廃プラスチック熱分解油市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Plastic Waste Pyrolysis Oil Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1716534

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

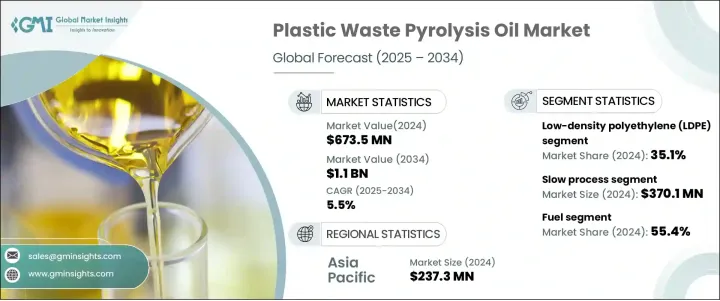

廃プラスチック熱分解油の世界市場は、2024年に6億7,350万米ドルを生み出し、2025年から2034年にかけてCAGR 5.5%で成長すると予測されています。

この市場は、世界の産業界や政府が持続可能な廃棄物管理ソリューションをますます重視し、化石燃料への依存を減らすために代替燃料源を求めるようになるにつれて、着実な成長を遂げています。無酸素環境下でのプラスチック廃棄物の熱分解から得られる廃プラスチック熱分解油は、リサイクル不可能なプラスチックを貴重な燃料や原料に変換するための実行可能なソリューションとして台頭してきています。廃棄物の最小化と資源効率の促進を目指した循環型経済へのシフトの高まりが、市場拡大の原動力となっています。熱分解オイルは、温室効果ガスの排出を削減し、エネルギー効率を向上させ、輸送用燃料、工業用暖房油、石油化学原料の需要増を支えることができるため、支持を集めています。熱分解技術の進歩によりプロセス効率が向上し、操業コストが削減されるため、廃プラスチック熱分解油市場は大きく成長する見込みです。

市場は原料によって区分され、2024年には低密度ポリエチレン(LDPE)が35.1%で最大のシェアを占める。LDPEは、プラスチック袋やフィルムなどの包装材料に広く使用されているが、融点が低く収率が高いため、依然として熱分解の有力候補です。LDPE廃棄物は機械的プロセスによるリサイクルが困難なため、熱分解のような化学的リサイクル方法の需要が高まっています。LDPE由来の熱分解オイルは魅力的な代替燃料源になりつつあります。特に、各国政府が埋立地に対する厳しい規制を実施し、環境への影響を減らすために廃棄物エネルギー化システムを推進しているためです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 6億7,350万米ドル |

| 予測金額 | 11億米ドル |

| CAGR | 5.5% |

廃プラスチック熱分解油市場はプロセスタイプ別にも分類され、低速熱分解は2024年に3億7,010万米ドルを生み出します。低速熱分解は、油収量が高く安定性が高いため、熱分解油の生産に適した方法です。300~500℃の低温で作動し、滞留時間を長くするこのプロセスは、より効率的な熱分解を保証し、液体燃料の生産量を増加させる。このプロセスは、大規模な商業用途において最も費用対効果の高い選択肢であり続け、操業コストを最小限に抑えながら収率を最大化することを目指す産業にとって好ましい選択肢となっています。

アジア太平洋廃プラスチック熱分解油産業は、2024年に2億3,730万米ドルを生み出し、2034年までにCAGR 5.7%で成長すると予想されています。同地域の優位性は、急速な工業化、都市化、プラスチック使用の普及が後押ししています。アジア太平洋のいくつかの国は、プラスチック廃棄物の増加問題に対処するため、熱分解プラントの開発に多額の投資を行っています。廃棄物エネルギー化技術と持続可能な実践に強く焦点を当てることで、この地域はプラスチック廃棄物を価値ある資源に変換する方向への世界のシフトをリードしています。廃棄物管理における環境の持続可能性と技術革新への取り組みの高まりは、アジア太平洋地域およびそれ以外の地域でも、廃プラスチック熱分解油の需要を引き続き牽引しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 政府の有利な取り組み

- 急速な都市化と工業化

- 都市固形廃棄物(MSW)の増加

- 業界の潜在的リスク&課題

- 高い生産コスト

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場規模・予測:原料別、2021年~2034年

- 主要動向

- 低密度ポリエチレン(LDPE)

- 高密度ポリエチレン(HDPE)

- ポリプロピレン(PP)

- その他

第6章 市場規模・予測:プロセス別、2021年~2034年

- 主要動向

- ファスト

- フラッシュ

- スロー

第7章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 燃料

- 化学

- 熱・電力

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Nexus Circular

- OMV Aktiengesellschaft

- Niutech Environment Technology Corporation

- Klean Industries

- Fortum OyJ

- Enerkem

- Ensyn Corporation

- Twence B.V.

- Agilyx Corporation

- Green Fuel Nordic Corporation

- Vadxx Energy LLC

- Quantafuel AS

- RESYNERGI

- JBI Inc.

目次

The Global Plastic Waste Pyrolysis Oil Market generated USD 673.5 million in 2024 and is projected to grow at a CAGR of 5.5% between 2025 and 2034. This market is experiencing steady growth as industries and governments worldwide increasingly emphasize sustainable waste management solutions and seek alternative fuel sources to reduce dependence on fossil fuels. Plastic waste pyrolysis oil, derived from the thermal decomposition of plastic waste in an oxygen-free environment, is emerging as a viable solution for converting non-recyclable plastics into valuable fuels and feedstock. The increasing shift toward circular economy practices, aimed at minimizing waste and promoting resource efficiency, is driving market expansion. Pyrolysis oil is gaining traction due to its ability to reduce greenhouse gas emissions, improve energy efficiency, and support the growing demand for transport fuels, industrial heating oils, and petrochemical feedstock. With advancements in pyrolysis technologies enhancing process efficiency and reducing operational costs, the market for plastic waste pyrolysis oil is poised for significant growth.

The market is segmented based on feedstock, with low-density polyethylene (LDPE) holding the largest share at 35.1% in 2024. LDPE, widely used in packaging materials such as plastic bags and films, remains a prime candidate for pyrolysis due to its lower melting point and high yield efficiency. As LDPE waste is difficult to recycle through mechanical processes, the demand for chemical recycling methods like pyrolysis is increasing. LDPE-derived pyrolysis oil is becoming an attractive alternative fuel source, especially as governments implement stringent regulations on landfills and promote waste-to-energy systems to reduce environmental impact.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $673.5 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 5.5% |

The plastic waste pyrolysis oil market is also classified by process type, with slow pyrolysis generating USD 370.1 million in 2024. Slow pyrolysis is the preferred method for producing pyrolysis oil because of its higher oil yield and stability. Operating at lower temperatures between 300-500°C and extended residence times, this process ensures more efficient thermal decomposition, resulting in increased liquid fuel production. It remains the most cost-effective option for large-scale commercial applications, making it a preferred choice for industries aiming to maximize yield while minimizing operational costs.

The Asia Pacific Plastic Waste Pyrolysis Oil Industry generated USD 237.3 million in 2024 and is expected to grow at a CAGR of 5.7% by 2034. The region's dominance is fueled by rapid industrialization, urbanization, and widespread plastic usage. Several countries across Asia Pacific are investing heavily in developing pyrolysis plants to address the rising issue of plastic waste. With a strong focus on waste-to-energy technologies and sustainable practices, the region is leading the global shift toward converting plastic waste into valuable resources. This increasing commitment to environmental sustainability and innovation in waste management continues to drive demand for plastic waste pyrolysis oil in Asia Pacific and beyond.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Favourable government initiatives

- 3.6.1.2 Rapid urbanization and industrialization

- 3.6.1.3 Increasing amount municipal solid waste (MSW)

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High production costs

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Feedstock, 2021 – 2034 (USD Million, Tons)

- 5.1 Key trends

- 5.2 Low density polyethylene (LDPE)

- 5.3 High density polyethylene (HDPE)

- 5.4 Polypropylene (PP)

- 5.5 Others

Chapter 6 Market Size and Forecast, By Process, 2021 – 2034 (USD Million, Tons)

- 6.1 Key trends

- 6.2 Fast

- 6.3 Flash

- 6.4 Slow

Chapter 7 Market Size and Forecast, By End Use, 2021 – 2034 (USD Million, Tons)

- 7.1 Key trends

- 7.2 Fuel

- 7.3 Chemicals

- 7.4 Heat & power

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Nexus Circular

- 9.2 OMV Aktiengesellschaft

- 9.3 Niutech Environment Technology Corporation

- 9.4 Klean Industries

- 9.5 Fortum OyJ

- 9.6 Enerkem

- 9.7 Ensyn Corporation

- 9.8 Twence B.V.

- 9.9 Agilyx Corporation

- 9.10 Green Fuel Nordic Corporation

- 9.11 Vadxx Energy LLC

- 9.12 Quantafuel AS

- 9.13 RESYNERGI

- 9.14 JBI Inc.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日