|

市場調査レポート

商品コード

1716657

動物飼料添加物市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Animal Feed Additives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 動物飼料添加物市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月13日

発行: Global Market Insights Inc.

ページ情報: 英文 263 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

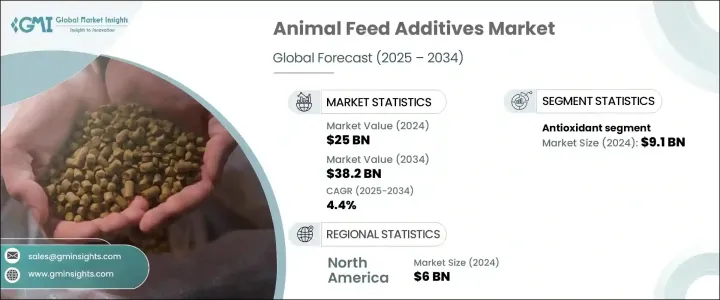

世界の動物飼料添加物市場は2024年に250億米ドルに達し、2025年から2034年にかけてCAGR 4.4%で成長すると予測されています。

飼料添加物は家畜飼料の栄養価を高め、家畜全体の生産性を向上させる。これらの物質にはビタミン、アミノ酸、酵素、酸化防止剤、プロバイオティクスなどが含まれ、家畜の健康と生産効率を高める上で重要な役割を果たしています。世界人口の増加に伴い、高品質の食肉製品への需要が高まり、効果的な飼料ソリューションの必要性が高まっています。動物福祉への関心が高まるにつれ、畜産農家は、家禽、豚、牛、水産養殖、その他の畜産カテゴリーにおいて、より良い消化、栄養吸収、全体的なパフォーマンスを確保するための強化飼料製品を求めています。

飼料効率の改善に重点を置くことで、酵素、甘味料、プロバイオティクスなど、多様な添加物への関心が高まっています。これらの製品は消化率を高め、腸の健康を促進し、免疫機能を改善し、ひいては家畜の生産性を向上させる。さらに、食肉、乳製品、その他の農産物の生産における畜産部門の重要性は、特にトルコ、ブロイラー、豚、肉牛、乳牛などの分野で高まっています。急速な都市化、飲食品産業の成長、外食産業の拡大も、特に北米における飼料添加物需要の増加に寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 250億米ドル |

| 予測金額 | 382億米ドル |

| CAGR | 4.4% |

市場は製品タイプによって区分され、抗酸化剤が大きなシェアを占めています。酸化防止剤セグメントは2024年に91億米ドルの売上を生み出しました。北米では動物の栄養と健康への関心が高まっており、ビタミン分野の成長に寄与しています。生産者や農家は、家畜がより良いパフォーマンスと高い収量に必要な必須栄養素を確実に摂取できるよう、強化飼料製品への投資を増やしています。家畜の生産性向上は肉、乳、卵の生産量増加につながり、飼料添加物市場を強化します。A、D、E、B複合体などのビタミンは家畜に不可欠な生理学的機能を果たすため、強化飼料の採用をさらに後押ししています。

飼料添加物の技術的進歩は、動物福祉規制の厳格化とともに市場の成長を促進しています。生産者は、持続可能で効率的な家畜生産を確保しつつ、動物性タンパク質に対する需要の高まりに対応するため、強化飼料ソリューションへと移行しつつあります。この移行は、法改正や飼料品質基準に対する意識の高まりによってさらに後押しされ、強化配合飼料の採用を促進しています。

北米は世界の動物飼料添加物市場をリードし、2024年には60億米ドルの売上を生み出します。特に鶏肉部門は、鶏肉製品の需要増加の恩恵を受けています。ビタミン、ミネラル、アミノ酸、酵素、プロバイオティクスなどの添加物は、飼料利用の最適化、腸内環境の改善、家禽の生産性向上に重要な役割を果たしています。抗生物質を使用しない鶏肉生産へのシフトの拡大、高品質タンパク質の消費量の増加、厳格な食品安全規制が市場成長の主な促進要因です。さらに、進化する飼料配合政策と持続可能な有機養鶏への注目の高まりが、市場の地位をさらに強化しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 動物性タンパク質に対する需要の増加

- 動物の健康と栄養への注目

- 抗生物質の使用規制

- 業界の潜在的リスク&課題

- 不安定な原料価格

- 厳しい規制要件

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 酸化防止剤

- 色素

- 酵素

- 香料

- 甘味料

- プロバイオティクス

- ビタミン

第6章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第7章 企業プロファイル

- Adm

- Alltech

- Basf

- Biomin Holdings

- Cargill

- Dr. Eckel

- Dsm

- Dupont

- Impextraco

- Iptsa

- Kemin Industries

- Lucta

- Miavit

- Novus International

- Nutreco

- Nutriad

The Global Animal Feed Additives Market reached USD 25 billion in 2024 and is projected to grow at a CAGR of 4.4% from 2025 to 2034. Feed additives enhance the nutritional value of livestock feed and improve overall animal productivity. These substances include vitamins, amino acids, enzymes, antioxidants, and probiotics, playing a crucial role in boosting livestock health and production efficiency. As global populations rise, the demand for high-quality meat products increases, driving the need for effective feed solutions. With growing attention to animal welfare, farmers are seeking fortified feed products to ensure better digestion, nutrient absorption, and overall performance in poultry, swine, cattle, aquaculture, and other livestock categories.

The focus on improving feed efficiency has amplified interest in a diverse range of additives, including enzymes, sweeteners, and probiotics. These products enhance digestibility, promote gut health, and improve immune function, which, in turn, increases animal productivity. Additionally, the livestock sector's importance in producing meat, dairy, and other agricultural products is increasing, particularly in segments like turkeys, broilers, swine, beef, and dairy cattle. Rapid urbanization, the growing food and beverage industry, and expanding food service sectors further contribute to the rising demand for animal feed additives, particularly in North America.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $25 Billion |

| Forecast Value | $38.2 Billion |

| CAGR | 4.4% |

The market is segmented based on product type, with antioxidants holding a significant share. The antioxidant segment generated USD 9.1 billion in revenue in 2024. The growing focus on animal nutrition and well-being in North America is contributing to the growth of the vitamins segment. Producers and farmers are increasingly investing in fortified feed products to ensure that livestock receive the essential nutrients required for better performance and higher yields. Enhanced animal productivity leads to increased production of meat, milk, and eggs, strengthening the market for feed additives. Vitamins such as A, D, E, and B complexes perform vital physiological functions in livestock, further driving the adoption of fortified feeds.

Technological advancements in feed additives, along with stricter animal welfare regulations, are fostering growth in the market. Producers are shifting towards fortified feed solutions to meet rising demands for animal protein while ensuring sustainable and efficient livestock production. This transition is further supported by legislative reforms and increasing awareness of feed quality standards, promoting the adoption of enhanced feed formulations.

North America leads the global animal feed additives market, generating USD 6 billion in revenue in 2024. The poultry sector, in particular, is benefiting from the rising demand for chicken products. Additives such as vitamins, minerals, amino acids, enzymes, and probiotics play a critical role in optimizing feed utilization, improving gut health, and boosting poultry productivity. The growing shift toward antibiotic-free chicken production, higher consumption of high-quality protein, and stringent food safety regulations are the primary drivers fueling the market's growth. Moreover, evolving feed formulation policies and a heightened focus on sustainable and organic poultry farming are further strengthening the market position.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Base estimates and calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news and initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for animal protein

- 3.6.1.2 Focus on animal health and nutrition

- 3.6.1.3 Restrictions on antibiotic use

- 3.6.2 Industry pitfalls and challenges

- 3.6.2.1 volatile raw material prices

- 3.6.2.2 stringent regulatory requirements

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Antioxidant

- 5.3 Pigments

- 5.4 Enzymes

- 5.5 Flavors

- 5.6 Sweeteners

- 5.7 Probiotics

- 5.8 Vitamins

Chapter 6 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 UK

- 6.3.3 France

- 6.3.4 Spain

- 6.3.5 Italy

- 6.3.6 Netherlands

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.4.4 Australia

- 6.4.5 South Korea

- 6.5 Latin America

- 6.5.1 Brazil

- 6.5.2 Mexico

- 6.5.3 Argentina

- 6.6 Middle East and Africa

- 6.6.1 Saudi Arabia

- 6.6.2 South Africa

- 6.6.3 UAE

Chapter 7 Company Profiles

- 7.1 Adm

- 7.2 Alltech

- 7.3 Basf

- 7.4 Biomin Holdings

- 7.5 Cargill

- 7.6 Dr. Eckel

- 7.7 Dsm

- 7.8 Dupont

- 7.9 Impextraco

- 7.10 Iptsa

- 7.11 Kemin Industries

- 7.12 Lucta

- 7.13 Miavit

- 7.14 Novus International

- 7.15 Nutreco

- 7.16 Nutriad