|

市場調査レポート

商品コード

1716573

自動車におけるAI市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測AI in Automotive Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車におけるAI市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月10日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

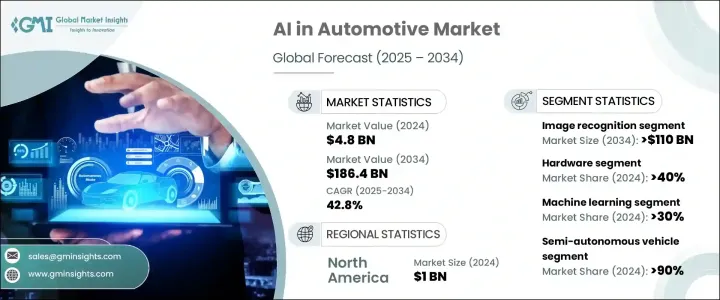

世界の自動車におけるAI市場は、2024年に48億米ドルと評価され、2025年から2034年にかけて42.8%という驚異的なCAGRを記録すると予測されています。

この急激な成長は、AI技術がモビリティの未来を再定義し続ける中、インテリジェントな自動車ソリューションに対する需要の高まりを反映しています。自動車へのAIの統合は、自動車の運用方法を変革し、乗員の安全性と運転体験の両方を向上させています。主要自動車メーカーやテクノロジー企業は、特に自律走行車や次世代ADAS(先進運転支援システム)向けのAI駆動システムに多額の投資を行っています。

自動車のインテリジェンス、状況認識、リアルタイムの意思決定を強化するAIの役割は、自動車がより安全で、よりつながり、ますます自律的になる未来に向けて自動車セクターを後押ししています。交通管理や衝突回避から、予知保全やパーソナライズされた車内体験に至るまで、AIは現代の自動車アーキテクチャの中心的な要素になりつつあります。自動車メーカーもAIを活用して、予測ナビゲーション、音声認識、行動分析機能を提供し、ドライバーと同乗者の利便性を高めています。より安全でスマートなモビリティ・ソリューションに対する消費者の需要が高まる中、AIは自動車の世界で不可欠な存在となり、今後10年間の市場成長をさらに加速させると思われます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 48億米ドル |

| 予測金額 | 1,864億米ドル |

| CAGR | 42.8% |

AI導入の急増は、ADASや自律走行ソリューションなどの技術導入の増加によるところが大きいです。AIは、先進センサー、高解像度カメラ、レーダー、LiDARシステムとのシームレスな統合を通じて、自動車の安全性と全体的な運転体験を大幅に向上させる。車線維持支援、アダプティブ・クルーズ・コントロール、自動緊急ブレーキ、歩行者検知などの機能は、車両が周囲の状況を分析して即座に運転判断を下し、事故を減らして交通安全を向上させることを可能にするAIアルゴリズムを搭載しています。

市場は主にデータマイニングや画像認識などのプロセスに基づいてセグメント化され、画像認識が優位を占めています。このセグメントは、自律走行車とADAS機能を実現する上で重要な役割を果たすことから、2034年までに1,100億米ドル以上を生み出すと予想されています。画像認識技術は、AIシステムがリアルタイムの環境データを処理・解釈し、歩行者、交通標識、車両、車線標示を正確に識別することを可能にします。ダイナミックな道路状況を認識・理解する能力により、画像認識は自律走行開発の要となっています。

コンポーネントの観点から、自動車におけるAI市場はハードウェア、ソフトウェア、サービスに分けられ、2024年にはハードウェアのシェアが40%を大きく占める。自動車メーカーは、AI搭載車の計算需要をサポートするため、先進的なハードウェアに多額の投資を行っています。AIチップ、GPU、センサー、LiDARシステムなどの専用コンポーネントは、膨大なデータストリームをリアルタイム処理するために不可欠であり、自動運転、画像検出、センサーフュージョン、ディープラーニングベースの分析などのシームレスなAI機能を可能にします。

米国の自動車におけるAI市場は、同国の強固な技術インフラと急速なAI導入により、注目すべき33%のシェアを占め、2024年には10億米ドルを創出しました。主な自動車メーカーやハイテク大手は、AIベースの自律走行技術や高度な安全システムの開発を主導しており、米国を世界のAI駆動型自動車の展望を形成する重要なプレーヤーとしてしっかりと位置づけています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- テクノロジープロバイダー

- OEMメーカー

- 流通業者

- 最終用途

- 利益率分析

- サプライヤーの状況

- 技術とイノベーションの展望

- 特許分析

- 規制状況

- 影響要因

- 促進要因

- ADAS(先進運転支援システム)と自律走行車

- 自動車の安全性向上と衝突回避

- 予知保全と車両管理

- AIを活用した車載インフォテインメントと音声アシスタント

- 業界の潜在的リスク&課題

- 高い導入コストと複雑な統合

- データプライバシーとサイバーセキュリティの懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- ソフトウェア

- サービス

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- コンピュータビジョン

- コンテキスト認識

- ディープラーニング

- 機械学習

- 自然言語処理(NLP)

第7章 市場推計・予測:プロセス別、2021年~2034年

- 主要動向

- データマイニング

- 画像認識

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 半自律走行車

- 完全自律走行車

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Alphabet

- Audi

- Bayerische Motoren Werke(BMW)

- Daimler

- Didi Chuxing

- Ford Motor

- General Motors

- Harman International Industries

- Honda Motor

- Intel

- International Business Machines(IBM)

- Microsoft

- NVIDIA

- Qualcomm

- Tesla

- Toyota Motor

- Uber Technologies

- Volvo Car

- Waymo

- Xilinx

The Global AI In Automotive Market was valued at USD 4.8 billion in 2024 and is projected to witness a staggering CAGR of 42.8% between 2025 and 2034. This exponential growth reflects the rising demand for intelligent automotive solutions as AI technologies continue to redefine the future of mobility. The integration of AI into vehicles is transforming the way cars operate, elevating both the safety and driving experience of passengers. Leading automakers and technology companies are heavily investing in AI-driven systems, particularly for autonomous vehicles and next-generation Advanced Driver Assistance Systems (ADAS).

AI's role in enhancing vehicle intelligence, situational awareness, and real-time decision-making is pushing the automotive sector toward a future where cars are safer, more connected, and increasingly autonomous. From traffic management and collision avoidance to predictive maintenance and personalized in-car experiences, AI is becoming a central component of modern vehicle architecture. Automakers are also capitalizing on AI to offer predictive navigation, voice recognition, and behavior analysis features, enhancing both driver and passenger convenience. With growing consumer demand for safer and smarter mobility solutions, AI is set to become indispensable in the automotive world, further accelerating market growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.8 Billion |

| Forecast Value | $186.4 Billion |

| CAGR | 42.8% |

The surge in AI adoption is largely driven by the increasing implementation of technologies such as ADAS and autonomous driving solutions. AI significantly enhances vehicle safety and overall driving experience through seamless integration with advanced sensors, high-resolution cameras, radar, and LiDAR systems. Features like lane-keeping assistance, adaptive cruise control, automatic emergency braking, and pedestrian detection are powered by AI algorithms that enable vehicles to analyze their surroundings and make instant driving decisions, reducing accidents and improving road safety.

The market is primarily segmented based on processes like data mining and image recognition, with image recognition dominating the landscape. This segment is expected to generate over USD 110 billion by 2034, driven by its critical role in enabling autonomous vehicles and ADAS functionalities. Image recognition technology allows AI systems to process and interpret real-time environmental data, identifying pedestrians, traffic signs, vehicles, and lane markings with precision. The ability to perceive and understand dynamic road conditions makes image recognition a cornerstone of autonomous driving development.

In terms of components, the AI in automotive market is divided into hardware, software, and services, with hardware accounting for a significant 40% share in 2024. Automotive manufacturers are heavily investing in advanced hardware to support the computational demands of AI-powered vehicles. Specialized components such as AI chips, GPUs, sensors, and LiDAR systems are essential to handle vast streams of data for real-time processing, enabling seamless AI functionalities like automated driving, image detection, sensor fusion, and deep learning-based analytics.

The U.S. AI in automotive market commanded a notable 33% share and generated USD 1 billion in 2024, thanks to the country's robust technological infrastructure and rapid AI adoption. Major automakers and tech giants are leading the charge in developing AI-based autonomous driving technologies and advanced safety systems, firmly positioning the U.S. as a key player in shaping the global AI-driven automotive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Technology providers

- 3.1.1.2 OEM Manufacturers

- 3.1.1.3 Distributors

- 3.1.1.4 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Advanced Driver Assistance Systems (ADAS) and Autonomous Vehicles

- 3.5.1.2 Enhanced Vehicle Safety and Collision Avoidance

- 3.5.1.3 Predictive Maintenance and Fleet Management

- 3.5.1.4 AI-powered In-Vehicle Infotainment and Voice Assistants

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 High Implementation Costs and Integration Complexity

- 3.5.2.2 Data Privacy and Cybersecurity Concerns

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Service

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Computer vision

- 6.3 Context awareness

- 6.4 Deep learning

- 6.5 Machine learning

- 6.6 Natural Language Processing (NLP)

Chapter 7 Market Estimates & Forecast, By Process, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Data mining

- 7.3 Image recognition

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Semi-Autonomous vehicles

- 8.3 Fully Autonomous vehicles

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alphabet

- 10.2 Audi

- 10.3 Bayerische Motoren Werke (BMW)

- 10.4 Daimler

- 10.5 Didi Chuxing

- 10.6 Ford Motor

- 10.7 General Motors

- 10.8 Harman International Industries

- 10.9 Honda Motor

- 10.10 Intel

- 10.11 International Business Machines (IBM)

- 10.12 Microsoft

- 10.13 NVIDIA

- 10.14 Qualcomm

- 10.15 Tesla

- 10.16 Toyota Motor

- 10.17 Uber Technologies

- 10.18 Volvo Car

- 10.19 Waymo

- 10.20 Xilinx