|

市場調査レポート

商品コード

1885822

ハードウェア・イン・ザ・ループ試験市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測Hardware-in-the-Loop (HIL) Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ハードウェア・イン・ザ・ループ試験市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年11月26日

発行: Global Market Insights Inc.

ページ情報: 英文 206 Pages

納期: 2~3営業日

|

概要

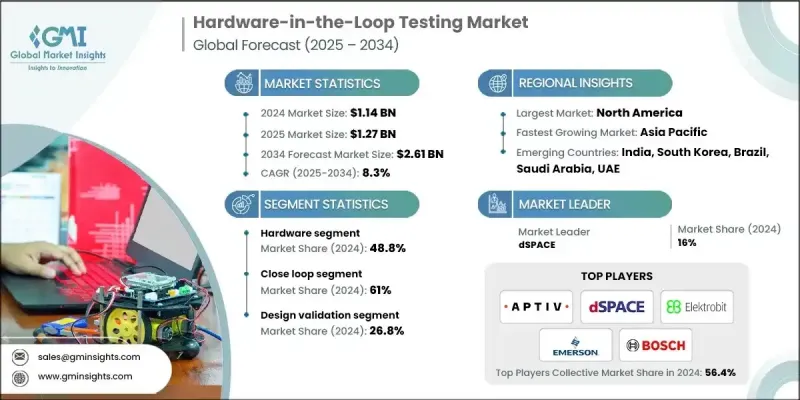

世界のハードウェア・イン・ザ・ループ(HIL)試験市場は、2024年に11億4,000万米ドルと評価され、2034年までにCAGR8.3%で成長し、26億1,000万米ドルに達すると予測されています。

高度な制御アーキテクチャへの急速な移行と、より迅速な製品検証の推進により、高度に複雑なシステム動作を再現できるリアルタイムシミュレーション環境の必要性が高まっています。HILプラットフォームは、継続的なソフトウェア検証、広範なマルチドメインテスト、運用障害の早期検出を支援し、現代のエンジニアリングワークフローにおいて不可欠な要素となっています。開発サイクルの加速に伴い、ソリューションプロバイダーは技術能力の拡充、リアルタイムコンピューティングリソースの拡張、高密度I/Oボードの追加、ソフトウェアツールチェーンとの連携強化を進めています。これらの強化策は、電動モビリティ、航空研究、次世代エネルギーシステムにおける需要増に対応するものです。企業は、高電圧アーキテクチャ、推進ユニット、系統連系機器を、実際のデバイスを危険にさらすことなく、熱的・経年劣化・変動負荷条件下で評価するため、HILテストへの依存度を高めています。この進化により、HIL技術は複数の産業分野にわたる先進的な検証手法の中核的推進力として位置づけられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年度 | 2025-2034 |

| 開始時価値 | 11億4,000万米ドル |

| 予測金額 | 26億1,000万米ドル |

| CAGR | 8.3% |

ハードウェアセグメントは2024年に48.8%のシェアを占め、2034年までCAGR7.1%で成長すると予測されています。その重要性は、リアルタイムコンピューティングユニット、高チャネル数インターフェースモジュール、プログラマブルプロセッサ、専用負荷ユニット、電力特化型リグなど、高性能な物理コンポーネントの必要性から生じています。これらのシステムは、重要な運用環境で使用される制御装置や組み込みロジックを検証するために必要な、マイクロ秒レベルの精密な性能を提供します。運輸、防衛、エネルギーなどの産業は、電気推進システム、安全重視の制御装置、高度な保護技術の実世界での動作を検証するために、これらのハードウェアプラットフォームに依存しています。

クローズドループ方式は2024年に61%のシェアを占め、2025年から2034年にかけて8%の成長が見込まれています。この手法が主流であり続ける理由は、物理コンポーネントと仮想モデル間のシームレスな相互作用を可能にし、動作挙動を反映した動的なテストサイクルを構築できる点にあります。エンジニアはクローズドループ構成を活用し、物理的な試作機を運用上の危険に晒すことなく、極めて現実的な条件下で制御ユニット、電動化システム、インテリジェント機能の性能を安全に検証します。

北米のハードウェア・イン・ザ・ループ(HIL)試験市場は、2024年に3億5,530万米ドルの規模に達しました。同地域の成長は、自動化技術の継続的な進歩、電動モビリティの開発、および高度にモジュール化された車両アーキテクチャの普及拡大によって支えられています。米国企業は、安全性、コンプライアンス、デジタルシステム完全性における進化する基準を満たすため、検証プログラムを拡大しています。バッテリー開発、電動化プラットフォーム、次世代駆動システムにおける著しい進歩が、物理的なプロトタイピングに関連するコスト削減とエンジニアリング期間の短縮を目的としたHIL環境の導入加速に貢献しています。

よくあるご質問

目次

第1章 調査手法

- 市場範囲と定義

- 調査設計

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域別/国別

- 基本推定値と計算

- 基準年計算

- 市場推定における主要な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査前提条件と制限事項

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- シリコンおよびコア技術プロバイダー

- プラットフォームおよびシステムサプライヤー

- ソフトウェア及びモデルプロバイダー

- システムインテグレーター及びプロフェッショナルサービス

- 利益率分析

- シリコンおよびコア技術プロバイダー

- プラットフォームおよびシステムサプライヤー

- ソフトウェア及びモデルプロバイダー

- システムインテグレーター及びサービス

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- エコシステムへの変革

- サプライヤーの情勢

- 業界への影響要因

- 促進要因

- 電気自動車の普及とバッテリーシステム検証要件の分析

- ADAS/自動運転車の複雑性とソフトウェア定義車両アーキテクチャ

- 規制要件および機能安全規格(ISO 26262、IEC 61508、DO-178C)

- パワーエレクトロニクスと再生可能エネルギーのグリッド統合

- コスト削減の必要性と仮想検証による実証済みROI

- 業界の潜在的リスク&課題

- 中小企業における高額な資本投資と長期にわたる回収期間

- 熟練労働力の不足と知識移転の課題

- モデル忠実度と検証上の課題

- 市場機会

- クラウドベースのHILおよびハードウェア・イン・ザ・ループ・アズ・ア・サービス(HILaaS)

- AI/機械学習によるテスト自動化とシナリオ生成

- デジタルツイン統合とライフサイクル検証

- アジア太平洋市場における拡大とローカライゼーション

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米における規制状況

- 米国:連邦および州レベルの要件

- カナダ:米国基準との調和

- 欧州の規制状況

- 欧州連合:包括的な型式承認およびサイバーセキュリティ要件

- 英国:ブレグジット後の規制の相違

- アジア太平洋の規制状況

- 中国:国内基準とデータローカリゼーション

- 日本:品質基準と自動車技術の卓越性

- インド:規制が急速に進化する新興市場

- 韓国:先進技術と輸出重視

- ラテンアメリカにおける規制状況

- ブラジル:地域リーダーであり、現地化要件を有しております

- メキシコ:USMCA統合と自動車製造拠点

- 中東・アフリカ地域の規制状況

- アラブ首長国連邦(UAE)及びサウジアラビア:意欲的な技術導入

- 南アフリカ:地域製造拠点

- 地域横断的な規制動向と戦略的示唆

- 北米における規制状況

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- FPGA加速リアルタイムシミュレーションプラットフォーム

- モデルベース設計(MBD)及びシミュレーションツールチェーン

- モジュラーPXI/EtherCATベースのHILアーキテクチャ

- 認証済み安全・コンプライアンスツールチェーン

- 新興技術

- クラウドネイティブHILプラットフォーム及びHIL-as-a-Service(HILaaS)

- AI/機械学習駆動のテスト自動化とシナリオ生成

- ライフサイクル検証のためのデジタルツイン統合

- サイバーセキュリティ検証及びセキュアなOTA更新テスト

- 現在の技術動向

- 特許分析

- コスト内訳分析

- 貿易フロー分析

- 輸入市場の市場力学

- 世界な輸入パターン

- 貿易障壁と現地化

- 輸出市場構造

- 輸出障壁とインセンティブ

- 貿易フローの動向と戦略的示唆

- 輸入市場の市場力学

- 持続可能性と環境面

- 持続可能な実践の導入

- 廃棄物削減の革新

- エネルギー効率の最適化

- 環境イニシアチブの影響

- 使用事例

- アイアンバード試験

- ミサイル開発

- 自律型ドローンの試験運用

- ADASおよび自動運転

- 電動化と電気駆動システム

- 電力系統

- 車両ダイナミクス

- バーチャルビークル

- テストベンチ

- 実走行排出量(RDE)

- ベストケースシナリオ

- ライフサイクル全体にわたるデジタルツインとHILの統合

- 世界コラボレーションのためのクラウドネイティブHILaaS

- AI/機械学習駆動型自律検証

- 再生可能エネルギー統合のためのPHIL

- モジュール式でアップグレード可能な循環型HILアーキテクチャ

- HIL市場における主要競合が採用しているFPGAシステム

- 性能と適用適合性

- スケーラビリティ、モジュール性、ライフサイクルコスト

- 規制および認証における優位性

- エコシステムと統合

- 地域別・規制別の差異化

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ハードウェア

- 入出力インターフェース

- PCIeベースのI/Oインターフェース

- 標準PCIeカード

- 高速データ収集モジュール

- カスタムFPGA統合型PCIeソリューション

- FPGAベースのI/Oソリューション

- インテル(アルテラ)Arriaベースのインターフェースモジュール

- ザイリンクスZynqベースのインターフェースモジュール

- FPGA I/O拡張ボード

- リアルタイム論理制御および信号調整インターフェース

- イーサネットベースおよびEtherCATインターフェース

- 産業用イーサネット(ギガビットイーサネット、10ギガビットイーサネット、TSN対応)

- EtherCATマスター/スレーブモジュール

- EtherCAT搭載分散I/Oノード

- 時間同期通信モジュール

- PCIeベースのI/Oインターフェース

- プロセッサー

- リアルタイムシミュレーター

- データ収集システム

- その他

- 入出力インターフェース

- ソフトウェア

- サービス

- 専門サービス

- マネージドサービス

第6章 市場推計・予測:提供別、2021-2034

- 主要動向

- オープンループ

- クローズドループ

第7章 市場推計・予測:試験段階別、2021-2034

- 主要動向

- 設計検証

- 統合テスト

- 受入試験

- 製造試験

- 性能テスト

- その他

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 航空宇宙産業

- 防衛分野

- 鉄道

- パワーエレクトロニクス

- 自動車

- 医療機器

- 再生可能エネルギーシステム

- 通信およびネットワーク

- その他

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ANZ

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第10章 企業プロファイル

- 世界の企業

- MathWorks

- National Instruments

- dSPACE

- Vector Informatik

- Spirent Communications

- Wind River

- Robert Bosch

- Emerson

- 地域の企業

- ADVANTECH

- APTIV

- Wabtec

- ETAS

- Hinduja Tech

- Elektrobit

- ニッチ/新興企業

- ADD2

- Concurrent Real-Time

- IPG Automotive

- Lynx Software Technologies

- Opal-RT Technologies

- Plexim

- RealTime Wave

- Speedgoat

- Typhoon HIL