|

市場調査レポート

商品コード

1716555

永久磁石市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Permanent Magnet Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 永久磁石市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月06日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

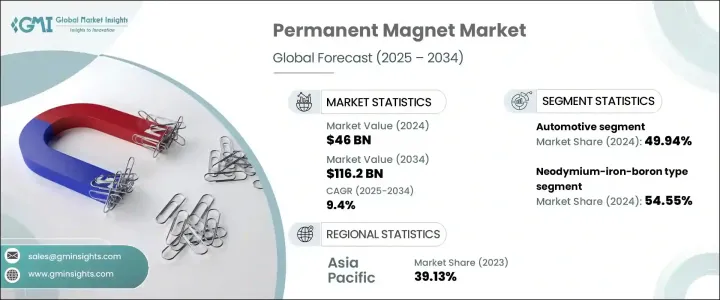

永久磁石の世界市場は2024年に460億米ドルを創出し、2025年から2034年にかけてCAGR 9.4%で拡大すると予測されています。

その主な要因は、電気自動車(EV)の普及率の上昇と、業界全体におけるエネルギー効率の高い技術に対する需要の高まりです。永久磁石は、電気モーターや風力タービンから医療機器や家電製品に至るまで、幅広い製品で重要な役割を果たしており、現代のエンジニアリングには欠かせないものです。産業界が持続可能でエネルギー効率の高いソリューションを優先し続ける中、継続的なエネルギー投入なしに優れた強度と信頼性を実現する高性能磁石の必要性は、さらに顕著になっています。

外部電源なしで持続的な磁場を維持できる磁石は、特に効率と省スペース設計が重要な、さまざまな機械的・電子的用途に好まれます。輸送や産業オートメーションにおける電動化へのシフトが加速していることに加え、ロボット工学、航空宇宙、ヘルスケア機器でも技術革新が進んでいるため、高度な永久磁石の需要はさらに高まっています。日常生活におけるスマートテクノロジーやIoT対応機器の急速な統合も、永久磁石の幅広い用途展開に寄与しています。さらに、風力発電や太陽光発電などの再生可能エネルギー源を推進する政府の取り組みが、エネルギー生成・貯蔵装置に不可欠な高性能磁石のニーズを間接的に高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 460億米ドル |

| 予測金額 | 1,162億米ドル |

| CAGR | 9.4% |

永久磁石市場は、製品タイプ別にフェライト、ネオジム-鉄-ボロン(NdFeB)、サマリウム-コバルト、アルミニウム-ニッケル-コバルトに分類されます。このうち、ネオジム-鉄-ボロン(NdFeB)磁石は、主にその卓越した磁気特性により、2024年には54.55%のシェアを占め、市場を独占しています。これらの磁石は、高い磁気エネルギー、安定した性能、高い飽和誘導で好まれ、電気モーター、発電機、オーディオシステム、各種モーター駆動電子機器での使用に不可欠となっています。材料科学と磁石技術の継続的な進歩により、NdFeB磁石は業界を問わず幅広く採用されるようになり、従来の使用事例を凌駕して、軽量かつ強力な磁石が重要な航空宇宙や先端ロボットなどの分野に新たなビジネスチャンスが広がっています。

アプリケーションの観点から見ると、自動車分野は2024年に永久磁石市場の49.94%という大きなシェアを占め、2034年までCAGR 9.5%で成長すると予測されています。自動車産業が電動モビリティに大きく舵を切る中、高効率モーター、先進パワートレイン・システム、精密センサーの統合が加速しています。ネオジム・鉄・ボロン磁石は、そのコンパクトなサイズと優れた性能から、電気自動車(EV)モーター、回生ブレーキシステム、その他の中核的な自動車用電子機器の重要な部品となっており、市場の拡大をさらに促進しています。

地域別では、アジア太平洋永久磁石市場が2023年に39.13%の圧倒的なシェアを占め、中国がその広範なレアアース生産能力によって主導的地位を占めています。中国は、ネオジム・鉄・ボロン磁石やサマリウム・コバルト磁石に不可欠な材料を含め、世界のレアアース供給の大部分を掌握しているため、競争力のある価格設定とサプライチェーンの安定性が確保されています。さらに、インド、日本、韓国などの国々による工業化の進展と堅調な需要は、EV市場の拡大、再生可能エネルギープロジェクト、家電製品の生産に支えられ、世界の永久磁石業界におけるアジア太平洋地域の地位を引き続き強化しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 電気自動車需要の高まり

- 持続可能なエネルギー生成への世界的シフト

- 製造技術の進歩

- 業界の潜在的リスク&課題

- 原材料の高価格と入手可能性の制限

- レアアースによる危険性

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- フェライト

- ネオ(NdFeB)

- SmCO

- アルニコ

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 自動車

- エレクトロニクス

- エネルギー発電

- その他

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第8章 企業プロファイル

- Hitachi Metals, Ltd.

- Jiangmen Magsource New Material Co. Ltd.

- Adams Magnetic Products Co.

- Arnold Magnetic Technologies

- Anhui Earth-Panda Advance Magnetic Material Co. Ltd.

- Ningbo Yunsheng Co. Ltd.

- Daido Steel Co. Ltd.

- Molycorp Magnequench

- Thomas &Skinner Inc.

- Vacuumschmelze GmbH &Co. KG

- Electron Energy Corporation

- Hangzhou Permanent Magnet Group

- Goudsmit Magnetics Group

- TDK Corporation

The Global Permanent Magnet Market generated USD 46 billion in 2024 and is projected to expand at a 9.4% CAGR from 2025 to 2034, fueled largely by the increasing penetration of electric vehicles (EVs) and the rising demand for energy-efficient technologies across industries. Permanent magnets are indispensable in modern engineering, playing a vital role in a wide array of products ranging from electric motors and wind turbines to medical devices and consumer electronics. As industries continue to prioritize sustainable and energy-efficient solutions, the need for high-performance magnets that deliver superior strength and reliability without continuous energy input is becoming even more prominent.

Their ability to maintain a persistent magnetic field without external power makes them a preferred choice for various mechanical and electronic applications, especially where efficiency and space-saving designs are critical. The accelerating shift toward electrification in transportation and industrial automation, along with ongoing innovations in robotics, aerospace, and healthcare equipment, further elevates the demand for advanced permanent magnets. The rapid integration of smart technologies and IoT-enabled devices in daily life has also contributed to the broader application landscape of these magnets. Moreover, government initiatives promoting renewable energy sources such as wind and solar power are indirectly bolstering the need for high-performance magnets essential for energy generation and storage equipment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $46 Billion |

| Forecast Value | $116.2 Billion |

| CAGR | 9.4% |

The permanent magnet market is categorized by product type into ferrite, neodymium-iron-boron (NdFeB), samarium-cobalt, and aluminum-nickel-cobalt. Among these, neodymium-iron-boron (NdFeB) magnets dominated the market with a commanding 54.55% share in 2024, primarily due to their exceptional magnetic properties. These magnets are favored for their high magnetic energy, stable performance, and high saturation induction, which make them essential for use in electric motors, generators, audio systems, and various motor-driven electronics. The ongoing advancements in material science and magnet technology have led to broader adoption of NdFeB magnets across industries, surpassing traditional use cases and opening new opportunities in sectors like aerospace and advanced robotics, where lightweight yet powerful magnets are crucial.

From an application standpoint, the automotive segment accounted for a substantial 49.94% share of the permanent magnet market in 2024 and is anticipated to grow at a 9.5% CAGR through 2034. As the automotive industry pivots sharply toward electric mobility, the integration of high-efficiency motors, advanced powertrain systems, and precision sensors is accelerating. Neodymium-iron-boron magnets, given their compact size and superior performance, have become critical components in electric vehicle (EV) motors, regenerative braking systems, and other core automotive electronics, further driving market expansion.

Regionally, the Asia Pacific Permanent Magnet Market held a dominant 39.13% share in 2023, with China spearheading this leadership position due to its extensive rare earth production capabilities. China's control over a large portion of the global rare earth supply, including materials crucial for neodymium-iron-boron and samarium-cobalt magnets, ensures competitive pricing and supply chain stability. Additionally, growing industrialization and robust demand from countries like India, Japan, and South Korea continue to strengthen Asia Pacific's standing in the global permanent magnet industry, supported by expanding EV markets, renewable energy projects, and consumer electronics production.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand of electric vehicle

- 3.6.1.2 Global shift towards sustainable energy generation

- 3.6.1.3 Advancements in manufacturing technologies

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High price and limited availability of raw materials

- 3.6.2.2 Hazards caused by rare earth metals

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Ferrite

- 5.3 Neo (NdFeB)

- 5.4 SmCO

- 5.5 Alnico

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Automotive

- 6.3 Electronics

- 6.4 Energy generation

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Hitachi Metals, Ltd.

- 8.2 Jiangmen Magsource New Material Co. Ltd.

- 8.3 Adams Magnetic Products Co.

- 8.4 Arnold Magnetic Technologies

- 8.5 Anhui Earth-Panda Advance Magnetic Material Co. Ltd.

- 8.6 Ningbo Yunsheng Co. Ltd.

- 8.7 Daido Steel Co. Ltd.

- 8.8 Molycorp Magnequench

- 8.9 Thomas & Skinner Inc.

- 8.10 Vacuumschmelze GmbH & Co. KG

- 8.11 Electron Energy Corporation

- 8.12 Hangzhou Permanent Magnet Group

- 8.13 Goudsmit Magnetics Group

- 8.14 TDK Corporation