一選択薬として認められています。特に、糖尿病による神経障害、帯状疱疹後神経痛、脊髄損傷などの治療で広く使用されています。慢性疾患の罹患率が上昇するにつれて、これらの実績のある薬剤の採用も増加し、市場での牙城を強めています。

適応症に関しては、糖尿病性神経障害が2024年の売上高で30億米ドルを占めています。世界的に糖尿病患者数が増加しており、長期的な治療ソリューションに対する需要が高まっています。神経障害治療に対する保険適用と償還の増加により、プレガバリンやカプサイシンパッチなどの治療が患者にとってより利用しやすくなり、アドヒアランスと治療成績が向上しています。

米国の神経障害性疼痛治療市場だけでも、2024年には33億米ドルと評価され、今後も大きな成長が見込まれています。この成長は主に、同国の高齢化、がん、糖尿病、帯状疱疹などの疾患の有病率の上昇によるものです。オピオイド処方に対する連邦政府の規制も、非オピオイド代替薬への需要を強化し、治療力学の大きな転換を促しています。

Assertio Therapeutics、Glenmark Pharmaceuticals、Cipla、Dr. Reddy's Laboratories、Johnson &Johnson、Eli Lilly and Company、GlaxoSmithKline、Biogen、Grunenthal、Mallinckrodt Pharmaceuticals、Novartis、Pfizer、Sun Pharmaceutical Industries、Teva Pharmaceutical Industries、Vertex Pharmaceuticalsなどが、このダイナミックな状況を形成している主要企業です。これらの企業は、治療パイプラインを積極的に拡大し、研究機関との戦略的提携を結ぶことで、新規治療をより迅速かつ効果的に市場に投入しようとしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 神経障害性疼痛疾患の有病率の上昇

- 医薬品開発と新しい治療法の進歩

- 高齢化人口の増加

- タイムリーな治療への意識向上

- 業界の潜在的リスク&課題

- 神経障害性疼痛治療薬の高コスト

- 薬物乱用の副作用とリスク

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- パイプライン分析

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:薬剤クラス別、2021-2034

- 主要動向

- 抗けいれん薬

- 抗うつ薬

- オピオイド

- カプサイシノイド

- その他の薬物クラス

第6章 市場推計・予測:適応症別、2021-2034

- 主要動向

- 糖尿病性神経障害

- 帯状疱疹後神経痛

- 三叉神経痛

- 化学療法誘発性末梢神経障害

- HIV関連神経障害

- その他の適応症

第7章 市場推計・予測:投与経路別、2021-2034

- 主要動向

- オーラル

- トピック

- 注射剤

第8章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 病院薬局

- 小売薬局

- eコマース

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Assertio Therapeutics

- Biogen

- Cipla

- Dr. Reddy’s Laboratories

- Eli Lilly and Company

- GlaxoSmithKline

- Glenmark Pharmaceuticals

- Grunenthal

- Johnson &Johnson

- Mallinckrodt Pharmaceuticals

- Novartis

- Pfizer

- Sun Pharmaceutical Industries

- Teva Pharmaceutical Industries

- Vertex Pharmaceuticals

目次

The Global Neuropathic Pain Treatment Market was valued at USD 8.2 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 18.1 billion by 2034. This robust growth trajectory is fueled by a rising burden of neuropathic pain disorders worldwide, fueled by factors such as an aging global population, lifestyle-related diseases, and a surge in chronic conditions like diabetes and cancer. As awareness about nerve-related pain and its debilitating effects increases, the demand for early diagnosis and effective treatment strategies continues to soar. The market is further propelled by evolving patient preferences, with a significant shift away from opioid-based therapies due to stringent government regulations and growing safety concerns. Advancements in drug delivery systems, biotechnology, and novel formulations have opened new doors for the treatment landscape. The availability of digital health platforms and telemedicine services is enhancing access to specialized care, particularly in underserved regions, accelerating diagnosis and timely intervention for neuropathic conditions.

The increasing prevalence of chronic pain and the urgent need for safer treatment alternatives are driving the development of next-generation therapies. Manufacturers are focusing on innovative drug pipelines that include non-opioid medications, gene therapies, monoclonal antibodies, and biosimilars designed to address both acute and chronic forms of neuropathic pain. These breakthrough therapies aim to provide targeted, long-lasting relief while minimizing side effects, representing a major leap forward in pain management.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.2 Billion |

| Forecast Value | $18.1 Billion |

| CAGR | 8.3% |

Based on drug class, anticonvulsants continue to dominate the market and are expected to grow at a CAGR of 8.5%, reaching USD 7.8 billion by 2034. Widely prescribed medications like pregabalin, gabapentin, and carbamazepine are recognized as first-line treatments due to their high efficacy and favorable safety profiles. Their extensive use is especially notable in the treatment of diabetes-induced neuropathy, postherpetic neuralgia, and spinal cord injuries. As chronic disease incidence rises, so does the adoption of these proven medications, reinforcing their stronghold in the market.

When it comes to indications, diabetic neuropathy accounted for USD 3 billion in revenue in 2024. The escalating number of diabetic patients globally is generating sustained demand for long-term treatment solutions. Increased insurance coverage and reimbursement for neuropathic treatments are making therapies such as pregabalin and capsaicin patches more accessible to patients, improving adherence and outcomes.

The U.S. Neuropathic Pain Treatment Market alone was valued at USD 3.3 billion in 2024 and is anticipated to witness significant growth ahead. This rise is primarily due to the country's aging population and the rising prevalence of conditions like cancer, diabetes, and shingles. Federal restrictions on opioid prescriptions are also reinforcing the demand for non-opioid alternatives, encouraging a major shift in treatment dynamics.

Assertio Therapeutics, Glenmark Pharmaceuticals, Cipla, Dr. Reddy's Laboratories, Johnson & Johnson, Eli Lilly and Company, GlaxoSmithKline, Biogen, Grunenthal, Mallinckrodt Pharmaceuticals, Novartis, Pfizer, Sun Pharmaceutical Industries, Teva Pharmaceutical Industries, and Vertex Pharmaceuticals are among the leading companies shaping this dynamic landscape. These firms are actively expanding their therapeutic pipelines and forging strategic alliances with research organizations to bring novel treatments to market faster and more effectively.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of neuropathic pain disorders

- 3.2.1.2 Advancements in drug development and novel therapies

- 3.2.1.3 Growing geriatric population

- 3.2.1.4 Increasing awareness towards timely treatment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of neuropathic pain medications

- 3.2.2.2 Side effects and risk of drug abuse

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Anticonvulsants

- 5.3 Antidepressants

- 5.4 Opioids

- 5.5 Capsaicinoids

- 5.6 Other drug classes

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Diabetic neuropathy

- 6.3 Postherpetic neuralgia

- 6.4 Trigeminal neuralgia

- 6.5 Chemotherapy-induced peripheral neuropathy

- 6.6 HIV-associated neuropathy

- 6.7 Other indications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Topical

- 7.4 Injectable

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacy

- 8.3 Retail pharmacy

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Assertio Therapeutics

- 10.2 Biogen

- 10.3 Cipla

- 10.4 Dr. Reddy’s Laboratories

- 10.5 Eli Lilly and Company

- 10.6 GlaxoSmithKline

- 10.7 Glenmark Pharmaceuticals

- 10.8 Grunenthal

- 10.9 Johnson & Johnson

- 10.10 Mallinckrodt Pharmaceuticals

- 10.11 Novartis

- 10.12 Pfizer

- 10.13 Sun Pharmaceutical Industries

- 10.14 Teva Pharmaceutical Industries

- 10.15 Vertex Pharmaceuticals

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日