|

市場調査レポート

商品コード

1716601

産業用ガス煙管ボイラー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Gas Fire Tube Industrial Boiler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 産業用ガス煙管ボイラー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月31日

発行: Global Market Insights Inc.

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

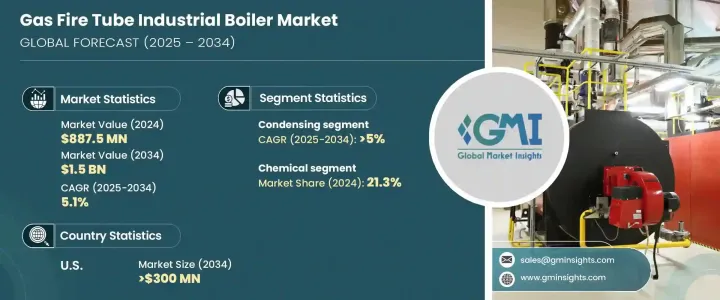

産業用ガス煙管ボイラーの世界市場は、2024年に8億8,750万米ドルに達し、2025年から2034年にかけてCAGR 5.1%で拡大すると予測されています。

この成長は、主要経済圏で工業化のペースが高まっていることと、エネルギーインフラへの投資が増加していることが主な要因です。よりクリーンなエネルギー源へのシフトは、排出削減と効率向上に焦点を当てたボイラー技術の進歩とともに、市場をさらに押し上げると予想されます。

遠隔監視と予知保全ソリューションに向けた動向の高まりは、産業用ガス煙管ボイラーの需要を引き続き煽ると思われます。このシフトは、持続可能な経済成長とスマートビル管理システムの採用に対する世界の関心の高まりと一致しています。加えて、デジタル・モニタリングや高度な燃焼制御システムなど、ボイラー技術の継続的な進歩が、業界全体における製品採用の拡大を促進すると思われます。また、持続可能な耐腐食性材料を使用した高効率ボイラーの開発を目指した投資も顕著に増加しており、市場開拓の新たなチャンスとなると思われます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 8億8,750万米ドル |

| 予測金額 | 15億米ドル |

| CAGR | 5.1% |

産業開拓、近代化、効率的で信頼性の高い蒸気発生システムに対する需要の高まりにより、市場はさらに拡大するとみられます。さらに、エネルギー効率の高い暖房技術が重視され、ボイラーシステムにデジタル技術が統合されることで、事業の見通しが強化されます。クリーンエネルギー・ソリューションの推進が強まるにつれて、こうしたグリーンイニシアチブをサポートするボイラーへの需要が高まっており、市場の拡大にさらに寄与しています。

同市場は、技術別にコンデンシング・システムと非コンデンシング・システムに区分され、いずれも環境への影響が少なく、効率が向上し、暖房にかかるコストを削減できることから、支持を集めています。特にコンデンシング・セグメントは、エネルギー・コストの上昇と環境規制の強化に牽引され、2034年までCAGR 5%以上で安定成長すると予想されます。エネルギー効率の高い機器に対する政府の奨励金やリベートも、採用を加速する上で重要な役割を果たすと思われます。

用途別では、化学分野が2024年に21.3%のシェアを獲得して市場をリードしました。新興国におけるインフラ投資の増加と高効率ボイラーシステムの採用は、今後もこの分野の成長を刺激し続けると思われます。米国では、産業用ガス燃焼管ボイラー市場は2022年に1億9,220万米ドル、2024年には2億1,330万米ドルに成長し、2034年には3億米ドルを突破する見込みです。

北米市場は、厳しいエネルギー効率規制と気候変動緩和戦略の実施により、CAGR 4.5%以上で拡大する見込みです。同地域では、低温システムにおける耐腐食性材料の採用や、高地における産業プロジェクトの開発が、継続的な市場成長の原動力となりそうです。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:容量別、2021年~2034年

- 主要動向

- 10 MMBTU/hr未満

- 10-25 MMBTU/hr

- 25-50 MMBTU/hr

- 50-75 MMBTU/hr

- 75 MMBTU/hr超

第6章 市場規模と予測:用途別、2021年~2034年

- 主要動向

- 食品加工

- パルプ・製紙

- 化学

- 精製

- 一次金属

- その他

第7章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- コンデンシング

- 非コンデンシング

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- フランス

- 英国

- ポーランド

- イタリア

- スペイン

- オーストリア

- ドイツ

- スウェーデン

- ロシア

- アジア太平洋

- 中国

- インド

- フィリピン

- 日本

- 韓国

- オーストラリア

- インドネシア

- 中東・アフリカ

- サウジアラビア

- イラン

- アラブ首長国連邦

- ナイジェリア

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

第9章 企業プロファイル

- ALFA LAVAL

- Babcock &Wilcox

- Babcock Wanson

- Clayton Industries

- Cleaver-Brooks

- EPCB Boiler

- Fulton

- Hurst Boiler &Welding

- IHI Corporation

- Johnston Boiler

- Miura America

- Rentech Boilers

- Thermax

- Thermodyne Boilers

- Viessmann

The Global Gas Fire Tube Industrial Boiler Market reached USD 887.5 million in 2024 and is projected to expand at a CAGR of 5.1% between 2025 and 2034. This growth is largely driven by the increasing pace of industrialization across key economies, coupled with rising investments in energy infrastructure. The shift towards cleaner energy sources, along with advancements in boiler technologies that focus on emissions reduction and enhanced efficiency, is expected to further boost the market.

The increasing trend towards remote monitoring and predictive maintenance solutions will continue to fuel demand for fire tube industrial boilers. This shift is aligned with the growing global focus on sustainable economic growth and the adoption of smart building management systems. In addition, continuous advancements in boiler technologies, such as digital monitoring and sophisticated combustion control systems, are likely to drive higher product adoption across industries. There is also a noticeable increase in investments aimed at developing high-efficiency boilers using sustainable, corrosion-resistant materials, which will open new opportunities for market players.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $887.5 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 5.1% |

Industrial development, modernization, and a rising demand for efficient and reliable steam generation systems are set to further penetrate the market. Additionally, the emphasis on energy-efficient heating technologies, combined with the integration of digital technologies in boiler systems, will provide an enhanced outlook for the business. As the push for clean energy solutions intensifies, there is a growing demand for boilers that support these green initiatives, further contributing to market expansion.

The market is segmented by technology into condensing and non-condensing systems, both of which are gaining traction due to their minimal environmental impact, improved efficiency, and cost savings in heating. The condensing segment, in particular, is expected to grow steadily at a CAGR of over 5% until 2034, driven by higher energy costs and stricter environmental regulations. Government incentives and rebates for energy-efficient equipment will also play a key role in accelerating adoption.

In terms of application, the chemical sector led the market with a 21.3% share in 2024. The increasing infrastructure investments and adoption of high-efficiency boiler systems in emerging economies will continue to stimulate growth in this sector. In the U.S., the market for gas fire tube industrial boilers was valued at USD 192.2 million in 2022, growing to USD 213.3 million in 2024, and expected to surpass USD 300 million by 2034.

The North American market is expected to expand at a CAGR of over 4.5% due to stringent energy efficiency regulations and the implementation of climate change mitigation strategies. The region's adoption of corrosion-resistant materials in low-temperature systems and the development of industrial projects in high-altitude areas are likely to drive continued market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 - 2034 (Units, MMBTU/hr & USD Million)

- 5.1 Key trends

- 5.2 < 10 MMBTU/hr

- 5.3 10 - 25 MMBTU/hr

- 5.4 25 - 50 MMBTU/hr

- 5.5 50 - 75 MMBTU/hr

- 5.6 > 75 MMBTU/hr

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (Units, MMBTU/hr & USD Million)

- 6.1 Key trends

- 6.2 Food processing

- 6.3 Pulp & paper

- 6.4 Chemical

- 6.5 Refinery

- 6.6 Primary metal

- 6.7 Others

Chapter 7 Market Size and Forecast, By Technology, 2021 - 2034 (Units, MMBTU/hr & USD Million)

- 7.1 Key trends

- 7.2 Condensing

- 7.3 Non-condensing

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (Units, MMBTU/hr & USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 France

- 8.3.2 UK

- 8.3.3 Poland

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Austria

- 8.3.7 Germany

- 8.3.8 Sweden

- 8.3.9 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Philippines

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.4.6 Australia

- 8.4.7 Indonesia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 Iran

- 8.5.3 UAE

- 8.5.4 Nigeria

- 8.5.5 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

Chapter 9 Company Profiles

- 9.1 ALFA LAVAL

- 9.2 Babcock & Wilcox

- 9.3 Babcock Wanson

- 9.4 Clayton Industries

- 9.5 Cleaver-Brooks

- 9.6 EPCB Boiler

- 9.7 Fulton

- 9.8 Hurst Boiler & Welding

- 9.9 IHI Corporation

- 9.10 Johnston Boiler

- 9.11 Miura America

- 9.12 Rentech Boilers

- 9.13 Thermax

- 9.14 Thermodyne Boilers

- 9.15 Viessmann