ヴィーガンプロテインパウダー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Vegan Protein Powder Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1716498

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

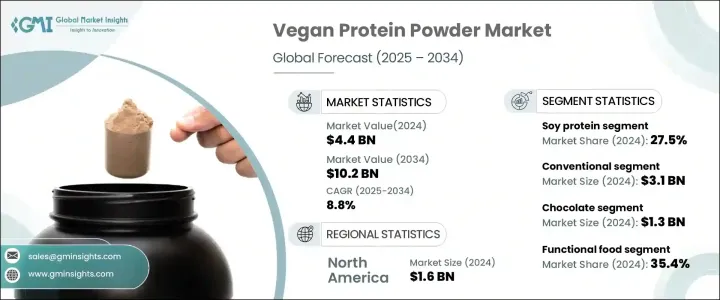

ヴィーガンプロテインパウダーの世界市場は2024年に44億米ドルに達し、2025年から2034年にかけてCAGR 8.8%で成長すると予測されています。

この力強い成長は、特にアスリート、健康志向の個人、ビーガンまたはベジタリアンの食生活を遵守する人々の間で、植物由来の代替タンパク質への嗜好が高まっていることに後押しされています。消費者がより倫理的で持続可能な食習慣を受け入れるにつれて、非動物由来のタンパク質源に対する需要が急増しています。加えて、環境の持続可能性や従来の畜産による悪影響に対する懸念の高まりが、消費者の価値観に沿った代替タンパク源の探求を後押ししています。ヴィーガンプロテインパウダー市場の企業各社は、強化されたアミノ酸プロファイル、改善された消化性、その他の健康特典を備えた革新的な製品を提供することにより、この動向を活用し、より幅広い消費者に対応しています。

フィットネス文化の台頭と、植物性タンパク質に関連する健康上の利点に対する意識の高まりが、市場をさらに強化しています。植物性タンパク質パウダーは、必須ビタミンとミネラルで強化されていることが多く、より健康的なライフスタイルを求める消費者にアピールしています。機能性食品への需要が高まるにつれて、メーカーは栄養要件を満たすだけでなく、筋肉の回復、体重管理、免疫力の強化などの利点も提供するプロテインパウダーの製造にますます力を入れるようになっています。この継続的な技術革新は、フィットネス愛好家やプロのアスリートから、単に健康全般の向上を目指す個人まで、多様な消費者層を引き付け続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 44億米ドル |

| 予測金額 | 102億米ドル |

| CAGR | 8.8% |

市場は、エンドウ豆、大豆、米、麻、その他の品種など、タンパク源によって分類されます。市場のかなりのシェアを占める濃縮大豆たん白は、2034年までにCAGR 9.7%の成長が見込まれます。その幅広い人気は、優れたアミノ酸プロファイル、優れた溶解性、手頃な価格によるもので、スポーツ栄養や機能性食品に理想的な選択肢となっています。さらに、濃縮大豆タンパク質の汎用性と入手しやすさがその優位性を高め、ビーガンタンパク質パウダー業界の成長の極めて重要な原動力として位置づけられています。

性質上、市場は有機と従来型に区分されます。従来型セグメントは2024年に31億米ドルを生み出し、2034年までCAGR 8.4%で成長すると予測されています。従来型のビーガンタンパク質パウダーは、手頃な価格で広く入手可能なため、依然として好ましい選択肢です。製造業者が従来の蛋白源を好むのは、製造コストが低く、機能性含有量が高いからです。これらの製品は主要な飲食品用途で強い存在感を示しており、強固な小売ネットワークが継続的な市場拡大を後押ししています。

北米は2024年にヴィーガンプロテインパウダー市場の16億米ドルを占め、2034年までにCAGR 3.6%で成長すると予想されています。この地域は植物性栄養に対する強い需要があり、確立された健康とウェルネス部門と相まって、世界最大の市場となっています。カナダのオーガニック製品やクリーンラベル製品に対する嗜好の高まりと、植物由来産業を支援する政府の取り組みが、同地域の市場牽引に大きく寄与しています。菜食主義、フィットネス文化、機能性食品への需要の高まりは、菜食主義プロテインパウダー市場における北米の支配的地位をさらに強化しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 菜食主義者の増加による植物由来の飲食品への需要の高まりが市場成長を牽引しています。

- 高タンパク質を含む機能性食品と健康的な製品に対する需要の増加

- スポーツ栄養市場の成長

- 業界の潜在的リスク&課題

- 高い生産コスト

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- ヘンプタンパク

- 分離大豆たん白

- 濃縮大豆たん白

- 分離米タンパク

- 濃縮米タンパク

- 分離エンドウ豆プロテイン

- 濃縮エンドウ豆プロテイン

- スピルリナタンパク

- キヌアプロテイン

- プロテインブレンド

第6章 市場規模・予測:由来別、2021年~2034年

- 主要動向

- オーガニック

- 従来

第7章 市場規模・予測:フレーバー別、2021年~2034年

- 主要動向

- ノンフレーバー

- チョコレート

- バニラ

- ストロベリー

- その他

第8章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- スポーツ栄養

- 飲料

- 機能性食品

- その他

第9章 市場規模・予測:流通チャネル別、2021年~2034年

- 主要動向

- ハイパーマーケット・スーパーマーケット

- 専門店

- オンライン小売

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- Archer-Daniels-Midland Company

- AMCO Proteins

- Bunge Global SA

- Cargill, Incorporated

- Garden Of Life

- Glanbia plc

- Ingredion Incorporated

- Now Foods

- Orgain

- PlantFusion

- Vitaco Health Group

- Wilmar International Limited

目次

The Global Vegan Protein Powder Market reached USD 4.4 billion in 2024 and is projected to grow at a CAGR of 8.8% between 2025 and 2034. This robust growth is fueled by the increasing preference for plant-based protein alternatives, especially among athletes, health-conscious individuals, and those adhering to vegan or vegetarian diets. As consumers embrace more ethical and sustainable eating habits, the demand for non-animal-based protein sources has skyrocketed. Additionally, growing concerns about environmental sustainability and the adverse effects of traditional livestock farming have pushed consumers to explore alternative protein sources that align with their values. Companies in the vegan protein powder market are capitalizing on this trend by offering innovative products with enhanced amino acid profiles, improved digestibility, and additional health benefits, catering to a broader audience.

The rise of fitness culture and the growing awareness of the health advantages associated with plant-based proteins have further bolstered the market. Plant-based protein powders, often fortified with essential vitamins and minerals, appeal to consumers seeking healthier lifestyles. As the demand for functional foods grows, manufacturers are increasingly focusing on creating protein powders that not only meet nutritional requirements but also provide benefits such as muscle recovery, weight management, and enhanced immunity. This ongoing innovation continues to attract a diverse consumer base, ranging from fitness enthusiasts and professional athletes to individuals simply looking to improve their overall well-being.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.4 Billion |

| Forecast Value | $10.2 Billion |

| CAGR | 8.8% |

The market is categorized by the source of protein, including pea, soy, rice, hemp, and other varieties. Soy protein concentrate, which holds a substantial share of the market, is expected to grow at a CAGR of 9.7% by 2034. Its widespread popularity is due to its superior amino acid profile, excellent solubility, and affordability, making it an ideal choice for sports nutrition and functional foods. Additionally, soy protein concentrate's versatility and accessibility enhance its dominance, positioning it as a pivotal driver of growth in the vegan protein powder industry.

In terms of nature, the market is segmented into organic and conventional categories. The conventional segment generated USD 3.1 billion in 2024 and is projected to grow at a CAGR of 8.4% through 2034. Conventional vegan protein powders remain the preferred choice due to their affordability and widespread availability. Manufacturers favor conventional protein sources because of their lower production costs and high functional content. These products enjoy a strong presence in mainstream food and beverage applications, supported by robust retail networks that drive continued market expansion.

North America accounted for USD 1.6 billion of the vegan protein powder market in 2024 and is expected to grow at a CAGR of 3.6% by 2034. The region's strong demand for plant-based nutrition, coupled with a well-established health and wellness sector, has made it the largest market globally. Canada's growing preference for organic and clean-label products, along with government initiatives supporting plant-based industries, contributes significantly to the region's leadership in the market. The rise in veganism, fitness culture, and the demand for functional foods further strengthens North America's dominant position in the vegan protein powder market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for plant-based food & beverages due to growing vegan population is driving market growth

- 3.6.1.2 Increasing demand for functional food and healthy products with high protein content

- 3.6.1.3 Growing market for sports nutrition

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High production costs

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Hemp protein

- 5.3 Soy protein isolate

- 5.4 Soy protein concentrate

- 5.5 Rice protein isolate

- 5.6 Rice protein concentrate

- 5.7 Pea protein isolate

- 5.8 Pea protein concentrate

- 5.9 Spirulina protein

- 5.10 Quinoa protein

- 5.11 Protein blends

Chapter 6 Market Size and Forecast, By Nature, 2021 - 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Organic

- 6.3 Conventional

Chapter 7 Market Size and Forecast, By Flavor, 2021 - 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Unflavoured

- 7.3 Chocolate

- 7.4 Vanilla

- 7.5 Strawberry

- 7.6 Other

Chapter 8 Market Size and Forecast, By Application, 2021 - 2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Sports nutrition

- 8.3 Beverages

- 8.4 Functional food

- 8.5 Others

Chapter 9 Market Size and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 Hypermarkets & supermarkets

- 9.3 Specialty stores

- 9.4 Online retail

- 9.5 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Archer-Daniels-Midland Company

- 11.2 AMCO Proteins

- 11.3 Bunge Global SA

- 11.4 Cargill, Incorporated

- 11.5 Garden Of Life

- 11.6 Glanbia plc

- 11.7 Ingredion Incorporated

- 11.8 Now Foods

- 11.9 Orgain

- 11.10 PlantFusion

- 11.11 Vitaco Health Group

- 11.12 Wilmar International Limited

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日