|

市場調査レポート

商品コード

2019184

レーザー溶接機市場の機会、成長要因、業界動向分析、および2026年~2035年の予測Laser Welding Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| レーザー溶接機市場の機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年03月22日

発行: Global Market Insights Inc.

ページ情報: 英文 219 Pages

納期: 2~3営業日

|

概要

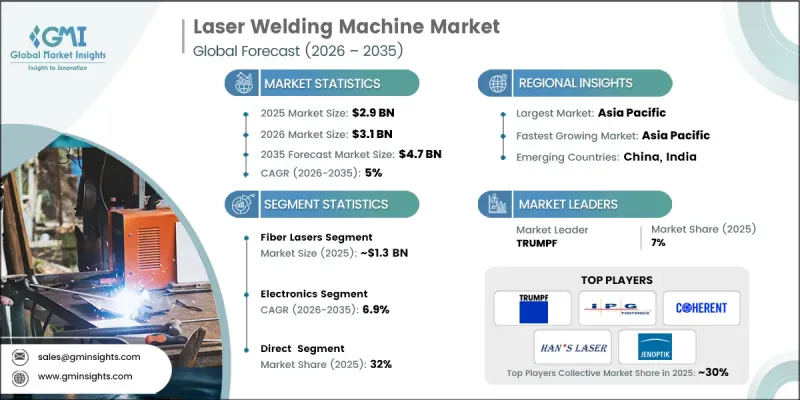

世界のレーザー溶接機市場は、2025年に29億米ドルと評価され、CAGR 5%で成長し、2035年までに47億米ドルに達すると推定されています。

各産業が自動化およびデジタル統合された製造環境への移行を加速させる中、レーザー溶接機市場は強い勢いを見せています。ロボット溶接セル、スマート生産システム、およびインダストリー4.0フレームワークの導入拡大により、高精度な溶接技術への需要が大幅に高まっています。これらの機械は、卓越した精度と再現性を備え、高度な制御プラットフォームとのシームレスな互換性を有しており、一貫性と効率性を重視する現代の産業ワークフローに極めて適しています。非接触での動作により、摩耗や損傷が最小限に抑えられ、メンテナンスの頻度が減少し、生産サイクルの途切れのない継続が保証されます。さらに、リアルタイムモニタリングと統合されたセンシング技術が自動化された品質保証を支え、その価値提案をさらに強化しています。製造業者が生産性の最適化と運用上の変動の低減を引き続き優先する中、レーザー溶接ソリューションは次世代の生産ラインにおいて不可欠な要素となりつつあります。スマートファクトリーや先進的な製造インフラへの投資拡大により、複数の産業分野における導入がさらに加速すると予想されます。

| 市場の範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026-2035 |

| 開始時の市場規模 | 29億米ドル |

| 予測額 | 47億米ドル |

| CAGR | 5% |

産業オペレーションにおいて自動化が中核となるにつれ、レーザー溶接機市場は進化を続けており、高性能な溶接システムの広範な導入を後押ししています。企業は、効率的で拡張性の高い生産へのニーズに応えるべく、ダウンタイムを最小限に抑えた連続運転を実現する技術をますます採用しています。精密制御やインテリジェントなモニタリングを含むシステムの機能強化により、製造業者は運用上の柔軟性を維持しつつ、優れた出力品質を達成できるようになっています。こうした進歩は、現代の製造エコシステムにおけるレーザー溶接装置の役割を強化し、長期的な市場拡大を支えています。

ファイバーレーザー部門は2025年に13億米ドルの市場規模を記録し、2026年から2035年にかけてCAGR4.2%で成長すると予測されています。この部門は、従来のレーザー技術と比較してエネルギー効率が高く、ビーム品質に優れ、メンテナンス要件が低いことから、強固な地位を維持しています。ファイバーレーザーシステムは、熱変形を最小限に抑えながら精密かつクリーンな溶接を可能にするため、精度と一貫性が求められる用途において極めて有効です。その採用拡大に伴い、自動および手動の溶接作業の両方で従来のレーザーシステムが徐々に置き換えられつつあり、市場における優位性がさらに強まっています。

直接販売セグメントは2025年に32%のシェアを占め、複雑な産業ソリューションの提供におけるその重要性を浮き彫りにしています。直接販売チャネルにより、メーカーはカスタマイズされたシステム構成、設置サポート、技術トレーニングを提供しながら、顧客との強固な関係を構築することができます。このアプローチは、エンドユーザーが継続的なサービス、メンテナンス、専門家の指導を必要とする高額投資機器において特に価値があります。企業が特定の運用要件を満たすための信頼できるパートナーシップとオーダーメイドのソリューションを求めるにつれ、直接的な関与を好む傾向は引き続き高まっています。

米国レーザー溶接機市場は2025年に6億米ドルに達し、2035年までCAGR5.1%で成長し、北米地域における主導的地位を維持すると予想されています。この成長は、高度な製造能力、自動化レベルの向上、および主要セクター全体における強力な産業基盤によって支えられています。精密製造プロセスへの需要の高まりと、次世代生産技術への継続的な投資が、市場の拡大を後押ししています。同国におけるイノベーションと効率改善への注力は、様々な産業用途における先進的なレーザー溶接システムの導入を牽引し続けています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 製造業における自動化の普及拡大

- 高精度溶接への需要の高まり

- レーザー光源における技術的進歩

- 落とし穴と課題

- 初期投資コストが高め

- 熟練労働力の不足

- 機会

- 電気自動車(EV)製造における利用の拡大

- 医療機器製造の拡大

- 促進要因

- 成長可能性分析

- 今後の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 規制情勢

- 北米

- 米国:消費者製品安全委員会(CPSC)、連邦規則集(CFR)第16編第1512条

- カナダ:国際標準化機構(ISO)4210

- 欧州

- ドイツ:ドイツ規格協会(DIN)欧州規格(EN)ISO 4210

- 英国:欧州規格(EN)ISO 4210/英国適合性評価(UKCA)

- フランス:欧州規格(EN)ISO 4210

- アジア太平洋地域

- 中国:国家標準(GB)3565

- インド:インド規格(IS)10613

- 日本:日本工業規格(JIS)D 9110

- ラテンアメリカ

- ブラジル:ブラジル技術規格協会(ABNT)ブラジル規格(NBR)ISO 4210

- メキシコ:国際標準化機構(ISO)4210

- 中東・アフリカ

- 南アフリカ:南アフリカ国家規格(SANS)311

- サウジアラビア:サウジアラビア規格・計量・品質機構(SASO)、湾岸標準化機構(GSO)、ISO 4210

- 北米

- 貿易データ分析(HSコード-851580)

- 輸出入数量・金額の動向

- 主要な貿易ルートと関税の影響

- AIおよび生成AIが市場に与える影響

- AIによる既存ビジネスモデルの変革

- セグメント別のGenaiの使用事例と導入ロードマップ

- リスク、制約、および規制上の考慮事項

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:技術別、2022-2035

- ファイバーレーザー

- CO2レーザー

- ダイオードレーザー

- その他

第6章 市場推計・予測:出力別、2022-2035

- 3 kW未満

- 3 kW~6 kW

- 6 kW超

第7章 市場推計・予測:最終用途別、2022-2035

- 自動車

- 医療

- エレクトロニクス

- 航空宇宙・防衛

- 宝飾品

- その他

第8章 市場推計・予測:流通チャネル別、2022-2035

- 直接

- 間接

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ(MEA)

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第10章 企業プロファイル

- Amada Weld Tech

- CHIRON Group

- Coherent

- Emerson Electric

- Han's Laser Technology Industry Group

- Huagong Laser Engineering

- IPG Photonics

- Jenoptik

- KEYENCE

- Laser Technologies

- Laser line

- Laser Star Technologies

- Penta Laser

- Precitec

- TRUMPF