|

市場調査レポート

商品コード

1716581

固定取付式低電圧開閉装置市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Fixed Mounted Low Voltage Switchgear Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 固定取付式低電圧開閉装置市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月04日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

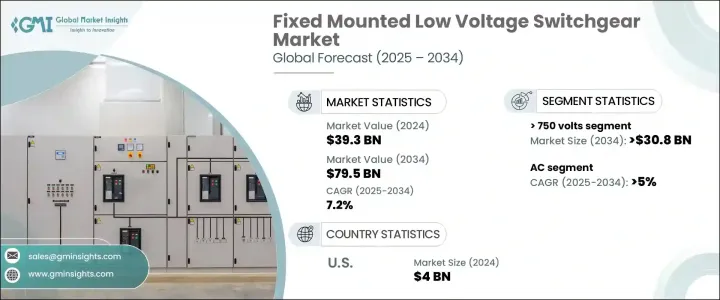

固定取付式低電圧開閉装置の世界市場規模は2024年に393億米ドルとなり、2025年から2034年にかけてCAGR 7.2%で成長すると予測されています。

この市場拡大の主な要因は、配電インフラへの投資の増加、エネルギー需要の増加、電気安全基準の継続的な進歩です。商業、工業、公益事業分野で固定取付式低電圧開閉装置が広く採用されていることは、配電、制御、保護におけるその重要な役割を浮き彫りにしています。産業が進化し、規模が拡大するにつれ、効率的で信頼性の高い電気システムへの需要は高まり続け、開閉装置ソリューションは現代の電力管理戦略の中心に位置付けられています。

産業施設、商業ビル、データセンターの増加により、信頼性の高い配電システムへの需要が大幅に高まっています。固定取付式低電圧開閉装置は、引出し式開閉装置に比べて費用対効果が高く、設置が簡単で、メンテナンスの必要性が少ないため、好まれるソリューションとなっています。産業が拡大し、商業スペースが電気インフラをアップグレードするにつれて、高度で堅牢な配電ソリューションへのニーズが加速しています。エネルギー効率の高い技術へのシフトと、さまざまな分野での電化の進展が、市場の成長をさらに後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 393億米ドル |

| 予測金額 | 795億米ドル |

| CAGR | 7.2% |

固定取付式低電圧開閉装置の需要は、750ボルト超セグメントで急増し、2034年には308億米ドルに達すると予測されます。この大幅な拡大は、大容量配電ネットワークに対するニーズの高まり、産業オートメーションの動向の高まり、再生可能エネルギーインフラの急速な拡大に起因しています。産業や公益事業がクリーンエネルギー源へとますますシフトしているため、シームレスな動作と信頼性を確保する洗練された開閉装置・ソリューションに対する需要が増加しています。さらに、持続可能性とスマートグリッド統合の推進が次世代電気システムへの投資を促進し、市場の見通しをさらに高めています。

現在のタイプに関しては、ACセグメントは2034年までCAGR 5%で成長すると予想されます。交流電力は、長距離送電と電圧変換の効率性から、世界的に送配電の主流となっています。産業機械、商業施設、住宅用電力システムなど、多様な用途で交流電力が広く使用されていることが、交流低電圧開閉装置の旺盛な需要に寄与しています。さらに、風力発電や太陽光発電などの再生可能エネルギー源の採用が拡大していることも、エネルギー配給と運用効率を最適化するACベースの開閉器ソリューションに対する需要を引き続き強化しています。

米国の固定取付式低電圧開閉装置市場は、2024年に40億米ドルを生み出し、送電網の近代化とインフラのアップグレードへの多額の投資に支えられています。米国政府は電力会社とともに、グリッドの信頼性と効率を高めるため、時代遅れの電力システムを先進的な低電圧開閉装置に置き換える投資を積極的に行っています。スマートグリッドと分散型エネルギー資源への移行は、市場の成長をさらに促進しています。さらに、製造とエネルギー効率の高い技術を促進する政府の優遇措置は、最新の開閉装置・ソリューションの需要を促進する上で重要な役割を果たしており、弾力的で将来対応可能な電気インフラを保証しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:定格電圧別、2021年~2034年

- 主要動向

- 250ボルト以下

- 250ボルト以上750ボルト未満

- 750ボルト以上

第6章 市場規模・予測:電流別、2021年~2034年

- 主要動向

- 交流

- 直流

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 変電所

- 配電

- 力率改善

- サブ配電

- モーター制御

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第9章 企業プロファイル

- ABB

- Bharat Heavy Electricals

- CG Power and Industrial Solutions

- CHINT Group

- Eaton

- Fuji Electric

- General Electric

- HD Hyundai Electric

- Hitachi

- Hyosung Heavy Industries

- Lucy Group

- Mitsubishi Electric

- Ormazabal

- Schneider Electric

- Siemens

- Skema

- Toshiba

The Global Fixed Mounted Low Voltage Switchgear Market was valued at USD 39.3 billion in 2024 and is projected to grow at a CAGR of 7.2% between 2025 and 2034. This market expansion is primarily fueled by rising investments in power distribution infrastructure, increasing energy demand, and continuous advancements in electrical safety standards. The widespread adoption of fixed mounted low voltage switchgear across commercial, industrial, and utility sectors highlights its critical role in power distribution, control, and protection. As industries evolve and scale, the demand for efficient and reliable electrical systems continues to rise, positioning switchgear solutions at the center of modern power management strategies.

The growing number of industrial facilities, commercial buildings, and data centers is significantly driving the demand for dependable electrical distribution systems. Fixed mounted low voltage switchgear has become a preferred solution due to its cost-effectiveness, ease of installation, and minimal maintenance requirements compared to withdrawable switchgear. With industries expanding and commercial spaces upgrading their electrical infrastructures, the need for advanced and robust power distribution solutions is accelerating. The shift toward energy-efficient technologies and increased electrification across various sectors further propels market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $39.3 Billion |

| Forecast Value | $79.5 Billion |

| CAGR | 7.2% |

The demand for fixed mounted low voltage switchgear is expected to surge in the >750 volts segment, which is forecast to reach USD 30.8 billion by 2034. This significant expansion is attributed to the rising need for high-capacity power distribution networks, the growing trend of industrial automation, and the rapid expansion of renewable energy infrastructure. As industries and utilities increasingly shift toward clean energy sources, the demand for sophisticated switchgear solutions that ensure seamless operation and reliability is on the rise. Additionally, the push for sustainability and smart grid integration is driving investments in next-generation electrical systems, further enhancing market prospects.

Regarding the current type, the AC segment is expected to grow at a CAGR of 5% through 2034. AC power remains the dominant choice for electricity transmission and distribution worldwide due to its efficiency in long-distance transmission and voltage conversion. The extensive use of AC power in diverse applications, including industrial machinery, commercial establishments, and residential power systems, contributes to the strong demand for AC low voltage switchgear. Furthermore, the growing adoption of renewable energy sources, such as wind and solar power, continues to reinforce the demand for AC-based switchgear solutions that optimize energy distribution and operational efficiency.

The U.S. Fixed Mounted Low Voltage Switchgear Market generated USD 4 billion in 2024, supported by substantial investments in grid modernization and infrastructure upgrades. The U.S. government, alongside utility companies, has been actively investing in replacing outdated power systems with advanced low voltage switchgear to enhance grid reliability and efficiency. The transition toward smart grids and distributed energy resources is further fueling market growth. Additionally, government incentives promoting manufacturing and energy-efficient technologies are playing a crucial role in driving demand for modern switchgear solutions, ensuring a resilient and future-ready electrical infrastructure.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Voltage Rating 2021 - 2034 (USD Million, ‘000 Units)

- 5.1 Key trends

- 5.2 ≤ 250 volts

- 5.3 > 250 volts to ≤ 750 volts

- 5.4 > 750 volts

Chapter 6 Market Size and Forecast, By Current 2021 - 2034 (USD Million, ‘000 Units)

- 6.1 Key trends

- 6.2 AC

- 6.3 DC

Chapter 7 Market Size and Forecast, By Application 2021 - 2034 (USD Million, ‘000 Units)

- 7.1 Key trends

- 7.2 Substation

- 7.3 Distribution

- 7.4 Power factor correction

- 7.5 Sub distribution

- 7.6 Motor control

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, ‘000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Italy

- 8.3.5 Russia

- 8.3.6 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Turkey

- 8.5.4 South Africa

- 8.5.5 Egypt

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Bharat Heavy Electricals

- 9.3 CG Power and Industrial Solutions

- 9.4 CHINT Group

- 9.5 Eaton

- 9.6 Fuji Electric

- 9.7 General Electric

- 9.8 HD Hyundai Electric

- 9.9 Hitachi

- 9.10 Hyosung Heavy Industries

- 9.11 Lucy Group

- 9.12 Mitsubishi Electric

- 9.13 Ormazabal

- 9.14 Schneider Electric

- 9.15 Siemens

- 9.16 Skema

- 9.17 Toshiba